Best Homeowners Insurance USA 2026 — Top Companies, Average Costs & How to Save

Your home is likely your single largest financial asset — yet millions of American homeowners are either underinsured, overpaying, or both. The homeowners insurance market has changed dramatically in recent years: premiums have risen 20–35% since 2022 driven by climate-related losses, inflation in construction costs, and insurer withdrawals from high-risk states. Choosing the right company and coverage in 2026 requires more research than ever before. This guide ranks the best homeowners insurance companies in the USA, explains exactly what coverage you need, and gives you a proven framework to save $300–$700 per year without sacrificing protection.

Key Facts — Homeowners Insurance USA 2026

- Average annual premium: $2,285/year ($190/month) nationally — up 23% since 2022

- Most expensive states: Florida ($4,218), Oklahoma ($3,900), Texas ($3,600), Louisiana ($3,400)

- Most affordable states: Hawaii ($578), Delaware ($841), Vermont ($900)

- Best overall insurer: Amica Mutual — highest customer satisfaction, lowest complaint ratio

- Best for affordability: USAA (military only) or Erie Insurance

- 65% of homes in the USA are underinsured by an average of 22% — critical coverage gap

- Required by mortgage lenders — your lender will force-place expensive coverage if you let your policy lapse

- Bundle discounts of 15–25% available when combining with auto insurance

The 8 Best Homeowners Insurance Companies USA — 2026

We evaluated insurers across six criteria: J.D. Power customer satisfaction scores, AM Best financial strength ratings, average premium competitiveness, claims handling speed and fairness, coverage options and riders, and complaint ratios from the National Association of Insurance Commissioners (NAIC).

| Company | Best For | AM Best | J.D. Power | Avg. Annual Premium | Score |

|---|---|---|---|---|---|

| Amica Mutual Editor's Pick | Customer satisfaction, claims | A+ | 906/1000 ★ | $1,800–$2,200 | ⭐ 4.9/5 |

| USAA Military Only | Military families — best rates | A++ | 884/1000 | $1,500–$1,900 | ⭐ 4.9/5 |

| Erie Insurance | Best value, Midwest/East | A+ | 856/1000 | $1,600–$2,000 | ⭐ 4.7/5 |

| State Farm | Largest network, all states | A++ | 829/1000 | $1,900–$2,500 | ⭐ 4.5/5 |

| Allstate | Digital tools, broad availability | A+ | 815/1000 | $2,000–$2,800 | ⭐ 4.3/5 |

| Nationwide | Unique coverages, older homes | A+ | 820/1000 | $1,800–$2,400 | ⭐ 4.4/5 |

| Chubb | High-value homes, luxury coverage | A++ | 847/1000 | $3,000–$6,000+ | ⭐ 4.7/5 |

| Lemonade | Tech-forward, instant claims | A | N/A (newer) | $1,400–$2,000 | ⭐ 4.2/5 |

Amica Mutual has ranked #1 in J.D. Power's homeowners insurance customer satisfaction study for more than a decade — a remarkable consistency that reflects genuine operational excellence in claims handling and customer service. As a mutual company, Amica is owned by its policyholders and pays annual dividends that effectively reduce your net premium by 5–20%. Their claims representatives are direct employees (not outsourced adjusters), and their complaint ratio is among the lowest in the industry. Premiums are competitive but not always the cheapest — the value is in claims experience when you need it most. Get a quote at Amica.com.

✓ Pros

- #1 J.D. Power customer satisfaction 10+ years

- Annual dividend payments — net premium reduction

- Lowest complaint ratio in the industry

- Direct claims employees — not outsourced

- Excellent for complex or large claims

✗ Cons

- Not available in all states

- Online quote process less streamlined than competitors

- May not be cheapest premium in your market

For the roughly 13 million Americans eligible for USAA membership (active military, veterans, and their immediate families), USAA offers the best combination of price and service in the homeowners insurance market. USAA premiums average 15–30% below comparable coverage from national insurers, with an A++ AM Best rating and customer satisfaction scores that consistently rival Amica. Their military-specific coverages — including protection for uniforms and equipment — and understanding of deployment-related situations make them uniquely valuable for servicemembers. If you are eligible, USAA is almost always the right choice. Learn more at USAA.com.

✓ Pros

- 15–30% below market average premiums

- A++ AM Best — highest financial strength

- Military-specific coverages included

- Outstanding claims satisfaction

✗ Cons

- Eligibility limited to military community

- No local agents — fully direct

Erie Insurance offers the best combination of price and coverage breadth among regional insurers — and for homeowners in their 12-state coverage area, it regularly beats national insurers on both price and claims experience. Erie's standard policy includes several coverages that competitors charge extra for: guaranteed replacement cost, identity theft protection, and service line coverage. Their local independent agent model means personalized service and a knowledgeable advisor who knows your local market. Get a quote through a local Erie agent at ErieInsurance.com.

✓ Pros

- Competitive premiums — often below national average

- Guaranteed replacement cost standard

- Identity theft protection included

- Strong local agent network

✗ Cons

- Only 12 states — not available nationally

- Requires working through an agent

What Does Homeowners Insurance Cover? The 6 Core Coverages

A standard homeowners insurance policy (HO-3 — the most common form) includes six distinct coverage components. Understanding each is essential to knowing whether you are properly protected:

Coverage A — Dwelling Most Important

Covers the physical structure of your home — walls, roof, floors, built-in appliances, and attached structures like garages. This is the most critical coverage: it must reflect the full replacement cost of rebuilding your home from scratch at current construction prices — not its market value. With construction costs up 35% since 2020, many policies are severely underinsured here. Always insure at 100% of replacement cost, not market value.

Coverage B — Other Structures

Covers detached structures on your property — fences, detached garages, sheds, pool houses. Typically set at 10% of your dwelling coverage automatically. If you have significant outbuildings, verify this limit is sufficient.

Coverage C — Personal Property

Covers your belongings — furniture, electronics, clothing, appliances — against covered perils. Standard coverage is 50–70% of dwelling coverage. Important distinction: standard policies cover personal property at actual cash value (depreciated). Upgrading to replacement cost value for personal property typically adds $50–$100/year but pays out what it actually costs to replace items today — always worth the upgrade.

Coverage D — Additional Living Expenses (ALE)

Pays for hotel, meals, and temporary housing if your home becomes uninhabitable due to a covered loss. Typically 20–30% of dwelling coverage. Critical for families — hotel and living costs after a major loss can exceed $5,000–$10,000/month in many markets.

Coverage E — Liability Protection

Pays for legal defense and damages if someone is injured on your property or you accidentally damage someone else's property. Standard coverage is $100,000 — often dangerously insufficient. Most homeowners should carry $300,000–$500,000 in liability coverage, or supplement with a personal umbrella policy. For context, a serious dog bite or slip-and-fall lawsuit easily exceeds $100,000. See our personal injury guide for typical lawsuit values.

Coverage F — Medical Payments to Others

Pays small medical bills (typically $1,000–$5,000) for guests injured on your property regardless of fault — helping prevent minor incidents from becoming lawsuits. A goodwill coverage that costs very little and provides meaningful protection.

What Homeowners Insurance Does NOT Cover — Critical Gaps

Standard homeowners policies have significant exclusions that surprise many homeowners at claim time. Know these gaps before you need them:

- Floods: Not covered under any standard homeowners policy — requires a separate flood insurance policy through the National Flood Insurance Program (NFIP) or private flood insurer. Over 40% of flood claims occur outside high-risk flood zones. Average NFIP policy: $700–$900/year.

- Earthquakes: Excluded from standard policies. Separate earthquake insurance required — critical in California, Pacific Northwest, and New Madrid Seismic Zone. Average California earthquake policy: $800–$2,000/year.

- Sewer backup and water line failure: Not covered unless you add a sewer backup rider (typically $50–$100/year — always worth adding). One sewer backup can cause $10,000–$50,000 in damage.

- Normal wear and tear: Insurance covers sudden accidental losses — not gradual deterioration, maintenance failures, or aging roofs. A 20-year-old roof that leaks is not covered; storm damage to a 20-year-old roof may be covered partially.

- Home business: Business equipment and liability from home-based businesses are excluded from standard coverage. A separate home business rider or commercial policy is needed.

- High-value items: Jewelry, art, collectibles, cameras, and firearms face sub-limits under standard Coverage C (typically $1,500 for jewelry, $2,500 for firearms). A separate scheduled personal property rider covers these items at full value.

⚠️ Florida, California & Texas Homeowners: The standard insurance market has deteriorated severely in these states. Multiple major insurers have exited Florida and California due to hurricane and wildfire losses. If your insurer cancels your policy or you cannot find coverage, your state's FAIR Plan provides coverage of last resort — but at significantly higher premiums with more limited coverage. Check your state insurance department at NAIC.org for current market resources.

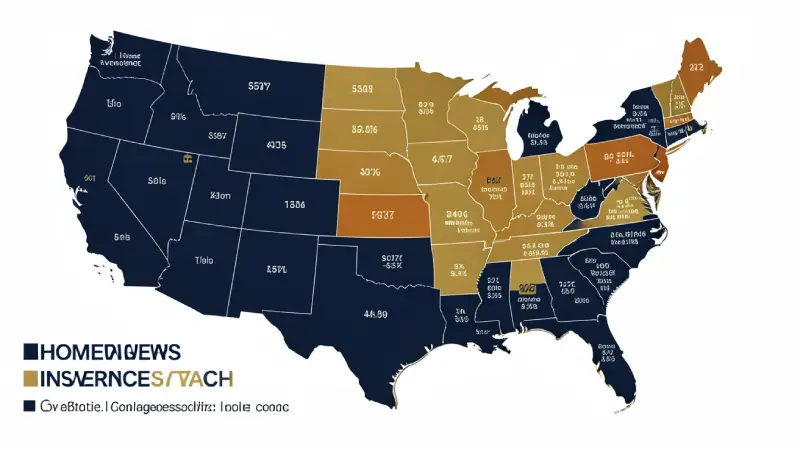

Homeowners Insurance Rates by State — 2026

| State | Avg. Annual Premium | vs. National Avg. | Primary Risk Factor |

|---|---|---|---|

| Florida Highest Risk | $4,218 | +85% | Hurricanes, sinkholes |

| Oklahoma | $3,900 | +71% | Tornadoes, hail |

| Texas | $3,600 | +58% | Hurricanes, hail, tornadoes |

| Louisiana | $3,400 | +49% | Hurricanes, flooding |

| Kansas | $3,100 | +36% | Tornadoes, hail |

| California | $2,100 | -8% | Wildfires (varies widely) |

| New York | $1,700 | -26% | Winter storms, flooding |

| Illinois | $2,000 | -12% | Tornadoes, hail |

| Pennsylvania | $1,500 | -34% | Winter storms |

| Hawaii Lowest | $578 | -75% | Low storm frequency |

How to File a Homeowners Insurance Claim — Step by Step

Most homeowners file fewer than one claim per decade — making the claims process unfamiliar precisely when you are most stressed. Here is the correct procedure to maximize your claim:

- Ensure safety first. If the damage involves structural collapse, gas leaks, or electrical hazards, evacuate and call 911 before anything else. Your insurer will cover temporary housing under Coverage D.

- Document all damage immediately. Photograph and video every affected area before any cleanup or repairs. Date-stamped photos are critical evidence. Use cloud storage to back up immediately.

- Prevent further damage. You have a legal duty to mitigate damage — board up broken windows, tarp a damaged roof, extract standing water. Keep all receipts for emergency protective measures — they are reimbursable.

- Contact your insurer within 24–48 hours. Most policies have prompt notification requirements. Delays can complicate claims. File online, via app, or by phone — get a claim number immediately.

- Do NOT authorize permanent repairs before an adjuster inspects. Wait for the adjuster to document damage before contractors begin permanent work. Emergency temporary repairs are fine.

- Create a home inventory of damaged personal property. List every damaged item with estimated replacement cost, age, and original purchase price if known. Photos and receipts strengthen personal property claims significantly.

- Review the settlement offer carefully. If the insurer's settlement seems low, you have the right to negotiate, request re-inspection, or hire a public adjuster to advocate on your behalf. For major disputes, consult your state's insurance commissioner through the NAIC consumer resources.

10 Proven Ways to Save on Homeowners Insurance in 2026

💰 Savings Strategies — Average Annual Savings Each

- Bundle with auto insurance: Save 15–25% by purchasing home and auto from the same insurer. Average savings: $200–$400/year. See our auto insurance guide for the best bundling options.

- Raise your deductible: Increasing from $1,000 to $2,500 typically reduces premiums 10–15%. Only do this if you have $2,500 in emergency savings to cover it. Average savings: $150–$300/year.

- Install safety and security features: Smoke detectors, deadbolt locks, burglar alarms, and sprinkler systems each earn discounts of 2–10%. A monitored security system can save $100–$200/year.

- Improve your credit score: Most states allow insurers to use credit-based insurance scores in pricing. Improving from fair to good credit can reduce premiums 15–30%. See our mortgage guide for credit score improvement strategies.

- Shop and compare every 2–3 years: Loyalty does not pay in home insurance — insurers price new customers better. Getting 3–4 competing quotes at renewal is the single most reliable way to save. Use Policygenius or Insurify to compare multiple quotes simultaneously.

- Avoid small claims: Filing claims under $3,000–$5,000 often costs more in premium increases than the payout. Pay small repairs out-of-pocket and reserve insurance for major losses.

- New roof discount: A new roof (especially impact-resistant shingles) can reduce premiums 20–40% in hail and wind-prone areas. If your roof is over 15 years old, replacing it before renewal can pay for itself in 5–7 years of premium savings.

- Claim-free discount: Many insurers offer 5–10% discounts for staying claim-free for 3–5 years. Ask your insurer about claim-free or loyalty discount programs.

- Retire or pay off your mortgage: Some insurers offer discounts for retired homeowners (home is monitored more) and for mortgage-free homes.

- Eliminate unnecessary coverage: Review your policy annually — if you've downsized belongings, lower your personal property limits. Remove riders for items you no longer own.

How Much Homeowners Insurance Do You Actually Need?

The most dangerous homeowners insurance mistake is underinsurance — and 65% of American homes are underinsured by an average of 22%. Here is how to calculate proper coverage for each component:

Dwelling Coverage (Coverage A) — The Critical Number

Insure at full replacement cost — what it would cost to completely rebuild your home from scratch at today's construction prices. This is not your market value, purchase price, or outstanding mortgage. With construction costs up 35% since 2020, replacement costs now routinely exceed market values in many areas. Use an online replacement cost estimator or ask your insurer to conduct a formal replacement cost appraisal. Underinsuring your dwelling by 20% means you bear 20% of any major claim personally.

Liability Coverage (Coverage E) — Often Dangerously Low

The default $100,000 liability limit is insufficient for most households in 2026. A swimming pool, dog, frequent guests, or a home-based business increases your liability exposure substantially. We recommend a minimum of $300,000 in liability coverage. For higher net-worth households, supplementing with a personal umbrella policy ($1M–$5M in additional liability coverage for roughly $200–$400/year) is strongly recommended. Umbrella policies provide the best value in personal insurance. For context on what injury lawsuits actually cost, see our personal injury settlement guide.

Personal Property — Upgrade to Replacement Cost

Always select replacement cost value (RCV) rather than actual cash value (ACV) for personal property. ACV pays out depreciated value — a 5-year-old laptop worth $200 at depreciated value costs $800 to replace. RCV pays the current replacement cost. The upgrade typically costs $50–$100/year and is always worth it.

Annual Homeowners Insurance Review Checklist

- Verify dwelling coverage reflects current replacement cost (adjust after renovations or rising construction costs)

- Confirm personal property coverage reflects current belongings — update after major purchases

- Review liability limits — increase to $300,000+ minimum; consider umbrella policy

- Check for coverage gaps — flood, earthquake, sewer backup based on your location

- Update scheduled personal property riders for new jewelry, art, or valuables

- Get 3 competing quotes at renewal — never auto-renew without shopping

- Ask about available discounts you may qualify for

- Verify your insurer's AM Best rating has not declined (A or above required)

- Review your deductible — adjust based on your current emergency fund level

- Check state insurance department for complaint ratios: NAIC.org

FAQ — Best Homeowners Insurance USA 2026

Ahmada Ndao is a financial research analyst and independent journalist

specializing in US consumer finance, legal rights, and insurance markets.

With over 5 years covering American financial products, he has helped

thousands of readers navigate complex insurance decisions, find the right

legal representation, and optimize their credit strategies. His research

methodology combines primary data analysis, direct outreach to industry

professionals, and continuous monitoring of federal regulatory changes.

Ahmada’s work has been cited by financial communities across the US and

reviewed by licensed attorneys and insurance professionals for accuracy.