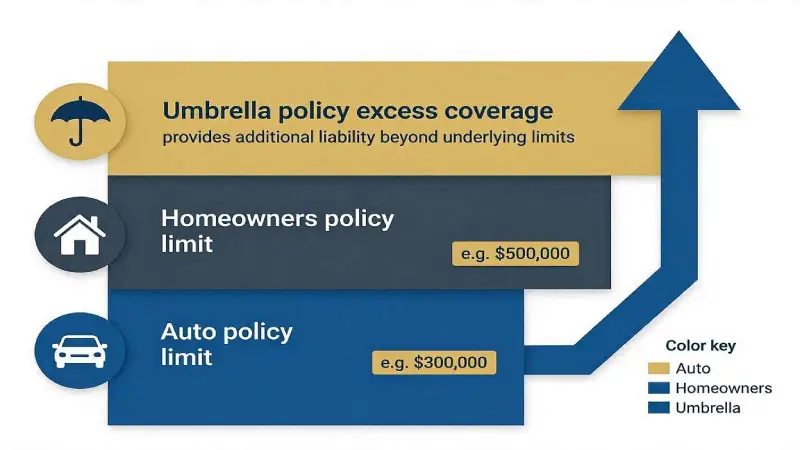

Umbrella insurance is a type of excess liability insurance that adds additional protection above your home, auto, boat, or rental property insurance limits.

For example:

If your auto insurance covers up to $300,000 but you are sued for $1.2 million after a severe accident, umbrella insurance can cover the remaining costs.

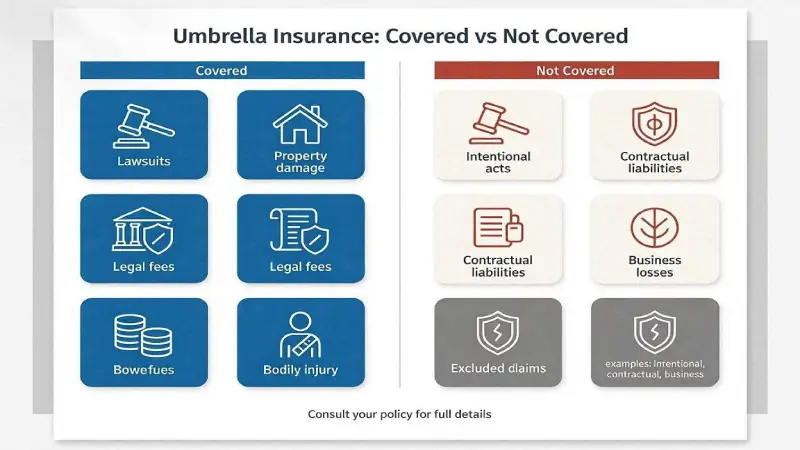

This protection may include:

- Legal defense costs

- Medical bills

- Property damage

- Personal injury lawsuits

- Defamation claims

- Dog bite liability

- Rental property lawsuits

Many wealthy Americans now consider umbrella insurance essential financial protection.

Related guides:

- /best-life-insurance-companies-usa-2026/

- /best-health-insurance-plans-usa-2026/

- /best-business-credit-cards-usa-2026/

- /best-credit-cards-usa-2026/

- /best-personal-loans-for-bad-credit-2026/

Several trends are increasing lawsuit risks in the United States:

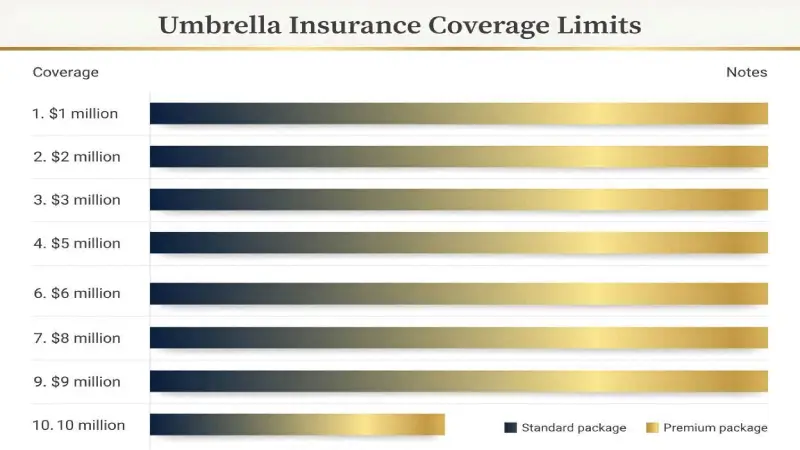

Financial experts often recommend:

- $1 million minimum for average households

- $2–5 million for high-income professionals

- $5M+ for landlords and wealthy families

You should consider:

- Net worth

- Home value

- Future earnings

- Number of vehicles

- Rental properties

- Teen drivers

Also compare:

- /best-landlord-insurance-usa-2026/

- /best-rental-property-insurance-2026/

Ahmada Ndao is a financial research analyst and independent journalist

specializing in US consumer finance, legal rights, and insurance markets.

With over 5 years covering American financial products, he has helped

thousands of readers navigate complex insurance decisions, find the right

legal representation, and optimize their credit strategies. His research

methodology combines primary data analysis, direct outreach to industry

professionals, and continuous monitoring of federal regulatory changes.

Ahmada’s work has been cited by financial communities across the US and

reviewed by licensed attorneys and insurance professionals for accuracy.