Best Family Health Insurance Plans USA 2026 — Top Coverage, Costs & How to Choose the Right Plan

Choosing a family health insurance plan is one of the highest-stakes financial decisions American families make every year — yet most families make it in under 20 minutes by defaulting to the cheapest premium. The result: wrong plan types, unexpected out-of-pocket costs, and coverage gaps that cost families thousands of dollars when they actually need care. With the average family of four spending $25,000 per year on healthcare — and the ACA marketplace offering subsidies that many families leave unclaimed — getting this decision right can save $3,000–$8,000 annually. This guide ranks the best family health insurance plans and providers for 2026, explains the true cost structure for families, and gives you a precise framework to choose optimal coverage for your family's specific health needs.

Key Facts — Family Health Insurance USA 2026

- Average family premium: $1,437/month ($17,244/year) for employer-sponsored coverage

- Average ACA marketplace family premium: $1,152/month before subsidies

- Family out-of-pocket maximum 2026: $18,900 — your worst-case annual exposure

- Best overall for families: Kaiser Permanente — highest NCQA ratings, lowest premiums where available

- Best nationwide for families: Blue Cross Blue Shield — all 50 states, widest pediatric network

- ACA family subsidies: Available up to 400%+ FPL — a family of 4 earning $93,600 may qualify

- CHIP covers children in families earning too much for Medicaid — millions eligible don't enroll

- Family deductible structure: Embedded vs. aggregate — critical difference most families misunderstand

Best Family Health Insurance Providers USA — 2026 Rankings

We evaluated family health insurance providers across six criteria: pediatric network breadth, family out-of-pocket maximums, NCQA quality ratings, ACA marketplace availability, maternity and newborn coverage, and mental health parity compliance — all factors uniquely important for families versus individual enrollees.

| Provider | Best For | States | NCQA | Avg. Family Premium | Score |

|---|---|---|---|---|---|

| Kaiser Permanente Best Overall | Integrated family care, lowest premiums | 8 + DC | 4.5/5 ★ | $900–$1,200/mo | ⭐ 4.9/5 |

| Blue Cross Blue Shield | Nationwide, widest pediatric network | All 50 | 4.0/5 | $1,100–$1,600/mo | ⭐ 4.8/5 |

| UnitedHealthcare | Largest provider network, employer plans | All 50 | 3.5/5 | $1,200–$1,700/mo | ⭐ 4.5/5 |

| Aetna (CVS Health) | Maternity, pediatric care integration | All 50 | 3.8/5 | $1,100–$1,500/mo | ⭐ 4.5/5 |

| Cigna | Specialist access, chronic conditions | All 50 | 3.6/5 | $1,100–$1,600/mo | ⭐ 4.4/5 |

| Molina Healthcare | Low-income families, Medicaid expansion | 19 states | 3.5/5 | $600–$900/mo | ⭐ 4.2/5 |

| Oscar Health | Young families, tech-forward tools | 18 states | 3.8/5 | $950–$1,300/mo | ⭐ 4.3/5 |

Kaiser Permanente is the best family health insurance provider in the USA — delivering the highest NCQA quality ratings nationally for over a decade, premiums 15–25% below comparable plans, and an integrated care model that is uniquely suited to families. With Kaiser, your family's pediatrician, OB/GYN, specialists, lab, pharmacy, and hospital are all coordinated within one system — eliminating the referral confusion, duplicate tests, and communication gaps that plague fragmented care. Preventive care, childhood vaccinations, well-child visits, and developmental screenings are all streamlined. Mental health services for children and adolescents — one of the most important and most often inadequately covered areas for families — are well-integrated in Kaiser's system. If Kaiser is available in your area, it is almost always the best choice for families. Learn more at KP.org.

✓ Pros

- Highest NCQA quality ratings nationally

- Premiums 15–25% below market

- Integrated pediatric + specialist care

- Best mental health parity for children

- Seamless maternity and newborn care

✗ Cons

- Only 8 states + DC

- Must use Kaiser's own doctors

- Limited out-of-network coverage

Blue Cross Blue Shield is the best family health insurance choice for the 42 states where Kaiser is not available — offering all 50-state coverage, the largest pediatric physician and children's hospital network in the country, and every plan type at every ACA metal tier. BCBS is the insurer of choice for most children's hospitals nationally, making it the safest choice for families with children who have complex medical needs or may need specialized pediatric care. The BlueCard program provides seamless coverage when your family travels or when children go away to college. Find your local plan at BCBS.com.

✓ Pros

- All 50 states — available everywhere

- Largest pediatric and children's hospital network

- BlueCard — nationwide coverage when traveling

- Every plan type and metal tier available

- Strong maternity and newborn coverage

✗ Cons

- Quality varies significantly by regional affiliate

- PPO family plans can be expensive

- Not always cheapest premium option

Family Health Insurance Plan Types — Which Is Right for Your Family?

HMO — Best Value for Families with Young Children

An HMO requires choosing a primary care pediatrician who coordinates all your children's care and provides referrals for specialists. Coverage is limited to the HMO network. For families with young children who primarily use well-child visits, vaccinations, and occasional sick visits — all handled by the pediatrician — an HMO delivers the lowest total cost. Premium savings of $200–$400/month versus PPO are significant for families.

PPO — Best for Families with Specialist Needs

A PPO allows your family to see any doctor — in-network or out-of-network — without referrals. Ideal for families with children who have ongoing specialist needs: pediatric cardiologists, neurologists, oncologists, developmental pediatricians, or any specialized care that may require seeing multiple providers. The premium cost is significantly higher, but for families managing complex pediatric conditions, the flexibility is essential.

HDHP + HSA — Best for Healthy Families with High Income

A High Deductible Health Plan paired with a Health Savings Account offers the lowest premiums and triple-tax-advantaged savings — but requires paying the full deductible ($3,300+ for families in 2026) before most coverage kicks in. The 2026 family HSA contribution limit is $8,550. Best for families who are generally healthy, have adequate emergency savings to cover the deductible, and want to invest HSA funds for future healthcare costs. Risky for families with unpredictable or high healthcare usage.

The Critical Family Deductible Issue — Embedded vs. Aggregate

This is one of the most misunderstood aspects of family health insurance — and it costs families thousands of dollars in unexpected bills every year.

Aggregate Deductible — The Risky Structure

With an aggregate deductible, the entire family deductible (e.g., $6,000) must be met before insurance pays for any family member. If your deductible is $6,000 and your child needs surgery costing $8,000, you pay the first $6,000 — even though your child individually might have a $3,000 individual deductible listed on the plan. This structure can expose individual family members to the full family deductible amount.

Embedded Deductible — The Safer Structure

With an embedded deductible, each family member has their own individual deductible limit within the family plan. Once any individual meets their individual deductible (e.g., $3,000), insurance begins paying for that person — even if the family aggregate hasn't been met. This is significantly safer for families with one member who has high medical costs. Always ask specifically whether a family plan has an embedded or aggregate deductible before enrolling.

💡 Embedded Deductible Rule: Under ACA rules, all non-grandfathered family plans must have an embedded individual deductible that does not exceed the 2026 HDHP threshold of $1,650. This means most ACA-compliant family plans have embedded deductibles — but always verify, especially for employer-sponsored plans that may have different structures.

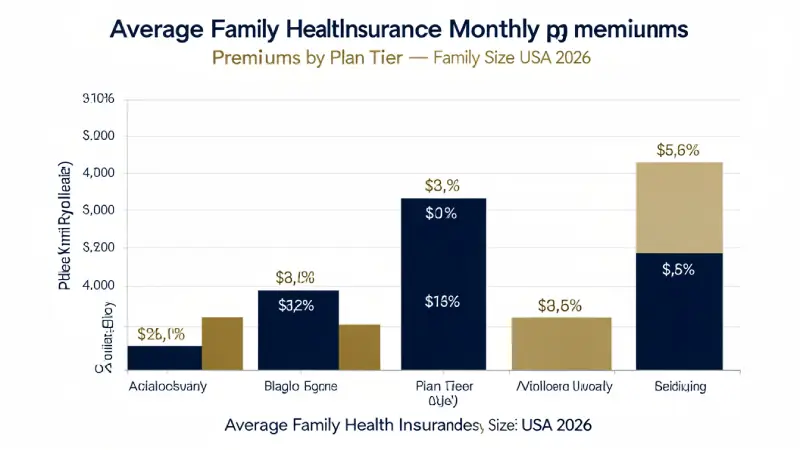

Family Health Insurance Costs — 2026 Breakdown

| Plan Tier | Family of 3 (35yr adult) | Family of 4 (35yr adult) | Family of 5 | Insurer Pays |

|---|---|---|---|---|

| Bronze | $850–$1,050/mo | $1,000–$1,250/mo | $1,100–$1,400/mo | 60% |

| Silver Most Popular | $1,050–$1,300/mo | $1,200–$1,500/mo | $1,350–$1,700/mo | 70% |

| Gold | $1,350–$1,700/mo | $1,550–$1,950/mo | $1,750–$2,200/mo | 80% |

| Platinum | $1,700–$2,100/mo | $1,950–$2,450/mo | $2,200–$2,750/mo | 90% |

*Before subsidies. Premiums vary by state, insurer, and plan. Source: KFF Health Insurance Marketplace Calculator, March 2026.

ACA Subsidies for Families — How Much Can You Save?

Family of 4 ACA Subsidy Examples — 2026 (Before Subsidies: ~$1,400/mo Silver)

The ACA's Cost-Sharing Reductions (CSR) add even more value for families earning 100–250% of the federal poverty level — reducing deductibles, copays, and out-of-pocket maximums on Silver plans to near-Platinum levels. A family of four earning $62,400 enrolling in a Silver CSR plan may have a family deductible as low as $300 and an out-of-pocket maximum as low as $2,900. This is the most powerful — and least used — benefit in the ACA. Apply only through Healthcare.gov or your state marketplace.

CHIP — Free or Low-Cost Coverage for Children

The Children's Health Insurance Program (CHIP) covers children in families that earn too much for Medicaid but too little for affordable marketplace coverage — typically households earning 200–300% of the federal poverty level, depending on state. CHIP covers doctor visits, dental, vision, hospitalizations, prescriptions, and emergency care for eligible children at zero or minimal cost to families.

An estimated 5 million eligible children are not enrolled in CHIP. A family of four earning up to $62,400–$78,000 in most states may qualify for their children — while parents purchase marketplace coverage separately. This combination often costs significantly less than a single family plan. Apply year-round at InsureKidsNow.gov — CHIP has no open enrollment deadline.

How to Choose the Right Family Health Insurance Plan — 10 Factors

- Verify your pediatrician and family doctors are in-network. Losing your child's established pediatrician is disruptive and medically risky. Always confirm in-network status before switching plans — don't assume.

- Check children's hospital access. If your area has a major children's hospital (Children's Hospital of Philadelphia, Texas Children's, Boston Children's, etc.), confirm it is in-network. Out-of-network children's hospital care can exceed $50,000 per stay.

- Understand embedded vs. aggregate deductible. Ask specifically which structure applies. For families where one member has high medical costs, embedded deductible plans are safer.

- Review mental health and behavioral health coverage. Pediatric mental health needs have risen dramatically — ensure your plan covers therapy, psychiatry, and behavioral health at parity with physical health coverage.

- Verify maternity and newborn coverage. If you plan to have more children, confirm maternity coverage including prenatal visits, labor and delivery, and newborn care. ACA plans must cover maternity, but coverage quality varies.

- Check prescription drug formulary. If any family member takes regular medications, verify they are on the plan's formulary at a favorable tier. A single medication moving from Tier 2 to Tier 3 can add $1,200–$3,600/year in costs.

- Calculate total annual cost — not just premium. (Annual premium) + (expected out-of-pocket based on your family's typical healthcare use) = true total cost. A Gold plan at $1,600/mo often beats a Bronze plan at $1,100/mo for families who use healthcare regularly.

- Check your ACA subsidy eligibility. Use the KFF Subsidy Calculator — many families significantly overestimate their premiums without accounting for subsidies.

- Evaluate dental and vision for children. ACA plans are required to offer pediatric dental and vision as essential health benefits — but they may be separate add-ons rather than included. Confirm coverage and whether you need a standalone pediatric dental plan.

- Assess telehealth options. For families with young children, telehealth access (same-day virtual sick visits, pediatric advice lines) reduces ER visits and missed work. Confirm your plan's telehealth availability and cost.

Family-Specific Coverage That Must Be in Every Plan

The ACA requires all marketplace and most employer plans to cover these essential health benefits for families — but coverage depth varies significantly between plans:

- Pediatric preventive care: Well-child visits (0–21 years), developmental screenings, childhood vaccinations — all at 100% coverage before deductible on ACA-compliant plans

- Maternity and newborn care: Prenatal visits, labor and delivery, postpartum care, newborn hospitalization — covered but cost-sharing varies significantly by plan

- Pediatric dental and vision: Required as essential health benefit under ACA — may be embedded in the medical plan or offered as a separate benefit

- Mental health and behavioral health: Required at parity with physical health coverage — therapy, psychiatric care, substance use treatment for all family members including children

- Preventive screenings: Adolescent depression screening, obesity screening, hearing and vision screening for children — all covered at 100% on ACA plans

Family Health Insurance Selection Checklist 2026

- Confirm pediatrician and all current family doctors are in-network

- Verify children's hospital in-network access for your area

- Determine embedded vs. aggregate deductible structure

- Check all family prescriptions on formulary at favorable tier

- Calculate total annual cost (premium + expected OOP)

- Check ACA subsidy eligibility at Healthcare.gov

- Evaluate CHIP eligibility for children separately

- Review mental health and behavioral health coverage for children

- Confirm maternity coverage if planning additional children

- Verify pediatric dental and vision coverage included

- Check telehealth access and after-hours pediatric options

- Compare NCQA quality ratings at NCQA.org

FAQ — Best Family Health Insurance Plans USA 2026

Ahmada Ndao is a financial research analyst and independent journalist

specializing in US consumer finance, legal rights, and insurance markets.

With over 5 years covering American financial products, he has helped

thousands of readers navigate complex insurance decisions, find the right

legal representation, and optimize their credit strategies. His research

methodology combines primary data analysis, direct outreach to industry

professionals, and continuous monitoring of federal regulatory changes.

Ahmada’s work has been cited by financial communities across the US and

reviewed by licensed attorneys and insurance professionals for accuracy.