Current Mortgage Rates Georgia April 2026 — Today’s Rates, Forecast, Monthly Payments & Best Lenders

Updated April 2026. Mortgage rates in Georgia remain one of the most important financial factors influencing homebuyers in cities like Atlanta, Savannah, Augusta, and Columbus. Whether you're purchasing your first home or refinancing, understanding current mortgage rates Georgia April 2026 can save you tens — even hundreds — of thousands of dollars over the life of your loan.

In this complete Nexuora premium guide, we break down real-time rates, lender comparisons, monthly payment simulations, refinancing strategies, and a realistic forecast for 2026–2027 based on economic data and market trends.

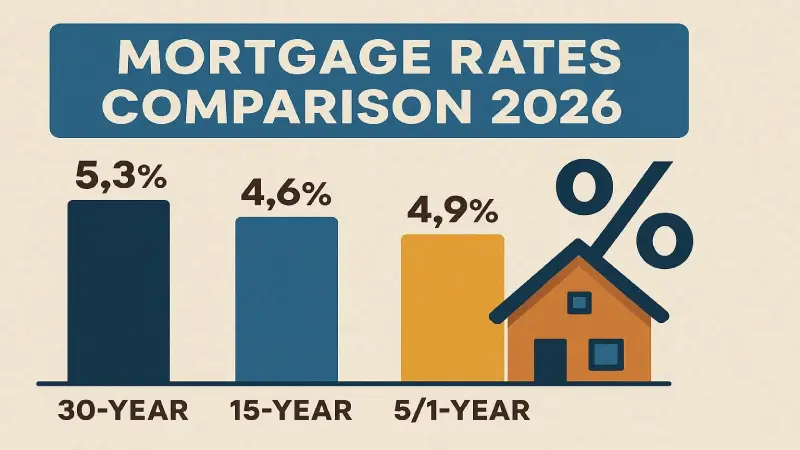

📊 Current Mortgage Rates in Georgia (April 2026)

| Loan Type | Average Rate | APR | Trend |

|---|---|---|---|

| 30-Year Fixed | 6.30% – 6.40% | 6.50%+ | ⬆ Slight increase |

| 15-Year Fixed | 5.60% – 5.75% | 5.85% | Stable |

| 5/1 ARM | 6.10% | 6.30% | Variable |

| 30-Year Refinance | 6.60%+ | 6.75% | ⬆ |

👉 According to market data, Georgia mortgage rates align closely with national averages around 6.3% for 30-year loans. :contentReference[oaicite:0]{index=0}

---📈 Why Mortgage Rates Are High in 2026

Mortgage rates are driven by macroeconomic forces — not banks alone.

1. Federal Reserve Policy

The Federal Reserve maintains higher interest rates to control inflation, directly impacting mortgage pricing.

2. Inflation Pressure

Persistent inflation keeps borrowing costs elevated across the U.S.

3. Treasury Yield Influence

Mortgage rates follow the 10-year Treasury yield, which remains volatile.

4. Georgia Housing Demand

Georgia remains one of the fastest-growing states in the U.S., especially Atlanta, increasing demand and keeping rates competitive.

---

🏡 Monthly Mortgage Payment Examples (Real Georgia Scenarios)

| Home Price | Down Payment | Loan | Rate | Monthly Payment |

|---|---|---|---|---|

| $250,000 | 20% | $200,000 | 6.3% | $1,240 |

| $350,000 | 20% | $280,000 | 6.3% | $1,730 |

| $400,000 | 20% | $320,000 | 6.3% | $1,980 |

| $500,000 | 20% | $400,000 | 6.3% | $2,470 |

👉 Even a 0.25% rate difference can change your payment significantly over time.

---🔍 Best Mortgage Lenders in Georgia (2026)

| Lender | Best For | Advantage |

|---|---|---|

| Rocket Mortgage | Online buyers | Fast approval |

| Bank of America | First-time buyers | Low down payment |

| Wells Fargo | Refinancing | Flexible options |

| Chase | Low rates | Strong reputation |

🔄 Refinance Rates in Georgia

Refinancing allows you to:

- Reduce monthly payments

- Access home equity

- Switch from ARM to fixed

👉 Current refinance rates average 6.6%+. :contentReference[oaicite:1]{index=1}

---📊 Fixed vs ARM Mortgage

| Type | Pros | Cons |

|---|---|---|

| Fixed | Stable payments | Higher rate |

| ARM | Lower start | Rate risk |

💡 How to Get the Lowest Rate in Georgia

- Improve credit score (700+)

- Increase down payment

- Compare multiple lenders

- Lock your rate early

- Buy discount points

📉 Mortgage Rate Forecast Georgia 2026–2027

Forecast models suggest:

- Rates staying between 5.8% and 6.5%

- Possible decline late 2026

- No return to 3% rates

👉 Experts predict mortgage rates will remain around 6% throughout 2026. :contentReference[oaicite:2]{index=2}

---🔗 Internal Nexuora Resources

---❓ FAQ — Mortgage Rates Georgia 2026

What is the current mortgage rate in Georgia?

Average rates are around 6.3% for a 30-year fixed mortgage.

Will rates go down?

Slight decrease expected, but still above 5.5%.

Best loan type?

30-year fixed for stability, 15-year for savings.

Is refinancing worth it?

Yes if you reduce your rate by at least 0.5%.

---✅ Final Verdict

Mortgage rates in Georgia in 2026 are higher than historic lows but still manageable with the right strategy.

👉 Smart move: Focus on affordability, not timing the market.

---Disclaimer: Rates vary by lender and borrower profile.

Ahmada Ndao is a financial research analyst and independent journalist

specializing in US consumer finance, legal rights, and insurance markets.

With over 5 years covering American financial products, he has helped

thousands of readers navigate complex insurance decisions, find the right

legal representation, and optimize their credit strategies. His research

methodology combines primary data analysis, direct outreach to industry

professionals, and continuous monitoring of federal regulatory changes.

Ahmada’s work has been cited by financial communities across the US and

reviewed by licensed attorneys and insurance professionals for accuracy.