A cancer diagnosis costs the average American $42,000 in out-of-pocket expenses even with health insurance. A heart attack adds $24,000 in costs not covered by standard health plans. Critical illness insurance addresses exactly this gap — paying you a lump sum of $10,000 to $100,000 cash directly when you’re diagnosed with a covered condition, with no restrictions on how you spend it. You can use it to cover deductibles, pay your mortgage while you can’t work, hire help at home, or travel to a specialist. This 2026 guide ranks the 7 best critical illness insurance providers in the US by coverage breadth, price, payout speed, and claims reliability — and explains exactly what these policies cover, what they exclude, and who actually needs one.

Table of Contents

- Quick Snapshot — Critical Illness Insurance 2026

- How Critical Illness Insurance Works

- Critical Illness vs Disability vs Life Insurance

- Top 7 Providers — Full Rankings

- Real Monthly Costs by Age and Coverage Amount

- What’s Covered — and What’s Not

- Who Actually Needs Critical Illness Insurance?

- Employer Plan vs Individual Policy

- Frequently Asked Questions

Quick Snapshot — Critical Illness Insurance USA 2026

| Category | Details |

|---|---|

| What it pays | Lump-sum cash benefit upon diagnosis of covered condition |

| Typical benefit amounts | $5,000 – $500,000 (individual policies) |

| Most common covered conditions | Cancer, heart attack, stroke, organ failure, coma |

| Broadest coverage (employer plans) | Up to 130+ conditions (Mutual of Omaha) |

| Average monthly cost (age 35, $25K benefit) | $25–$50/month |

| Average monthly cost (age 50, $50K benefit) | $80–$150/month |

| Waiting period after purchase | 30–90 days (varies by insurer) |

| Survival period requirement | 14–30 days after diagnosis (most policies) |

| Best for | High-deductible health plan holders, self-employed, high-risk family history |

| #1 Provider Overall | Aflac (broadest individual availability) |

How Critical Illness Insurance Works

The mechanics are simpler than most insurance products. You pay a monthly premium. If you are diagnosed with a covered condition — cancer, heart attack, stroke, organ failure, or one of the other listed conditions — the insurer pays you a lump sum of cash. That’s it. The money comes to you directly, not to your doctors or hospital. You can spend it on anything.

The Diagnosis Trigger

Payment is triggered by a confirmed medical diagnosis of a covered condition by a licensed physician. Most policies also require a « survival period » — typically 14–30 days following the diagnosis — before the benefit is paid. This prevents claims from diagnoses made very close to the end of life where the insured passes away shortly after diagnosis.

Lump Sum vs Scheduled Benefits

Most critical illness policies pay the full lump sum on first diagnosis. Some policies pay a percentage for less severe diagnoses: for example, 25% of the benefit for early-stage cancer and 100% for invasive cancer. Aflac’s policies can pay additional benefits if you’re diagnosed with a different covered illness 180 days after your initial claim — meaning a cancer survivor who later has a heart attack can claim twice.

What Happens After You Claim

Most policies continue in force after a claim but reduce the available benefit by the amount paid. Some policies restore the full benefit after a waiting period (typically 12 months claim-free). Renewal terms vary — some policies are guaranteed renewable (the insurer cannot cancel as long as you pay premiums), while others have age limits for renewal.

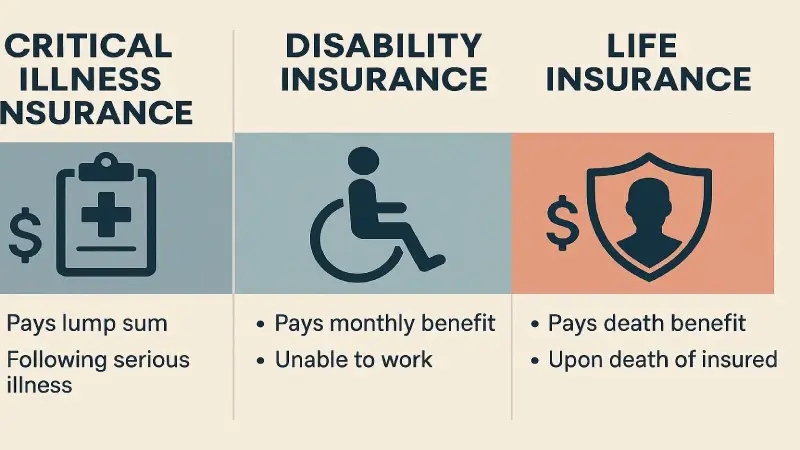

Critical Illness vs Disability vs Life Insurance — Key Differences

| Factor | Critical Illness | Disability Insurance | Life Insurance |

|---|---|---|---|

| When it pays | At diagnosis of covered condition | When you can’t work due to illness/injury | At death |

| Payment type | Lump sum — one payment | Monthly income replacement | Lump sum to beneficiary |

| Who receives payment | You (the insured) | You (the insured) | Your beneficiaries |

| Restriction on use | None — spend on anything | Replaces income only | None (beneficiary decides) |

| Covers inability to work? | Not specifically | Yes — primary purpose | No |

| Typical benefit | $10K–$100K lump sum | 60–70% of monthly income | $250K–$1M+ lump sum |

| Monthly cost (age 40) | $40–$80 | $100–$300 | $25–$100 (term) |

| Best use case | Cover deductibles, non-medical costs, immediate expenses | Replace lost income during long recovery | Protect dependents from loss of income at death |

Top 7 Critical Illness Insurance Providers USA 2026

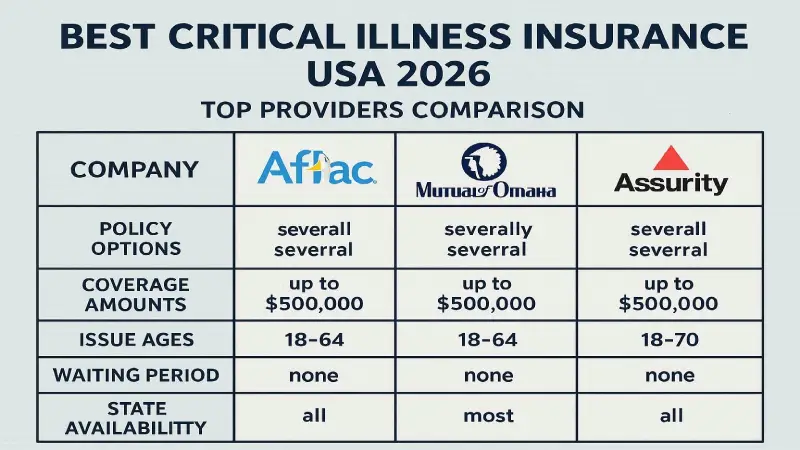

#1 — Aflac: Best Individual Critical Illness Insurance

Aflac is the most widely recognized critical illness insurer in America and the top choice for individual policies. Their key advantages: guaranteed issue up to $20,000 (no medical underwriting required for lower benefit amounts), coverage for 25+ conditions, and a subsequent illness benefit that pays again if you’re diagnosed with a different covered illness 180 days after your initial claim. Aflac also offers a return of premium rider — if you hold the policy for 20+ years without making a claim, you receive all premiums paid back. Coverage amounts run $5,000 to $75,000. Their wellness benefit pays you for completing annual health screenings — a unique feature that rewards preventive care. The limitation: not available in New York, New Jersey, Virginia, and Idaho for individual policies.

#2 — Mutual of Omaha: Best for Comprehensive Coverage

Mutual of Omaha covers 25+ conditions on individual policies and 130+ conditions through employer group plans — the broadest coverage in the market. Their $10,000 coverage amount is specifically designed for high-deductible health insurance holders — enough to cover most HDHP deductibles plus additional expenses. Their standout feature is the return of premium benefit: if you pass away without making a claim, your beneficiaries receive all premiums paid back — making the policy a zero-cost insurance product for families. They also offer separate cancer-only, heart attack-only, and stroke-only policies at lower premiums for targeted risk coverage. Available nationwide for individuals aged 18–89.

#3 — Assurity: Best for Multi-Condition Payouts

Assurity earns high marks from independent analysts for paying benefits on a per-condition basis rather than a single lifetime benefit — meaning multiple separate conditions can each trigger separate payments. Their wellness benefit pays $50–$150 annually for completing health screenings. Coverage amounts of $10,000 to $75,000 are available with relatively competitive underwriting. Assurity has a lower public profile than Aflac or Mutual of Omaha but consistently ranks among the top individual CI providers on plan design quality.

#4 — Corebridge Financial (formerly AIG): Best for High Benefit Amounts

Corebridge Financial (AIG’s life and retirement division) offers critical illness coverage up to $500,000 — the highest maximum available from any major US insurer. Their plans cover 30+ conditions including less common ones (ALS, cystic fibrosis, severe burns, major head trauma). The high benefit ceiling makes Corebridge the top choice for high-income earners who want significant financial protection against a career-disrupting diagnosis. A rated by AM Best.

#5 — UnitedHealthcare: Best Employer-Based Critical Illness

For employer-sponsored critical illness coverage, UnitedHealthcare covers 14 critical illness types at $66.66/month for $40,000 in benefits for a 45-year-old (one of the most competitive employer-rate benchmarks available). The limitation: maximum benefit drops by 50% after the policyholder reaches 65, and policies are renewable only until age 70. For working-age employees whose company offers UHC group benefits, this is typically the most cost-effective entry point into critical illness coverage.

#6 — MetLife: Best for Employer Group Plans with Large Teams

MetLife’s critical illness product shines in the employer group context — their underwriting is flexible for large groups, they cover a broad range of conditions, and their employer plan administration is rated highly by HR departments. For individual employees, the key benefit of MetLife CI insurance is portability — you can often take the policy with you if you leave the employer. Available through employers across the US.

#7 — Transamerica: Best for Senior Critical Illness Coverage

Transamerica specifically structures its critical illness products for older purchasers, with competitive underwriting for applicants up to age 64 and guaranteed renewable coverage. For Americans in their 50s or early 60s who want a financial cushion against cancer or heart disease before Medicare eligibility, Transamerica offers one of the most accessible individual CI products. Their cancer-specific rider allows targeted coverage at lower premiums if cancer is the primary concern.

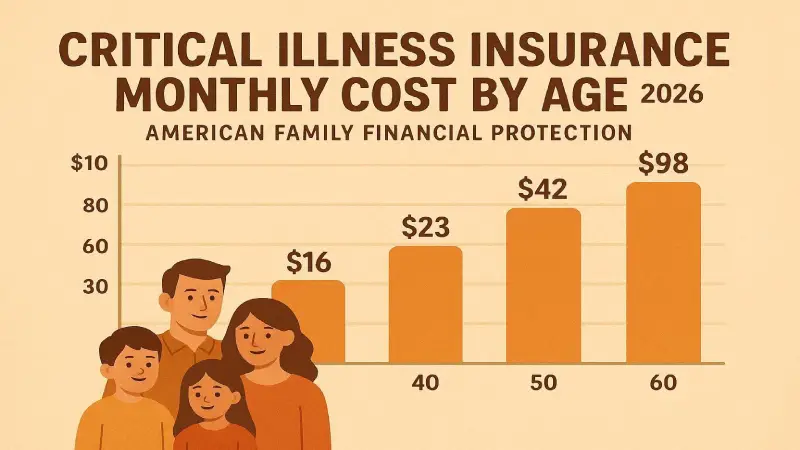

Real Monthly Costs by Age and Coverage Amount — 2026

| Age | $10,000 Benefit | $25,000 Benefit | $50,000 Benefit | $100,000 Benefit |

|---|---|---|---|---|

| Age 30 | ~$15/mo | ~$25/mo | ~$40/mo | ~$70/mo |

| Age 35 | ~$18/mo | ~$32/mo | ~$55/mo | ~$95/mo |

| Age 40 | ~$22/mo | ~$42/mo | ~$75/mo | ~$130/mo |

| Age 45 | ~$30/mo | ~$58/mo | ~$105/mo | ~$185/mo |

| Age 50 | ~$42/mo | ~$80/mo | ~$145/mo | ~$265/mo |

| Age 55 | ~$60/mo | ~$115/mo | ~$210/mo | ~$390/mo |

| Age 60 | ~$85/mo | ~$160/mo | ~$300/mo | ~$560/mo |

*Estimates based on male non-smoker standard health rating. Female rates are typically 10–20% lower. Smoker rates are 30–60% higher. Rates vary by insurer and state.

The Break-Even Question

The common objection to critical illness insurance is « what if I never use it? » At $50/month for a $25,000 benefit at age 35, you break even if you make a claim within 41 years (paying $25,000 total in premiums by age 76). Given that 1 in 3 Americans will develop cancer in their lifetime, and 1 in 4 will have a heart disease event before age 65, the statistical likelihood of needing the benefit is meaningfully above 25–30% for most profiles. The return of premium rider (available from Aflac and Mutual of Omaha) eliminates the break-even concern entirely — if you never claim, you get all premiums returned.

What Critical Illness Insurance Covers — and What It Doesn't

Standard Covered Conditions (Most Policies)

| Condition | Typical Payout | Notes |

|---|---|---|

| Invasive Cancer | 100% of benefit | Most policies; early-stage may pay 25% |

| Heart Attack | 100% of benefit | Requires confirmed cardiac enzyme evidence |

| Stroke | 100% of benefit | Must result in permanent neurological deficit |

| Major Organ Transplant | 100% of benefit | Heart, liver, kidney, lung, pancreas, bone marrow |

| Kidney (Renal) Failure | 100% of benefit | End-stage requiring dialysis or transplant |

| Coronary Artery Bypass | 25% of benefit | Surgical treatment only; angioplasty usually excluded |

| Coma | 100% of benefit | Typically requires 96+ hours of unconsciousness |

| Blindness / Deafness | 100% of benefit | Permanent, total loss required |

| Paralysis | 100% of benefit | Permanent loss of use of 2+ limbs |

| ALS / MS | 100% of benefit | Not all policies include these — check specifically |

Common Exclusions — What’s NOT Covered

Pre-existing conditions: Any condition you were diagnosed with or treated for before the policy start date is typically excluded for a period (usually 12–24 months) or permanently. Early-stage or non-invasive cancer: Skin cancer (unless melanoma), carcinoma-in-situ, and other early-stage cancers typically pay only 25% of the benefit or are excluded entirely. Self-inflicted injury and conditions resulting from drug or alcohol abuse are standard exclusions. Acts of war and criminal activity. Conditions diagnosed within the waiting period (typically the first 30–90 days after policy purchase). Cosmetic surgery complications.

Who Actually Needs Critical Illness Insurance?

Critical illness insurance is valuable for specific profiles — and unnecessary or redundant for others. Here is an honest assessment.

You Should Strongly Consider CI Insurance If:

You have a high-deductible health plan (HDHP) — the lump-sum benefit can cover your entire annual deductible ($1,600–$7,000 for individual plans in 2026) plus ancillary costs. You are self-employed without employer disability coverage — CI insurance provides immediate cash for non-medical expenses while you recover. You have a family history of cancer, heart disease, or stroke — higher personal risk makes the expected value calculation more favorable. You are the primary breadwinner and a serious illness would disrupt your household’s income even with health insurance covering medical costs. You have limited emergency savings — less than 6 months of expenses — and a serious illness could create financial crisis.

CI Insurance May Be Less Necessary If:

You have robust disability insurance covering 70%+ of your income — disability insurance already handles most of what CI insurance addresses. You have substantial emergency savings ($50,000+) that could absorb a serious illness without financial crisis. You have a very low deductible health plan where out-of-pocket maximum is below $2,000. You already have life insurance with a living benefits rider that pays on terminal illness diagnosis — this partially overlaps with CI coverage.

Employer Plan vs Individual Policy — Which Is Better?

| Factor | Employer Group Plan | Individual Policy |

|---|---|---|

| Cost | Lower (group rates) | Higher (individual underwriting) |

| Medical underwriting | Often guaranteed issue | Medical questions required (above $20K usually) |

| Portability | Sometimes portable (ask) | Always portable — yours regardless of employer |

| Coverage amount | Often capped at $20K–$50K | Up to $500K available |

| Conditions covered | Up to 130+ (group plans) | Typically 14–30 (individual plans) |

| Premium stability | Can change at renewal | Fixed or level premiums available |

| Recommendation | Take if offered at work | Supplement with individual policy if coverage is insufficient |

The optimal strategy for most Americans: If your employer offers group critical illness coverage, enroll in it — the guaranteed issue and group rates make it almost always worth taking regardless of your health. Then evaluate whether the benefit amount is sufficient. If your employer offers $20,000 and you want $50,000 in total coverage, supplement with an individual Aflac or Mutual of Omaha policy for the additional $30,000.

Frequently Asked Questions — Critical Illness Insurance 2026

What is critical illness insurance and how does it work?

Critical illness insurance pays you a lump sum of cash — typically $10,000 to $100,000 — when you are diagnosed with a covered serious illness such as cancer, heart attack, or stroke. The payment comes directly to you, with no restrictions on how you use it. You can pay medical deductibles, replace lost income, cover household expenses, or use it for anything else. It is supplemental to health insurance — not a replacement for it. You pay monthly premiums, and if you’re diagnosed with a covered condition (and survive the required waiting period, typically 14–30 days), the insurer pays the lump sum.

Is Aflac critical illness insurance worth it?

Aflac critical illness insurance is worth it for most people who don’t have strong employer disability coverage and carry a high-deductible health plan. Their guaranteed issue up to $20,000 (no medical questions) makes it accessible regardless of health history, the subsequent illness benefit allows multiple claims for different conditions, and the return of premium rider ensures you get your money back if you never claim. The main limitations are the $75,000 maximum benefit and unavailability in New York, New Jersey, Virginia, and Idaho.

How much does critical illness insurance cost per month?

Critical illness insurance typically costs $15–$45/month for a $25,000 benefit at ages 30–45 for a non-smoking male in standard health. At age 50, the same coverage costs $58–$80/month. At age 55, $80–$115/month. Women typically pay 10–20% less. Smokers pay 30–60% more. Coverage through an employer group plan is significantly cheaper because of group underwriting — often $15–$30/month for $20,000 in coverage regardless of age.

What is the difference between critical illness insurance and disability insurance?

Critical illness insurance pays a one-time lump sum when you’re diagnosed with a specific covered condition — regardless of whether you can work. Disability insurance pays monthly income replacement when you are unable to work due to any illness or injury. Critical illness coverage is triggered by a diagnosis; disability is triggered by inability to work. Many people benefit from both: disability insurance replaces your income during recovery, while critical illness insurance covers the immediate expenses (deductibles, household costs, non-medical bills) that appear at diagnosis before disability payments begin.

Does critical illness insurance cover all types of cancer?

No. Most critical illness policies cover invasive cancers but exclude or partially cover non-invasive conditions. Specifically: non-melanoma skin cancer (basal cell, squamous cell) is typically excluded entirely. Carcinoma-in-situ (pre-invasive cancer that hasn’t spread) usually pays 25% of the benefit, not 100%. Melanoma is typically covered at 100%. Early-stage prostate cancer detected by PSA without symptoms may be subject to waiting periods or partial benefits depending on the policy. Always check the specific cancer definition in any policy before purchasing.

Can I get critical illness insurance with a pre-existing condition?

It depends on the condition and the insurer. Guaranteed issue policies (like Aflac up to $20,000) approve anyone without medical questions — making them accessible regardless of health history. However, guaranteed issue policies typically exclude claims related to pre-existing conditions for the first 12–24 months after coverage begins. After this exclusion period, pre-existing conditions may be covered. Employer group plans also often offer guaranteed issue. Individually underwritten policies above $20,000 will ask health questions and may decline, exclude specific conditions, or charge higher premiums based on your health history.

Final Verdict — Best Critical Illness Insurance USA 2026

For most Americans, Aflac is the best starting point for individual critical illness coverage — guaranteed issue up to $20,000, broad availability (49 states), and the subsequent illness benefit make it the most accessible and comprehensive individual option. Mutual of Omaha is the best choice if you want comprehensive coverage with a return of premium option or if you need more than $20,000 without triggering medical underwriting through a group plan. Take your employer’s group CI plan if offered — the group rates and often-guaranteed issue make it almost always worth accepting regardless of health. Critical illness insurance works best as part of a complete financial protection strategy alongside health insurance and disability insurance — not as a replacement for either. For related coverage see our guide on Best Health Insurance USA 2026 and Best Medicare Advantage Plans 2026.

Disclaimer: This article is for informational purposes only and does not constitute financial or insurance advice. Premium estimates are illustrative and vary by insurer, state, age, health, and gender. Always obtain personalized quotes and review full policy documents before purchasing. Nexuora is not affiliated with any insurer listed. Updated May 26, 2026.

Ahmada Ndao is a financial research analyst and independent journalist

specializing in US consumer finance, legal rights, and insurance markets.

With over 5 years covering American financial products, he has helped

thousands of readers navigate complex insurance decisions, find the right

legal representation, and optimize their credit strategies. His research

methodology combines primary data analysis, direct outreach to industry

professionals, and continuous monitoring of federal regulatory changes.

Ahmada’s work has been cited by financial communities across the US and

reviewed by licensed attorneys and insurance professionals for accuracy.