Best Workers Compensation Insurance USA 2026 — Top 8 Providers, Real Costs by Industry & State Requirements Explained

Operating a business with employees and no workers' compensation insurance is not a risk — it is a legal violation in 49 states that carries personal liability for every workplace injury plus fines up to $100,000 per day. Yet the National Council on Compensation Insurance (NCCI) estimates that 20% of employers with legally required workers' comp coverage are either uninsured, underinsured, or misclassifying employees to reduce premiums — creating catastrophic exposure they don't discover until an injury forces a claim. Workers' compensation insurance is the most legally consequential coverage a business owner purchases. This guide ranks the best workers' compensation insurance companies in the USA for 2026, provides real cost data by industry and state, explains every state's requirements, and identifies the classification and compliance mistakes that generate the most expensive surprises.

Key Facts — Workers Compensation Insurance USA 2026

- Mandatory in 49 states for businesses with employees — Texas is the only opt-out state

- Best overall: The Hartford — A+, #1 J.D. Power, fastest claims resolution, RTW programs

- Best price for small business: Next Insurance — from $85/month, instant digital coverage

- Average cost: $1.00–$2.25 per $100 of payroll for office workers; $7–$14 per $100 for construction

- Employee misclassification is the #1 audit trigger — and carries back-premium plus penalties

- Experience Modification Rate (EMR) — every claim permanently affects your future premiums

- Most expensive claim type: Back injuries — average $80,000 per claim including lost wages

- Return-to-work programs reduce claim costs by 30–40% — most small businesses don't use them

Best Workers Compensation Insurance Companies USA 2026 — Full Rankings

| Rank | Provider | AM Best | Best For | States | RTW Program | Score |

|---|---|---|---|---|---|---|

| #1 | The Hartford Editor's Choice | A+ | Most businesses | All 50 | ✅ Industry-leading | 4.9/5 |

| #2 | Travelers | A++ | Large employers, RTW focus | All 50 | ✅ Best in class | 4.8/5 |

| #3 | Zurich | A+ | Large & mid-size employers | All 50 | ✅ Strong | 4.7/5 |

| #4 | Liberty Mutual | A | Multi-state employers | All 50 | ✅ Good | 4.6/5 |

| #5 | Next Insurance | A- | Small biz, lowest cost | All 50 | Basic | 4.5/5 |

| #6 | Nationwide | A+ | Agriculture, specialty | All 50 | ✅ Good | 4.5/5 |

| #7 | AmTrust Financial | A- | Small business specialist | All 50 | Basic | 4.3/5 |

| #8 | ICW Group | A+ | California focus | CA + select | ✅ Strong CA | 4.3/5 |

The Hartford's workers' compensation program is built around one core philosophy: the fastest path to recovery is the cheapest claim. Their nurse case manager model, 24-hour claim reporting line, and integrated pharmacy management reduce both claim duration and total cost more effectively than any competitor in their size tier. Their SafetyWorks! program provides free online safety training, workplace assessment tools, and OSHA compliance resources to policyholders — reducing claim frequency before injuries occur. For businesses in high-risk industries, proactive safety support is as valuable as claims response. Get a quote at TheHartford.com.

✓ Why The Hartford Wins

- Nurse case manager on every significant claim

- #1 J.D. Power workers' comp satisfaction

- 24-hour claim reporting — fastest response

- Free SafetyWorks! program reduces claim frequency

- A+ AM Best — 215-year payment track record

- Integrated pharmacy management reduces Rx costs

✗ Limitations

- Not cheapest for micro-businesses

- Premium surcharges in high-EMR businesses

- Agent-based for complex accounts

Travelers brings A++ financial strength to workers' compensation with an unmatched return-to-work infrastructure. Their dedicated RTW coordinators work directly with treating physicians and employers to design modified duty programs that return injured workers to productive employment faster — reducing total indemnity costs while maintaining employee morale and retention. Their risk control services include on-site ergonomic assessments, lifting technique training, and industry-specific safety programs that directly reduce claim frequency for manufacturers, distributors, and contractors. Contact via broker or at Travelers.com.

✓ Why Travelers Wins RTW

- A++ AM Best — maximum financial strength

- 37% reduction in average lost-time days

- Dedicated RTW coordinators per claim

- On-site ergonomic and safety assessments

- Best for manufacturing, distribution, contractors

✗ Limitations

- Higher minimum premiums than small biz options

- Claims satisfaction slightly below Hartford

- Better for mid-large employers than micro-business

Next Insurance's workers' compensation policies start at $85/month for small businesses — covering medical expenses, lost wages, and employer liability for workplace injuries. Their 1,300+ industry classification system ensures your business is rated accurately rather than defaulting to a high-risk generic class. Same-day coverage activation and instant certificate issuance make Next the fastest solution for businesses that need to prove compliance for a contract or state audit immediately. Apply at NextInsurance.com.

✓ Why Next Wins Small Business

- Lowest premiums — from $85/month

- Same-day coverage, instant certificate

- Accurate industry classification — no overpayment

- Fully digital — no broker or paper forms

✗ Limitations

- A- rating — below Hartford/Travelers tier

- Basic RTW support — no dedicated coordinator

- Not for large employers or high-hazard industries

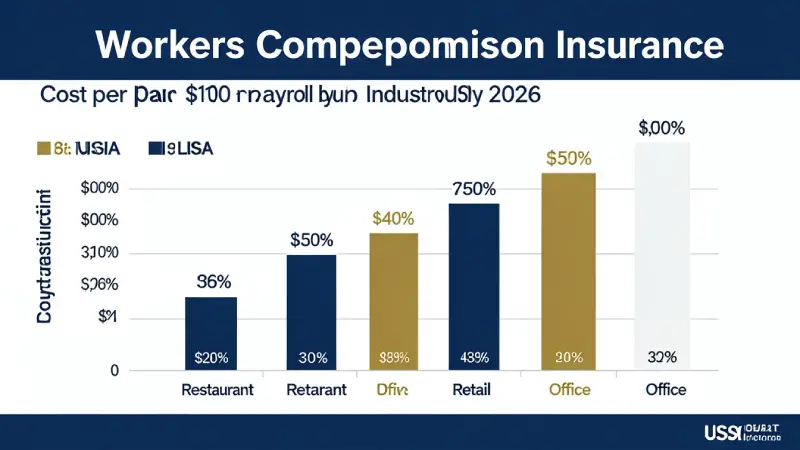

Workers Compensation Insurance Costs by Industry — March 2026

Workers' compensation premiums are calculated as a rate per $100 of payroll — not a flat fee. Your industry classification code (NCCI class code) determines your base rate. Here are the March 2026 average rates across the major industry categories:

| Industry / Class | Rate per $100 Payroll | Example: $500K Payroll | Risk Level |

|---|---|---|---|

| Clerical / Office Workers | $0.75–$1.50 | $3,750–$7,500/yr | 🟢 Low |

| Retail Store Employees | $1.50–$3.00 | $7,500–$15,000/yr | 🟡 Moderate |

| Restaurant / Food Service | $2.50–$5.00 | $12,500–$25,000/yr | 🟡 Moderate-High |

| Warehouse / Distribution | $3.00–$6.00 | $15,000–$30,000/yr | 🟠 High |

| Manufacturing | $3.50–$8.00 | $17,500–$40,000/yr | 🟠 High |

| Landscaping / Grounds | $5.00–$9.00 | $25,000–$45,000/yr | 🔴 Very High |

| Construction Highest | $7.00–$14.00 | $35,000–$70,000/yr | 🔴 Highest |

💡 EMR Multiplier: The rates above are base rates. Your actual premium is multiplied by your Experience Modification Rate (EMR) — a score calculated from your 3-year claims history. EMR 1.0 = average. EMR 0.85 = 15% discount (fewer claims than average). EMR 1.25 = 25% surcharge (more claims). A business with $50,000 base premium and EMR 1.30 pays $65,000. Managing your EMR through injury prevention and return-to-work programs is the single most impactful way to reduce workers' comp costs year over year.

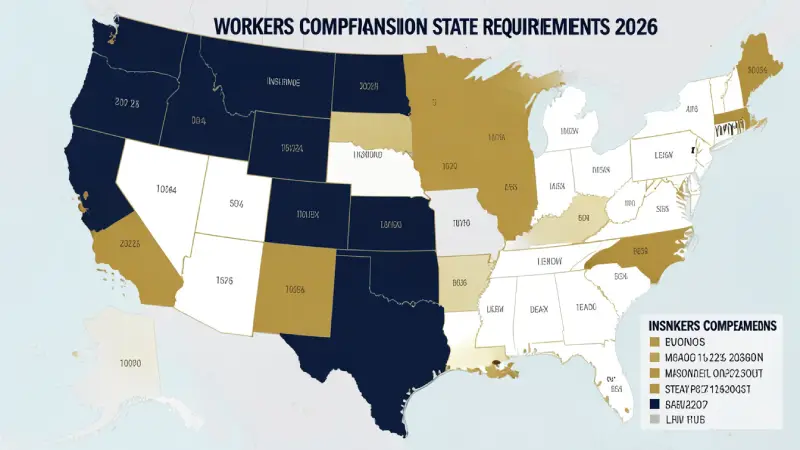

Workers Compensation State Requirements — What Your State Mandates

🔴 California

Required for ALL employers with 1+ employee. Fines: $10,000+ per violation plus personal liability. One of the highest premium states nationally. ICW Group and State Fund are CA-specific options.

🔴 New York

Required for ALL employers. Fines up to $50,000 for non-compliance plus $2,000/day. NY has its own state fund (NYSIF) as an alternative to private carriers.

🔴 Florida

Required for construction with 1+ employee, all other industries with 4+ employees. Fines: stop-work orders and $1,000/day. One of the most aggressively enforced states.

🟡 Illinois

Required for ALL employers with employees. Fines: $500/day for non-compliance. Self-insurance requires state approval and significant financial posting.

🟡 Pennsylvania

Required for most employers. SWIF (State Workers Insurance Fund) available as a last-resort option. Private market competitive for most industries.

🟢 Texas

Only opt-out state. Workers' comp is not mandatory — but non-subscribing employers lose key legal defenses and face full tort liability for any injury. Most Texas businesses still carry coverage.

The Experience Modification Rate (EMR) — How Your Claims History Permanently Affects Premiums

The Experience Modification Rate is the single most important number in workers' compensation — and the one most employers don't understand until it costs them tens of thousands of dollars in premium surcharges.

Your EMR is calculated annually by your state's rating bureau (NCCI in most states) based on your actual claims history compared to the expected claims for a business of your type and size. It applies as a direct multiplier to your base premium. Here is what this means in practice:

| EMR Score | Meaning | $40K Base Premium | Annual Impact |

|---|---|---|---|

| 0.75 | Far fewer claims than average | $30,000 | Save $10,000/yr |

| 0.85 | Below-average claims | $34,000 | Save $6,000/yr |

| 1.00 | Industry average | $40,000 | Baseline |

| 1.15 | Above-average claims | $46,000 | +$6,000/yr |

| 1.30 Danger | Significantly more claims | $52,000 | +$12,000/yr |

| 1.50+ | High-risk — may face non-renewal | $60,000+ | +$20,000+/yr |

How to improve your EMR: Implement a formal return-to-work program (reduces claim duration), conduct monthly safety meetings (reduces frequency), report every injury immediately (reduces claim escalation), work with a nurse case manager on every significant claim (reduces total cost). Businesses that actively manage EMR can reduce it from 1.30 to 0.85 within 3–5 policy years — translating to $18,000/year in premium savings on a $40,000 base.

Employee Classification — The Most Expensive Mistake in Workers' Comp

⚠️ Misclassification is the #1 workers' comp audit trigger. Every workers' compensation policy is subject to premium audit at year end. If your employees' actual job duties don't match the classification codes on your policy, your insurer recalculates your premium retroactively — and issues a bill for the underpayment plus administrative penalties. Common misclassification scenarios cost businesses $5,000–$50,000 in unexpected audit bills.

The most common misclassification mistakes:

- Classifying field workers as office workers — a contractor who codes estimators and project managers as clerical workers but they occasionally visit job sites. Clerical rate: $0.90/$100. Construction supervision rate: $8.50/$100. The difference on $300,000 payroll: $22,800.

- Misclassifying employees as independent contractors — the most audited situation. If workers have set schedules, use your equipment, or work exclusively for you, most states classify them as employees regardless of your contract language. Every audit that reclassifies a contractor as an employee triggers back premium plus penalties.

- Not separating payroll by class code — if a restaurant owner lumps all payroll under "restaurant worker" without separating managers, servers, cooks, and delivery drivers, they pay the highest applicable rate for the entire payroll. Proper separation can reduce premiums 15–25%.

Workers Compensation Insurance Checklist — 2026

- Verify state requirement — all states except Texas mandate coverage

- Confirm every employee (including part-time and seasonal) is covered

- Verify all job classifications match actual duties — avoid audit surprises

- Separate payroll by class code to avoid paying highest rate for all employees

- Implement a formal return-to-work program — reduces claim duration 37%

- Report every injury within 24 hours — late reporting escalates claim costs

- Request nurse case manager assignment on any claim above $5,000

- Review your EMR annually — dispute incorrect claims that inflate your rate

- AM Best minimum A- for any workers' comp insurer selected

- Get 3 quotes — Hartford + Next Insurance + state fund (if available)

- Review independent contractor status — misclassification = audit risk

- Post required workers' comp notices in workplace (legally required in most states)

FAQ — Workers Compensation Insurance USA 2026

Ahmada Ndao is a financial research analyst and independent journalist

specializing in US consumer finance, legal rights, and insurance markets.

With over 5 years covering American financial products, he has helped

thousands of readers navigate complex insurance decisions, find the right

legal representation, and optimize their credit strategies. His research

methodology combines primary data analysis, direct outreach to industry

professionals, and continuous monitoring of federal regulatory changes.

Ahmada’s work has been cited by financial communities across the US and

reviewed by licensed attorneys and insurance professionals for accuracy.