Best Health Insurance Australia 2026 — Top 8 Providers, Real Costs by State & How to Save AU$800+/Year

15.2 million Australians — 57% of the population — hold private health insurance in 2026. Despite universal access to Medicare, Australians purchase private health insurance to avoid public hospital waiting lists (which average 42 days for elective surgery nationally), access dental, optical, and physiotherapy services not covered by Medicare, and avoid the Medicare Levy Surcharge (MLS) that applies to higher-income earners without hospital cover. But with 37 registered private health insurers and thousands of individual policies in Australia, choosing the right cover is bewildering — and the wrong choice costs the average Australian family AU$840–$1,600 per year in excess premiums or inadequate coverage. This complete 2026 guide cuts through the confusion: the 8 best health insurers compared head-to-head, real costs by state and age, what you actually get for your premium, and how to find the cheapest policy that meets your specific needs.

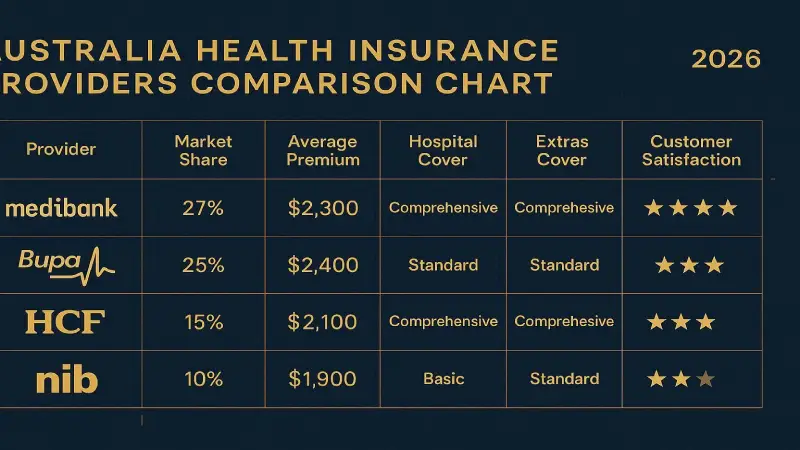

🏆 Top 8 Best Health Insurance Providers Australia 2026

| # | Provider | Members | Avg Annual Premium (Hospital+Extras) | FAIRER Rating | Best For |

|---|---|---|---|---|---|

| 🥇 1 | HCF | 1.9M | AU$1,980–$2,280 | ⭐⭐⭐⭐⭐ | Best value · Not-for-profit · Best claims satisfaction |

| 🥈 2 | Medibank | 3.7M | AU$2,080–$2,460 | ⭐⭐⭐⭐ | Largest insurer · Broadest hospital network |

| 🥉 3 | nib | 1.7M | AU$1,920–$2,240 | ⭐⭐⭐⭐ | Best digital experience · International workers |

| 4 | Bupa | 4.2M | AU$2,120–$2,520 | ⭐⭐⭐⭐ | Largest member base · Best dental network |

| 5 | Australian Unity | 0.5M | AU$1,860–$2,180 | ⭐⭐⭐⭐⭐ | Best wellness programme · Competitive pricing |

| 6 | Teachers Health | 0.35M | AU$1,780–$2,060 | ⭐⭐⭐⭐⭐ | Cheapest premium · Best for educators & health workers |

| 7 | CBHS (Corporate) | 0.1M | AU$1,720–$2,020 | ⭐⭐⭐⭐⭐ | Lowest claims rejection rate nationally |

| 8 | Defence Health | 0.12M | AU$1,680–$1,980 | ⭐⭐⭐⭐⭐ | Best for ADF members and families |

🔍 Why Australians Buy Private Health Insurance — 5 Real Reasons

Reason 1 — Avoiding Public Hospital Waiting Lists

The most practical driver of private health insurance uptake in Australia is the public hospital elective surgery waiting list. The national average wait for elective surgery in the public system was 42 days in 2025 — but for specific procedures, waits are far longer: knee replacements average 180 days, hip replacements 154 days, and cataract surgery 98 days. Private patients bypass these waiting lists entirely — surgery is scheduled around your availability, not the hospital's. For anyone who needs elective surgery and cannot afford to wait months, private hospital cover is the effective solution.

Reason 2 — Choice of Doctor and Hospital

Medicare covers public hospital treatment — but you do not choose your doctor, your hospital, or your admission timing in the public system. Private health insurance provides the right to choose your own surgeon, specialist, and preferred private hospital. This choice matters most for: specialist surgery where surgeon skill varies significantly, patients who have an established relationship with a specific specialist, and those undergoing complex or sensitive procedures where their comfort with the treating team is important.

Reason 3 — Medicare Does Not Cover Dental, Optical, or Allied Health

Medicare provides zero coverage for dental care (except limited emergency dental in some states), optical care (glasses, contact lenses, eye tests), physiotherapy, chiropractic, podiatry, psychology, occupational therapy, and most other allied health services. Extras cover (also called ancillary cover) in a private health policy covers these services — dental checkups, glasses, physio sessions, and other routine health services that most Australians use regularly. For an average Australian spending AU$600–$1,200 annually on dental and optical, extras cover can pay for itself through these benefits alone.

Reason 4 — Medicare Levy Surcharge Avoidance

The Medicare Levy Surcharge (MLS) is an additional 1.0–1.5% income tax levy applied to high-income earners without hospital cover. In 2026, the MLS applies to singles earning above AU$93,000 and families above AU$186,000. A single person earning AU$120,000 without hospital cover pays 1.25% × $120,000 = $1,500 in additional tax. Hospital-only cover from a fund like Teachers Health starts at approximately AU$1,200–$1,400 per year — making cover both cheaper than the surcharge and providing the actual insurance benefit as a bonus. For high-income earners, MLS avoidance alone often justifies the insurance premium.

Reason 5 — Lifetime Health Cover Loading

The Lifetime Health Cover (LHC) loading adds a 2% premium surcharge for each year you wait after age 31 to take out hospital cover — up to a maximum 70% loading. An Australian who first takes out private hospital cover at age 40 pays a 20% loading on their base premium permanently (until they have held cover for 10 continuous years). This government incentive strongly encourages earlier uptake — most financial advisors recommend taking out at least basic hospital cover by age 30 to avoid LHC loading accumulating.

📋 Hospital vs Extras — What Does Each Type of Cover Include?

Hospital Cover

Hospital cover pays for the cost of being treated as a private patient in a hospital. It covers: private hospital accommodation (private room), nursing care, theatre fees for surgery in a private hospital, intensive care, and the hospital's fees. Hospital cover does not pay for your doctor's fees — those are paid through a combination of Medicare Benefits Schedule (MBS) items and your doctor's charge, with an out-of-pocket gap if your doctor charges above the MBS fee. The gap between what Medicare pays and what your doctor charges is the "patient gap" — select doctors (called "no-gap" or "known-gap" doctors) limit or eliminate this gap payment. Hospital cover tiers — Gold, Silver, Bronze, Basic — determine which clinical categories are covered.

Extras Cover (Ancillary Cover)

Extras cover pays benefits for health services outside hospital: dental (checkups, fillings, crowns, orthodontics), optical (frames, lenses, contact lenses), physiotherapy, chiropractic, podiatry, psychology, occupational therapy, speech therapy, hearing aids, and in some policies natural therapies. Extras benefits are typically expressed as a benefit percentage (e.g., "80% of the cost up to the annual limit") and an annual limit per service category. Unused extras benefits do not typically carry over between policy years — use them or lose them. For most working Australians, the extras most frequently used are dental, optical, and physiotherapy — choose an extras cover that provides strong benefits in these categories.

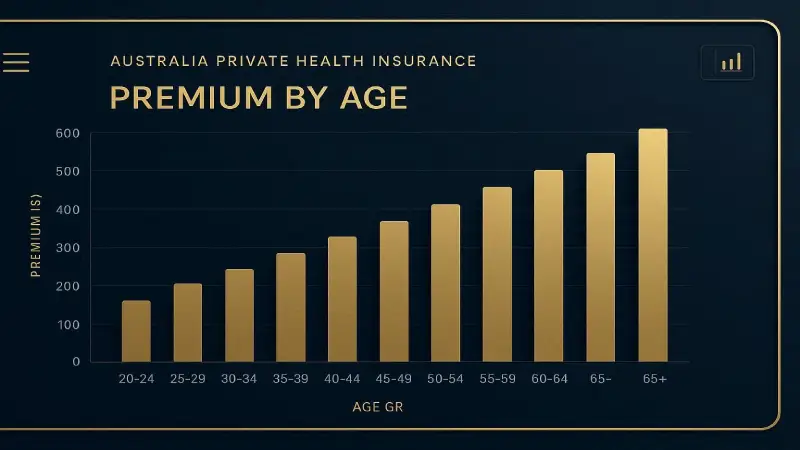

💰 Real Costs — Health Insurance Premiums by State and Age 2026

Australian private health insurance premiums are community-rated — meaning everyone of the same age pays the same base premium from a given fund for the same policy, regardless of health status. However, premiums vary by state (due to different hospital cost structures), age (community rating applies within ranges but the LHC loading affects older first-time purchasers), and hospital tier.

| Age | Gold Hospital (Single, NSW) | Silver Hospital | Bronze Hospital | Hospital + Mid Extras |

|---|---|---|---|---|

| 25–29 | AU$138–$165/mo | AU$105–$128/mo | AU$78–$95/mo | AU$195–$240/mo |

| 30–34 | AU$145–$172/mo | AU$110–$134/mo | AU$82–$100/mo | AU$205–$252/mo |

| 40–44 | AU$158–$188/mo | AU$120–$146/mo | AU$90–$109/mo | AU$222–$274/mo |

| 50–54 | AU$178–$212/mo | AU$135–$165/mo | AU$101–$123/mo | AU$250–$308/mo |

| 60–64 | AU$215–$256/mo | AU$163–$198/mo | AU$122–$148/mo | AU$302–$372/mo |

| 65+ | AU$248–$296/mo | AU$188–$228/mo | AU$140–$171/mo | AU$348–$430/mo |

State Premium Variations

| State | Premium Index vs National Avg | Primary Driver |

|---|---|---|

| NSW | +8% | High hospital costs · Dense urban claims |

| VIC | +3% | High medical specialist fees |

| QLD | -2% | Lower hospital base costs |

| WA | +5% | Remote service delivery costs |

| SA | -4% | Lower cost base · Less congested hospitals |

| TAS | -6% | Lowest cost base nationally |

🔍 Full Provider Reviews — Top 5 Detailed 2026

1. HCF — Best Overall Value (Not-for-Profit)

HCF (Hospitals Contribution Fund of Australia) is Australia's largest not-for-profit private health insurer with 1.9 million members. As a not-for-profit mutual, HCF returns all surplus to members — there are no shareholders to pay dividends, and every dollar of premium revenue either pays for member claims or improves member services. HCF consistently receives the highest FAIRER Finance customer satisfaction ratings in the Australian private health insurance market — 5 stars across claims satisfaction, communication, and value for money.

HCF's More for Members programme provides additional benefits beyond standard policy coverage: free preventive health services at HCF dental and eye centres, a health management programme with personalised support for chronic condition management, and the More for You extras programme that provides benefits at preferred provider networks above standard extras limits. HCF's dental network — with owned and affiliated HCF Dental centres nationally — provides higher benefits for in-network dental treatment and no-gap dental checkups for adults on most extras policies. For most Australian families not working in specific industries served by restricted-access funds like Teachers Health or CBHS, HCF is the starting recommendation.

2. Medibank — Best Network Breadth

Medibank is Australia's largest private health insurer by market share — 3.7 million members across all states and territories. As an ASX-listed for-profit insurer (since its 2014 privatisation), Medibank returns profits to shareholders — a structural difference from not-for-profit funds that results in somewhat higher net premiums for equivalent cover. Medibank's primary strength is its hospital and healthcare provider network — the largest of any Australian insurer, covering 99%+ of private hospitals nationally and including the strongest preferred provider agreements with specialists in major metropolitan areas.

Medibank's 24/7 health advice line — staffed by registered nurses — is one of the most comprehensive member support services offered by any Australian health insurer, providing after-hours health guidance that reduces unnecessary emergency department presentations. Their Live Better programme rewards members with points for healthy activities (steps, mindfulness, health checks) redeemable for partner discounts and rewards. For members who prioritise network certainty and are comfortable with for-profit insurer structure, Medibank's breadth is its primary advantage.

3. nib — Best for Digital Experience and International Workers

nib is the most digitally sophisticated Australian health insurer — their app-first approach, immediate online claims processing, and digital health support tools (telehealth, mental health app partnerships, online pharmacy) are the most advanced in the market. For younger Australians who prefer digital self-service and are comfortable managing their health cover entirely through an app, nib's experience is significantly better than the legacy systems of Medibank and Bupa.

nib's international health insurance (OSHC — Overseas Student Health Cover, and OVHC — Overseas Visitors Health Cover) products make them particularly relevant for international students and temporary visa holders in Australia — nib is one of the leading OSHC providers and covers international healthcare needs with the most user-friendly digital experience in this segment. For Australian residents not needing international-specific products, nib's standard domestic products are competitive in pricing and strong in digital experience.

4. Bupa — Best Dental Network

Bupa is Australia's largest health insurer by member count (4.2 million) and the only insurer with a globally integrated health experience through the international Bupa group. Bupa's dental network — with over 300 owned Bupa Dental practices and thousands of affiliated dentists — is the largest of any insurer and enables no-gap dental checkups and preferred dental benefits significantly above standard extras limits. For families with high dental usage (orthodontics, crowns, regular preventive care), Bupa's dental network advantage is genuine and measurable. Bupa's premium pricing runs slightly above Medibank — which runs above the not-for-profit funds — making Bupa best suited for members who specifically value the dental and broader health provider network.

5. Australian Unity — Best Wellness Programme

Australian Unity is a not-for-profit health and care organisation with 500,000 health insurance members. Their Wellbeing programme — which provides members with personalised health coaching, preventive health incentives, and integrated care coordination — is the most comprehensive wellness benefit included in any Australian health insurance product. For health-conscious members who actively engage with wellness programmes, Australian Unity's approach provides tangible benefits beyond the standard insurance claim model. Their premium pricing is competitive with other not-for-profit funds and well below Medibank and Bupa.

📊 Gold, Silver, Bronze, Basic — Australia's Hospital Tier System

Since April 2019, Australian hospital cover products have been categorised into four standard tiers: Gold, Silver, Bronze, and Basic. These tiers define which clinical categories each policy must cover, making comparison easier than before when policy names and descriptions were unstandardised.

| Tier | What's Covered | Who Needs It | Typical Annual Premium (Single) |

|---|---|---|---|

| Gold 🏆 | All 38 clinical categories including obstetrics, joint replacement, cardiac, psychiatric | Families planning children · Older Australians · Comprehensive protection | AU$1,650–$2,100 |

| Silver | Most categories except some elective services — typically excludes obstetrics | Established families done with children · Middle-aged adults | AU$1,260–$1,610 |

| Bronze | Core services — excludes obstetrics, joint replacement, cardiac surgery | Young healthy adults wanting hospital access and MLS avoidance | AU$940–$1,200 |

| Basic | Minimum hospital cover — primarily for MLS avoidance, very limited clinical coverage | High-income earners avoiding MLS surcharge at lowest cost | AU$660–$850 |

The tier system creates clear guidance for age-appropriate cover selection. Young Australians under 30 who primarily want MLS avoidance and the ability to access a private hospital room if needed — Bronze or Basic cover is appropriate and costs AU$55–$80/month. Young families planning children need Gold cover for obstetrics — the difference between Gold and Bronze can exceed AU$60,000 in obstetric hospital costs per birth for private patients without Gold hospital cover. Older Australians approaching joint replacement or cardiac risk should ensure Gold or Silver+ cover that includes these procedures.

💵 Medicare Levy Surcharge — Do You Need Cover to Avoid It?

| Income (Single) | MLS Rate | Annual MLS Cost | Basic Hospital Cover Cost | Verdict |

|---|---|---|---|---|

| Under $93,000 | 0% | $0 | AU$660–$850 | MLS not applicable — buy cover for health reasons or don't |

| $93,001–$108,000 | 1.0% | $930–$1,080 | AU$660–$850 | ✅ Buy cover — cheaper than MLS |

| $108,001–$144,000 | 1.25% | $1,350–$1,800 | AU$660–$850 | ✅ Buy cover — significantly cheaper than MLS |

| Over $144,001 | 1.5% | $2,160+ | AU$660–$850 | ✅ Buy cover — always cheaper at these incomes |

For singles earning above AU$93,000 without hospital cover, the mathematics are unambiguous: the cheapest Basic hospital cover (AU$660–$850/year) costs less than the Medicare Levy Surcharge at every income level above $93,000 — while also providing the actual insurance protection. The MLS surcharge exists specifically to create this financial incentive. If you are above the threshold without hospital cover, contact a fund and take out at minimum Basic hospital cover immediately — the tax saving and coverage benefit combined make it a straightforward financial decision.

💡 How to Save on Health Insurance Australia 2026 — 8 Proven Strategies

1. Join a restricted-access fund if you qualify

Australia's restricted-access funds — Teachers Health (education sector), CBHS (Commonwealth Bank employees), Defence Health (ADF), Police Health (police), and several others — consistently offer the best value in Australian private health insurance. They are not-for-profit, have highly loyal member bases with lower churn, and have historically had lower claims ratios than open funds — resulting in lower premiums and better benefits. If your employer or profession qualifies you for a restricted fund, check their rates before looking at open funds.

2. Compare using iSelect, comparethemarket, or Finder — but also check direct

Comparison platforms are a useful starting point but do not include all funds. Private health insurance comparison using iSelect or comparethemarket is a good first step. Then check directly with HCF, nib, and Australian Unity — which are not always featured prominently on comparison platforms. For a detailed review of Australian insurance comparison platforms including their limitations, see our guide on iSelect Australia Review 2026.

3. Choose the right tier for your life stage

Over-insuring is as expensive as under-insuring. A healthy 27-year-old single adult does not need Gold hospital cover — Bronze or Silver is appropriate and costs AU$600–$700 less per year. A family planning to have children in the next 2 years needs Gold — or faces AU$20,000–$60,000 in obstetric costs per birth. Review your tier against your current and expected near-term health needs annually.

4. Increase your excess to reduce your premium

Choosing a higher hospital excess (AU$500 or AU$750 versus the minimum AU$0) reduces your annual hospital premium by AU$200–$500. For a young healthy adult who is unlikely to use hospital cover frequently, an AU$750 excess reduces both the premium and the financial risk in a realistic scenario — most hospital admissions for young adults are day procedures where the excess may not apply at all.

5. Pay annually, not monthly

Paying your annual premium upfront typically saves 4–6% versus monthly instalments — because the fund avoids administration costs of 12 monthly transactions and passes part of the saving to you. On a AU$2,200 annual premium, the saving is AU$88–$132 — worth having for a single online bank transfer.

6. Take out cover before age 31 to avoid LHC loading

The Lifetime Health Cover loading adds 2% per year after age 31 — permanently — until you have held cover for 10 continuous years. Taking out any level of hospital cover before your 31st birthday eliminates this loading risk entirely. Even Basic hospital cover at AU$55–$70/month avoids a 2% annual accumulating surcharge on your future premiums. The LHC maths favour early uptake decisively.

7. Review and switch at every annual premium increase

Australian private health insurance premiums increase once per year in April — by the government-approved percentage (3.73% in 2026). Each April increase is a natural review trigger. Use APRA's health insurance comparison data or a comparison platform to check whether your current fund's increase exceeded the industry average and whether equivalent cover is available cheaper elsewhere. Switching funds transfers your waiting period credits — you do not re-serve waiting periods for equivalent levels of cover.

8. Claim every extras benefit you're entitled to

The average Australian with extras cover claims only 62% of their annual extras entitlement — leaving 38% of their paid-for benefits unused. Track your annual limits for each benefit category (dental, optical, physio), schedule any necessary appointments before your policy year resets, and use your fund's app or member portal to check your remaining benefit balances quarterly. Unused dental benefits for a family can represent AU$200–$400 in foregone value every year.

❓ Frequently Asked Questions — Health Insurance Australia 2026

What is the best health insurance in Australia in 2026?

HCF is the best overall health insurance provider in Australia for 2026 for most members — it is Australia's largest not-for-profit fund, receives the highest FAIRER Finance customer satisfaction ratings (5 stars), offers competitive premiums, provides no-gap dental checkups at HCF Dental centres, and returns all surplus to members rather than to shareholders. For specific profiles: nib is best for digital-first users and international workers; Medibank is best for those who need the broadest national provider network; Bupa is best for families with heavy dental use; Teachers Health is cheapest if you qualify. The best insurer for you depends on your age, state, health needs, and whether you qualify for any restricted-access fund.

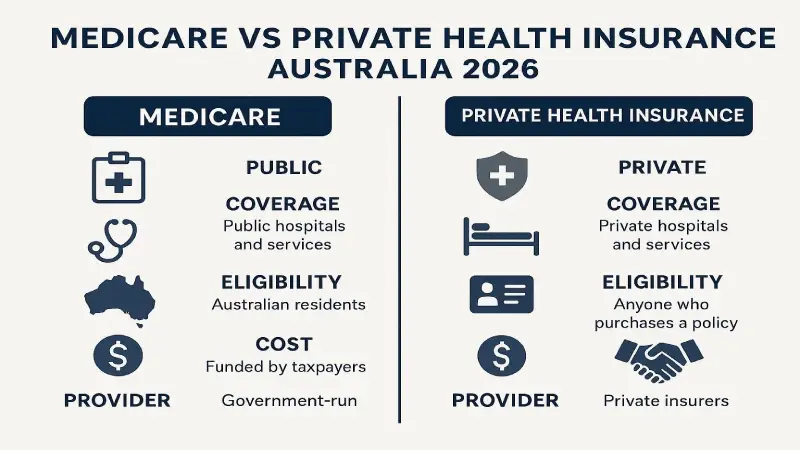

Do I need private health insurance in Australia?

Private health insurance is not legally mandatory in Australia — Medicare provides universal public healthcare. However, there are strong financial incentives to hold at minimum hospital cover: the Medicare Levy Surcharge (1.0–1.5% of income) applies to individuals earning above AU$93,000 without hospital cover; the Lifetime Health Cover loading (2% per year after age 31) applies to first-time purchasers who delay; and public hospital elective surgery waiting lists average 42 days nationally. For higher-income earners (above AU$93,000), hospital-only cover almost always costs less than the Medicare Levy Surcharge while providing actual insurance protection. For everyone, taking out at least Basic hospital cover before age 31 avoids the LHC loading permanently.

How much does private health insurance cost in Australia per month?

Private health insurance in Australia costs approximately AU$55–$85/month for Basic hospital cover, AU$78–$130/month for Bronze hospital cover, AU$105–$165/month for Silver hospital cover, and AU$138–$256/month for Gold hospital cover, for a single adult in NSW in 2026. Adding extras (dental, optical, physiotherapy) typically adds AU$50–$120/month depending on extras level. A family with Gold hospital and comprehensive extras typically pays AU$320–$480/month (AU$3,840–$5,760/year). Premiums vary by state — NSW and WA are the most expensive; Tasmania and South Australia are the cheapest. Premiums increased 3.73% from April 2025 under the government's annual approval process.

Can I switch health insurance funds without serving waiting periods again?

Yes — when you switch Australian health insurance funds for equivalent or lower levels of cover, your waiting period credits transfer to the new fund. You do not re-serve waiting periods you have already completed. If you are switching to a higher tier (e.g., from Bronze to Gold hospital), waiting periods apply only to the new clinical categories added — not to those you were already covered for. This means switching is financially risk-free from a waiting period perspective for equivalent cover — you keep all your entitlements while potentially accessing a cheaper premium or better benefits. Switch any time you find better value; you are not locked in to your current fund by waiting period concerns for equivalent cover.

What is the Medicare Levy Surcharge and how do I avoid it?

The Medicare Levy Surcharge (MLS) is an additional tax of 1.0–1.5% of taxable income charged to higher-income Australians who do not hold an appropriate private hospital insurance policy. In 2026, the MLS applies to singles earning above AU$93,000 per year and families above AU$186,000 combined. The surcharge is tiered: 1.0% for income $93,001–$108,000; 1.25% for $108,001–$144,000; and 1.5% for income above $144,001. To avoid the MLS, you must hold an eligible private hospital cover policy — at minimum a Basic hospital policy from a registered Australian health fund. Even the cheapest Basic hospital policy (approximately AU$55–$70/month) costs significantly less than the MLS for any income above AU$93,000, making it financially rational to take out cover at the surcharge threshold.

What is the Lifetime Health Cover loading and how does it work?

The Lifetime Health Cover (LHC) loading is a permanent premium surcharge applied to Australians who first take out private hospital cover after age 31. The loading is 2% per year of delay beyond age 30 — so someone who first buys hospital cover at age 40 pays a 20% permanent loading, while someone who waits until 50 pays a 40% loading (maximum 70%). The loading applies until the person has held private hospital cover continuously for 10 years, after which it is removed. The LHC incentivises Australians to take out hospital cover earlier in life. The practical advice: take out at least Basic hospital cover before your 31st birthday — even if you do not expect to use it frequently, the LHC loading avoided over a lifetime is worth far more than the minimal premium for Basic cover.

✅ Final Verdict — Best Health Insurance Australia 2026

HCF wins overall — best not-for-profit value, highest satisfaction, competitive premiums. nib wins for digital experience and international workers. Medibank wins for network breadth across all states. Bupa wins for dental — best for families with heavy dental use. Teachers Health, CBHS, and Defence Health win if you qualify — restricted funds offer the best value of all. For most Australians, comparing at least 3 quotes including the not-for-profit funds before renewing will identify savings of AU$400–$1,600 annually without reducing coverage quality.

For Australia's broader insurance landscape including car insurance, see our guides at Best Car Insurance Australia 2026 and iSelect Car Insurance Review Australia 2026.

Disclaimer: This article provides general information about Australian private health insurance. All premium ranges are approximate — individual quotes vary by state, age, and cover level. Always verify current premiums directly with funds using the government's Private Health Insurance Comparison website at privatehealth.gov.au. Nexuora is not affiliated with any health fund listed. Updated April 23, 2026.

Ahmada Ndao is a financial research analyst and independent journalist

specializing in US consumer finance, legal rights, and insurance markets.

With over 5 years covering American financial products, he has helped

thousands of readers navigate complex insurance decisions, find the right

legal representation, and optimize their credit strategies. His research

methodology combines primary data analysis, direct outreach to industry

professionals, and continuous monitoring of federal regulatory changes.

Ahmada’s work has been cited by financial communities across the US and

reviewed by licensed attorneys and insurance professionals for accuracy.