Best Homeowners Insurance USA 2026 — Top Providers After California Wildfires, Real Costs by State & The Coverage Gaps That Cost Homeowners Thousands

The 2025 Los Angeles wildfires caused $40 billion in insured losses — the most destructive wildfire event in California history — and triggered a crisis that is reshaping the American home insurance market in ways every homeowner in the country needs to understand. State Farm, Allstate, AIG, Chubb, Farmers, and at least a dozen other major carriers have either stopped writing new policies or dramatically reduced their California exposure. The state's insurer of last resort — the California FAIR Plan — reached 555,868 policies by March 2025, up 104,000 in just six months. But the crisis extends beyond California: Florida's hurricane-driven market collapse, rising premiums in tornado-prone Texas and Oklahoma, and nationwide construction cost increases of 4.2% are driving homeowners insurance premiums to record highs in every state. This guide ranks the best homeowners insurance providers for 2026 using real premium data from NAIC, NAIC complaint ratios, AM Best financial strength ratings, and J.D. Power customer satisfaction scores — giving you the complete framework to choose the right coverage before disaster strikes.

Key Facts — Best Homeowners Insurance USA 2026

- Amica is the #1 homeowners insurance company for 2026 for the third consecutive year — lowest average premium ($1,510/yr), lowest NAIC complaint ratio, strongest claims handling per Insure.com survey

- Travelers jumped to #2 in 2026 from #7 in 2025 — low complaint volume, excellent financial strength, and the cheapest California rates at $1,103/yr

- USAA is #1 for military families — highest J.D. Power satisfaction, cheapest premiums, but restricted to military members and veterans only

- State Farm dropped to #4 in 2026 — good customer service but NO new policies in California, Massachusetts, or Rhode Island

- California crisis: State Farm, Allstate, AIG, Chubb, Tokio Marine paused or stopped new CA home policies — use Travelers, AAA/CSAA, or California FAIR Plan as alternatives

- Average cost USA: $2,490/year for $300K dwelling coverage · Oklahoma $5,000+/yr · California $1,616/yr · Hawaii $400/yr

- The 80% Rule: Insure your home for at least 80% of rebuild cost — policies below this threshold trigger coinsurance penalties on every claim

- Wildfires not automatically covered in CA: Standard policies cover wildfire damage, but coverage is increasingly restricted in high-risk zones — verify before assuming you are covered

- Flood and earthquake are NEVER covered by standard homeowners insurance — require separate policies from private insurers or NFIP/CEA

- Check NAIC's Consumer Information Source to verify any insurer's complaint ratio before purchasing

The California Home Insurance Crisis — What Every American Homeowner Needs to Know

What began as a California problem is becoming a national warning. The sequence of events following the January 2025 LA wildfires has permanently altered how insurance companies price risk — not just in California, but in every high-risk state in America.

The timeline: State Farm — once California's largest home insurer — paused new policy sales in May 2023. Allstate followed. Then AIG, Chubb, Tokio Marine, AmGUARD, Falls Lake Insurance, and Trans Pacific all either stopped writing new home policies or dramatically reduced their California exposure. The January 2025 LA fires then caused $40 billion in insured losses, forcing the California FAIR Plan to request a $1 billion bailout from private insurers. New legislation in January 2026 created state-backed bond access and additional FAIR Plan funding — but the structural problem remains: California's Proposition 103 prevents insurers from pricing future wildfire risk accurately, making profitable underwriting nearly impossible in high-risk zones.

⚠️ If you live in a California wildfire-risk zone: Do not assume your current policy will renew. Check your renewal notice immediately. If you receive a non-renewal notice, you have 60 days to find alternative coverage. Options: (1) Travelers — still writing new CA policies at $1,103/yr average. (2) AAA/CSAA — regional coverage with competitive rates. (3) Mercury Insurance — announced CA expansion under new 2026 regulations. (4) California FAIR Plan — last resort, basic coverage only, significant gaps. Work with an independent broker who can access surplus lines carriers not available to consumers directly.

The ripple effects are national. Florida's home insurance market faces its own crisis driven by hurricane exposure and litigation abuse — with several state-backed Citizens Insurance policyholders receiving non-renewal notices as the state tries to reduce its exposure. Texas, Oklahoma, and Kansas homeowners face rising premiums driven by tornado and hail frequency. The lesson: every homeowner in America needs to verify their current coverage is adequate, review their insurer's financial strength, and understand exactly what their policy does and does not cover before the next disaster occurs.

Best Homeowners Insurance Companies USA 2026 — Ranked

Strengths

- #1 overall for 3rd consecutive year — Insure.com 2026

- Lowest average premium nationally ($1,510/yr)

- Lowest NAIC complaint ratio — fewer claims disputes than any major competitor

- Dividend program returns premiums in profitable years

- Strongest claims handling scores in annual survey

- A+ AM Best — exceptional financial stability

Limitations

- Not available in all states — check availability at amica.com

- No independent agent network — direct purchase only

- Limited coverage in California wildfire zones

Strengths

- Still writing new policies in California — $1,103/yr average

- A++ AM Best — highest possible financial strength rating

- Biggest ranking improvement in 2026 survey (#7 to #2)

- Low NAIC complaint ratio nationally

- Green home and identity theft add-ons available

- Available in all 50 states

Limitations

- California wildfire deductibles can be 2–5% of dwelling value ($8K–$20K on $400K home)

- Some add-ons require agent — limited online customization

Strengths

- #1 J.D. Power satisfaction — consistently the top-rated insurer

- A++ AM Best — same elite tier as Travelers

- Lowest average premiums among top national carriers

- Military-specific coverage (deployment, base housing, uniforms)

- Bundling discounts with USAA auto insurance

Limitations

- Eligibility restricted to military members, veterans, and immediate family

- Not available if you do not qualify — no exceptions

Strengths

- Second-lowest national average premium

- #1 digital experience — best website and app

- Highest trust and renewal scores in customer survey

- Extensive add-on options (business property, green home, yard/garden)

- Strong bundling discounts with auto insurance

Limitations

- Not writing new policies in California

- Agent required for purchase — no direct online bind

- Claim denial rates above average in disaster-prone areas (Weiss Ratings 2025)

Strengths

- A++ AM Best — highest financial strength

- Largest agent network in USA — 19,000+ agents

- Strong bundling discounts (home + auto = up to 20% off)

- Good add-on flexibility — water backup, identity theft, equipment

- Competitive $1,580/yr national average

Limitations

- Not writing new policies in California, Massachusetts, Rhode Island

- NAIC complaint ratio slightly above some competitors

- Agent-required for most transactions

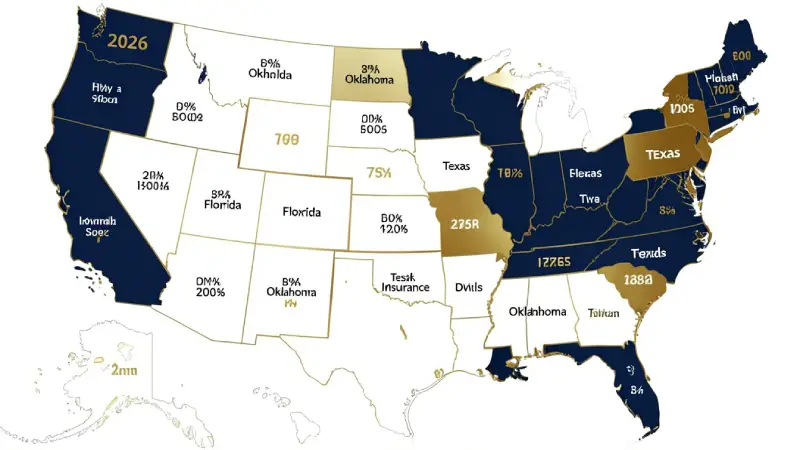

Homeowners Insurance Cost by State 2026 — Real Data

| State | Avg Annual Premium | vs National Avg | Primary Risk Driver | Market Condition |

|---|---|---|---|---|

| Oklahoma | $5,000+/yr | +100% | Tornadoes, hail | 🔴 Crisis — limited carriers |

| Kansas | $4,200/yr | +69% | Tornadoes, hail | 🔴 Very expensive |

| Florida | $3,800/yr | +52% | Hurricanes, litigation | 🔴 Crisis — many exits |

| Texas | $3,500/yr | +41% | Tornadoes, hail, hurricane | 🟡 Expensive, competitive |

| Louisiana | $3,400/yr | +37% | Hurricanes, flooding | 🔴 Very expensive |

| National Average | $2,490/yr | — | Varies | 🟡 Rising +8%/yr |

| California | $1,616/yr | -35% | Wildfires (not priced in) | 🔴 Crisis — limited new policies |

| New York | $1,800/yr | -28% | Winter storms, flooding | 🟢 Competitive |

| Illinois | $1,950/yr | -22% | Tornadoes, winter storms | 🟢 Competitive |

| Hawaii | $400/yr | -84% | Low (no hail/tornado) | 🟢 Cheap, stable |

What Homeowners Insurance Covers — And the 3 Critical Gaps That Surprise Claimants

| Coverage Type | What It Covers | Typical Limit | Key Notes |

|---|---|---|---|

| Dwelling (Coverage A) | Your home's physical structure — walls, roof, foundation, built-in appliances | Rebuild cost (typically $200K–$500K+) | Must equal at least 80% of rebuild cost to avoid coinsurance penalties |

| Other Structures (Coverage B) | Detached garage, fence, shed, pool | Typically 10% of Cov. A | Separate structures on your property not attached to main dwelling |

| Personal Property (Coverage C) | Furniture, clothing, electronics, appliances | Typically 50–70% of Cov. A | High-value items (jewelry, art) need scheduled endorsements |

| Liability (Coverage E) | Legal costs + damages if someone is injured on your property or you damage another's property | $100K–$500K standard | Increase to $300K+ — $100K is rarely enough in 2026 |

| Additional Living Expenses (Coverage D) | Hotel, meals, rental car while your home is uninhabitable after a covered loss | Typically 20–30% of Cov. A | Critical in California wildfire or hurricane evacuation scenarios |

The 3 Critical Coverage Gaps

Gap 1 — Flood damage is NEVER covered. Standard homeowners insurance explicitly excludes flood damage — even if a hurricane's storm surge floods your home. Flood insurance must be purchased separately through the National Flood Insurance Program (NFIP) or private flood insurers. Average NFIP policy: $700–$900/year. The gap between what people assume and what their policy actually covers has caused billions in out-of-pocket losses after every major flood event.

Gap 2 — Earthquake damage is NEVER covered. Standard policies explicitly exclude earthquakes and earth movement. California homeowners can purchase earthquake coverage through the California Earthquake Authority (CEA) or private insurers. The average California earthquake policy costs $800–$2,400/year depending on home location and construction.

Gap 3 — Sewer backup and water from outside is commonly excluded. Water damage from a burst pipe inside your home is typically covered. Water entering your home from outside — sewer backup, groundwater seepage, sump pump failure — is excluded by most standard policies. A sewer backup endorsement typically costs $50–$250/year and covers $5,000–$25,000 in damage. This is one of the most cost-effective add-ons available and one of the most commonly overlooked.

💡 The 80% Rule — the most expensive mistake homeowners make. If your home would cost $400,000 to rebuild and you insure it for $280,000 (70%), you have violated the 80% Rule. On a $100,000 partial loss claim, your insurer calculates: ($280K insured ÷ $320K required) × $100K loss = only $87,500 paid. You absorb $12,500 out-of-pocket — even though you thought you were insured. Insurers use their own replacement cost calculators at policy issuance — but rising construction costs of 4.2% per year mean your coverage needs adjustment annually. Ask your insurer about automatic inflation adjustment endorsements.

How to Choose the Right Homeowners Insurance — 10-Point Checklist

Homeowners Insurance Selection Checklist — 2026

- Calculate your home's rebuild cost (not market value) — use your insurer's replacement cost calculator or hire an independent appraiser. Insure for 100% of rebuild cost, not market value

- Verify the insurer's AM Best rating — only purchase from A-rated or better. A++ (USAA, Travelers, State Farm) = maximum financial strength

- Check NAIC complaint ratio at naic.org — below 1.0 is good, below 0.5 is excellent (Amica 0.370 = outstanding)

- Confirm coverage continues in your state — verify State Farm (not CA/MA/RI) and Allstate (not CA) availability before starting the application

- Add sewer backup endorsement — $50–$250/year covers $5K–$25K in water damage from outside sources

- Increase liability coverage to at least $300,000 — $100,000 is insufficient given current legal environment

- Schedule high-value items separately — jewelry, art, firearms, musical instruments need scheduled endorsements beyond standard personal property limits

- Verify flood exclusion and purchase NFIP or private flood insurance if you are in any flood zone — even Zone X (moderate risk) has meaningful flood probability

- Bundle with auto insurance — State Farm 20%, Allstate 10–25%, Nationwide 10–25% multi-policy discounts reduce total insurance cost significantly

- Get minimum 3 quotes before purchasing — rates for identical coverage can vary 30–50% between carriers in the same state

- Review your policy annually — construction cost increases of 4.2%/year mean your coverage limit needs adjustment even if your home is unchanged

FAQ — Best Homeowners Insurance USA 2026

Ahmada Ndao is a financial research analyst and independent journalist

specializing in US consumer finance, legal rights, and insurance markets.

With over 5 years covering American financial products, he has helped

thousands of readers navigate complex insurance decisions, find the right

legal representation, and optimize their credit strategies. His research

methodology combines primary data analysis, direct outreach to industry

professionals, and continuous monitoring of federal regulatory changes.

Ahmada’s work has been cited by financial communities across the US and

reviewed by licensed attorneys and insurance professionals for accuracy.