Wildfire Damage Restoration & Insurance Claims USA 2026 — What Every Homeowner Must Know

Wildfires caused $28.4 billion in insured losses in the United States in 2025 alone — the second-largest annual wildfire loss on record. California, Texas, Colorado, Florida, and Oregon account for the majority of wildfire damage claims, but the 2025 season saw destructive fires in states as far east as Tennessee and New Jersey, expanding the wildfire risk map significantly. For homeowners whose properties are damaged or destroyed by wildfire, the insurance claim and restoration process is one of the most complex and financially consequential experiences they will face — typically involving 12–36 months of displacement, an average of $380,000 in restoration costs for a total loss, and significant risk of claim disputes with their insurer. This complete 2026 guide explains everything homeowners need to know about wildfire damage claims: what is covered, what is excluded, how to file correctly, why claims get denied, and how to maximise your payout.

🛡️ What Wildfire Damage Home Insurance Covers — and What It Doesn't

Standard homeowners insurance (HO-3 policies) covers wildfire damage as a named or open-peril loss in virtually all US states. Wildfire is explicitly listed as a covered peril in nearly all standard homeowners policies — it is not excluded in the way that flood or earthquake is. However, coverage depth and exclusions vary significantly.

Covered: Dwelling Coverage (Coverage A)

The most critical coverage in a wildfire scenario — it pays for the cost to rebuild or repair your home's structure after wildfire damage. Coverage A should reflect the full replacement cost of your home — not its market value. These numbers diverge significantly in areas where land values are high (most of California) — your home's market value might be $800,000, but your rebuilding cost (structure only, not land) might be $450,000. Policies with Coverage A below the actual replacement cost result in under-insurance — you receive less than the full cost to rebuild. Given that construction costs increased 35–55% between 2022 and 2026, many policies written before 2022 are now significantly underinsured.

Covered: Other Structures (Coverage B)

Typically 10% of Coverage A — covers detached garages, fences, sheds, pools, and other structures on your property not attached to the main dwelling. For homeowners with significant other structures (large garages, guest houses, barns), this 10% limit may be inadequate. Request higher Coverage B limits if your other structures exceed 10% of your dwelling rebuild cost.

Covered: Personal Property (Coverage C)

Covers the replacement cost of your belongings — furniture, clothing, appliances, electronics, and other personal property — lost or damaged in the wildfire. Standard Coverage C is 50–70% of Coverage A. Critical limitation: high-value items (jewellery, art, firearms, musical instruments, collectibles, wine collections) are sub-limited — typically $1,000–$2,500 per category. Schedule valuable items separately on a personal articles floater to ensure full coverage. For wildfire total losses, the personal property claim requires an itemised inventory — which is why maintaining a documented home inventory (photos and video of every room and valuable item) is critically important before fire season.

Covered: Additional Living Expenses (Coverage D/E)

Pays for temporary housing, meals above your normal food cost, and other incremental living expenses while your home is uninhabitable during restoration. Standard limits are 20–30% of Coverage A or 12 months of actual expenses — whichever is less. Given that wildfire total-loss rebuilds currently average 18–36 months in California due to permit backlogs and contractor scarcity, 12-month ALE limits are frequently exhausted before rebuilding is complete. Seek policies with unlimited ALE or extended time limits in wildfire-prone areas.

NOT Covered: Vehicles

Vehicles damaged or destroyed by wildfire are not covered by your homeowners policy — they are covered under your comprehensive auto insurance. If you evacuated and your vehicle was damaged by fire, smoke, or falling debris, file a comprehensive auto claim — not a homeowners claim.

NOT Covered: Landscaping (Often Limited)

Trees, shrubs, plants, and landscaping are typically covered only to 5% of Coverage A, with a per-item limit of $500–$1,500. For homeowners with mature landscaping, orchards, or professionally designed gardens representing significant value, this limit is grossly inadequate. Separate landscaping coverage riders are available from some insurers.

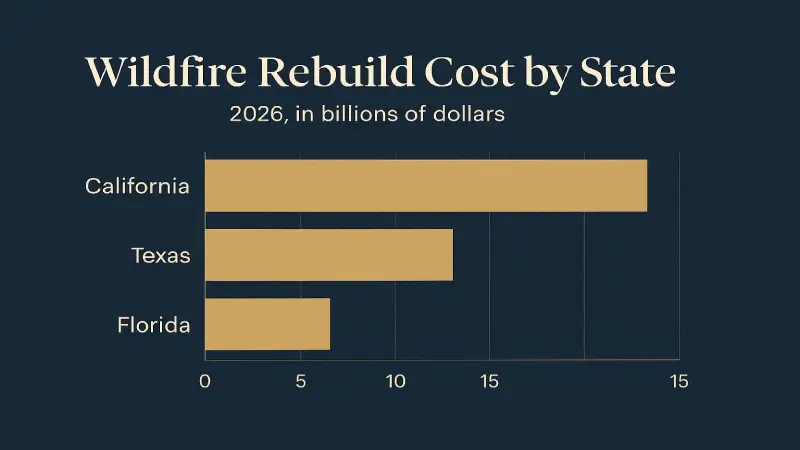

💰 Real Wildfire Restoration Costs — State by State 2026

| State | Avg Rebuild Cost/sq ft | 2,000 sq ft Home Total | vs 2022 Cost | High-Risk Areas |

|---|---|---|---|---|

| California (Coastal) | $380–$420 | $760K–$840K 🔴 | +52% | LA, San Diego, Bay Area WUI |

| California (Inland) | $280–$340 | $560K–$680K 🔴 | +47% | Sacramento, Shasta, Tehama |

| Colorado | $260–$310 | $520K–$620K | +41% | Boulder, Jefferson, Larimer |

| Oregon | $240–$285 | $480K–$570K | +38% | Jackson, Lane, Clackamas |

| Texas | $195–$240 | $390K–$480K | +35% | Panhandle, Central TX, East TX |

| Florida | $210–$260 | $420K–$520K | +40% | Panhandle, North FL flatwoods |

| Washington | $235–$280 | $470K–$560K | +37% | Okanogan, Chelan, Yakima |

📋 The Wildfire Insurance Claim Process — Step by Step

Immediately After Evacuation (Days 1–3)

Call your insurer's claims line within 24–48 hours — even before you know the full extent of the damage. Early filing establishes your claim date, triggers the ALE process for temporary housing reimbursement, and ensures you are in the queue when adjusters are overwhelmed (which they are after major wildfire events). Document your evacuation route and the condition of your neighbourhood when you left — time-stamped photos and videos from the evacuation are valuable claim evidence. Save all evacuation-related receipts: hotel, meals, pet boarding, temporary storage, and clothing purchased because you couldn't access your home.

Property Assessment Phase (Days 5–30)

Your insurer will assign a claims adjuster — either an in-house adjuster or an independent adjuster contracted for the event. After a major wildfire, adjusters are overwhelmed — realistic wait times for an adjuster visit in the aftermath of a major California or Texas wildfire are 2–6 weeks. You do not have to wait for the adjuster before beginning emergency mitigation — clearing debris, boarding openings, and preventing further damage are required by most policies and should proceed immediately. Document everything with time-stamped photos before any work begins.

Public adjuster consideration: For losses above $100,000 — which means virtually all wildfire total losses — seriously consider hiring a licensed public adjuster. Public adjusters work for you (not the insurer), assess the full scope of your loss, and prepare a comprehensive claim that typically exceeds what homeowners negotiate independently. Studies consistently show that wildfire claims handled by public adjusters settle for 15–40% more than those managed by the homeowner alone. Public adjusters charge 5–15% of the final settlement.

Personal Property Inventory (Days 5–60)

This is the most labour-intensive part of a wildfire total loss claim. You must document every item lost — furniture, clothing, appliances, electronics, books, kitchenware, tools, sporting equipment, and personal items. If you maintained a home inventory (photos, video, receipts stored off-site or in the cloud), this process is manageable. Without prior documentation, you are relying entirely on memory to reconstruct years of accumulated belongings. Use your credit card and bank statements to identify past purchases. Many public adjusters specialise in personal property inventory and significantly increase recovery by identifying items homeowners forget.

Settlement Negotiation (Days 30–180)

The insurer's initial settlement offer is rarely final and is often significantly below what a homeowner is entitled to receive. The insurer will estimate rebuild costs using their proprietary estimating software (typically Xactimate) — these estimates frequently underestimate California and high-cost construction markets. If you believe the estimate is too low, obtain independent contractor bids for the rebuild scope and present them as evidence. Request an itemised breakdown of every component of the insurer's estimate. Any disputed items can be submitted to the appraisal process defined in your policy — most HO-3 policies include an appraisal clause where each party selects an independent appraiser and a neutral umpire resolves disputes.

⚠️ Why Wildfire Claims Get Denied — 7 Critical Reasons

Reason 1 — Underinsurance / Coverage A Inadequacy

The most common "partial denial" — the insurer pays the full Coverage A limit, but that limit is less than the actual rebuild cost. This is not technically a denial, but the homeowner receives less than full replacement cost and must cover the gap themselves. Solution: increase Coverage A to match current replacement cost, and add an Extended Replacement Cost endorsement (typically 25–50% above Coverage A) as a buffer against construction cost increases after a loss.

Reason 2 — Policy Non-Renewal Before the Fire

Multiple major insurers have non-renewed policies in California, Colorado, and Oregon wildfire risk zones. If your policy was non-renewed and you did not secure replacement coverage before the fire, you are uninsured. This situation affects thousands of homeowners who missed non-renewal notices or could not secure replacement coverage. If you received a non-renewal notice and your home subsequently burned, consult an attorney immediately — the insurer's obligations depend on whether proper notice was given and whether you had a grace period.

Reason 3 — Policy Lapse Due to Non-Payment

A policy that lapsed for non-payment provides no coverage for losses after the lapse date. If your mortgage servicer is supposed to pay your homeowners insurance from an escrow account and failed to do so, you may have a claim against the servicer. If you are responsible for payment and missed it, coverage was void from the lapse date.

Reason 4 — Material Misrepresentation at Application

If you misrepresented your property's characteristics when applying for insurance — square footage, construction type, proximity to brush, prior claims history, number of stories — the insurer may deny the claim or rescind the policy on the basis of material misrepresentation. This is most commonly an issue when properties are significantly renovated or expanded after policy issuance without updating the policy.

Reason 5 — Failure to Maintain the Property

Some policies contain maintenance obligations — keeping defensible space clear, maintaining fire-resistant landscaping within the property perimeter, or ensuring that roof and vent covers meet current fire-resistant standards. If an insurer can demonstrate that you failed to maintain these conditions and that the failure contributed to the loss or its severity, they may reduce or deny coverage.

Reason 6 — Smoke Damage Dispute

Smoke damage is a particularly contentious area of wildfire claims. Smoke penetrates HVAC systems, walls, and structural materials in homes that were not directly burned. Insurers sometimes deny or minimise smoke damage claims for properties that were not directly destroyed, arguing that damage is cosmetic or pre-existing. Document smoke damage extensively with air quality measurements, professional assessments, and odour testing immediately after re-entry — this documentation is essential for a successful smoke damage claim.

Reason 7 — Arson Investigation

When the cause of a wildfire is unclear or when an individual fire is suspected to be intentionally set, the insurer may conduct an arson investigation before paying. Investigations can delay claims by 6–18 months even when the homeowner had no involvement in the fire's origin. If your claim is subject to an arson investigation, retain legal counsel early — the insurer's investigation team is not acting in your interest.

🏠 Total Loss Claims — Your Rights and How to Maximise Your Payout

A total loss determination — when rebuilding is not economically feasible or the structure is destroyed — triggers specific rights and processes that differ from partial loss claims.

Your Right to the Full Coverage A Limit

In a declared total loss, you are entitled to receive the full Coverage A limit even if the insurer's own rebuilding estimate is lower. Many homeowners do not know this — if your Coverage A limit is $650,000 and the insurer's rebuild estimate is $580,000, you are still entitled to the full $650,000 for a total loss claim in most states. California law (and similar statutes in several other states) specifically protects this right.

Cash vs Rebuild — Your Choice

In most states, you have the right to take the cash equivalent of the Coverage A limit rather than rebuilding. Some homeowners — particularly seniors, those without children, or those who decide to relocate rather than rebuild — prefer the cash. The cash settlement is typically the Coverage A limit minus your deductible. If you choose cash, ensure your personal property and ALE settlements are negotiated separately before finalising the dwelling settlement.

Extended Replacement Cost Endorsement

If your policy includes an Extended Replacement Cost endorsement (25–50% above Coverage A) and your rebuild cost exceeds your Coverage A limit, the extended coverage activates to cover the gap — up to the endorsement limit. This endorsement is the single most important underinsurance protection for wildfire-prone homeowners. If your policy does not currently include it, contact your insurer before next fire season.

🏨 Additional Living Expenses (ALE) — What Coverage D Actually Pays

ALE coverage pays the difference between your normal living costs and the higher costs incurred because you are displaced from your home. It covers: temporary rental housing (the incremental cost above your normal housing payment), meal costs above your normal grocery budget (not the full restaurant bill — the increment above what you would normally spend on food), pet boarding, storage for salvaged belongings, laundry costs when you lack access to your washer/dryer, and transportation costs above your normal commute if temporary housing requires a longer commute.

What ALE does not cover: your mortgage payment on the damaged home (you must continue paying your mortgage regardless of displacement), your property taxes, or your normal living expenses that you would have incurred anyway. The calculation is the incremental cost of displacement — not a blank cheque for living expenses.

Maximising ALE Recovery

Keep every receipt from the displacement period. Calculate and document the normal monthly cost of each expense category before displacement — this baseline is what you subtract from actual costs to determine the incremental ALE claim. If ALE limits are exhausted before your home is rebuilt (common for California total losses with 18–36 month rebuild timelines), consult your policy's specific language and your state's ALE duration requirements. California requires ALE coverage for at least 24 months for total losses — regardless of the dollar limit — under recent legislation.

🚨 Wildfire Insurance Non-Renewals — What Homeowners Can Do

Since 2023, State Farm, Allstate, Farmers, and several other major insurers have issued mass non-renewals or restricted new business in California, Oregon, and Colorado wildfire risk zones. Over 180,000 California homeowners received non-renewal notices from major carriers between 2024 and 2026. If you receive a non-renewal notice, you have several options:

Option 1 — Shop the independent and specialty market. Lloyd's of London syndicates, Palomar Insurance, and several regional specialty insurers continue to write wildfire-exposed properties. Independent insurance brokers with surplus lines access can often find coverage where standard market insurers have withdrawn. Expect significantly higher premiums — $4,000–$12,000 annually for a California wildfire-zone home versus $1,500–$3,500 from standard market.

Option 2 — California FAIR Plan (insurer of last resort). The California FAIR Plan provides basic fire insurance to homeowners who cannot obtain coverage in the standard market. Coverage is limited ($3M maximum dwelling, no liability coverage, limited personal property), premiums are high, and coverage breadth is narrow. Supplement the FAIR Plan with a "Difference in Conditions" (DIC) policy from a surplus lines insurer to add liability, personal property, and ALE coverage. Many other states have similar insurer-of-last-resort programmes.

Option 3 — Mitigation-based re-qualification. Some insurers have created programmes where homeowners who complete specific wildfire mitigation improvements — Class A roofing, ember-resistant vents, non-combustible siding, defensible space clearing — can re-qualify for standard market coverage. The California Department of Insurance's Safer from Wildfires programme provides a framework for these improvements, and several insurers have committed to reviewing non-renewed policies when mitigation criteria are met.

🏆 Which Insurers Handle Wildfire Claims Best in 2026

| Insurer | Wildfire Claim Rating | Availability (CA) | Key Strength | Key Weakness |

|---|---|---|---|---|

| Chubb | ⭐⭐⭐⭐⭐ 🏆 | Limited — select areas | Best claims service · Wildfire mitigation team | Premium-priced · Selective underwriting |

| USAA | ⭐⭐⭐⭐⭐ 🏆 | Limited — military only | Highest satisfaction · Fast settlement | Military families only |

| Travelers | ⭐⭐⭐⭐ | Partial — some CA | Green rebuild coverage · Strong ALE | Restricting in high-risk zones |

| Palomar | ⭐⭐⭐⭐ | ✅ Wildfire speciality | Writes wildfire zones others decline | Higher premium than standard market |

| State Farm | ⭐⭐⭐⭐ | ❌ Non-renewing CA | Good claims service where writing | Exited most CA wildfire-zone new business |

| CA FAIR Plan | ⭐⭐⭐ | ✅ Last resort | Available when others decline | Limited coverage · Higher cost · No liability |

For a complete review of home insurance providers beyond wildfire-specific analysis, see our full guide: Best Home Insurance Companies USA 2026. For commercial property wildfire coverage, see our Chubb vs AIG vs Travelers commercial property comparison.

🔥 Wildfire Mitigation — Protect Your Property and Keep Your Policy

Zone 0 — The Home Ignition Zone (0–5 feet)

The most critical area for survival in a wildfire. Remove all combustible materials from contact with the structure — wood mulch, firewood, propane tanks, patio furniture, wood decking. Use non-combustible alternatives (gravel, concrete, stone) in the immediate home perimeter. Clean gutters of leaves and debris that can ignite from ember showers. Install ember-resistant vent covers on all attic, crawlspace, and soffit vents — ember intrusion through vents is the most common mechanism of structure ignition in wildfire events.

Zone 1 — Lean, Clean and Green (5–30 feet)

Create a lean, clean, and green buffer zone immediately adjacent to the structure. Remove dead vegetation, maintain living plants with high moisture content, space trees at minimum 10-foot canopy separation, and prune tree limbs to a minimum height of 6–10 feet above the ground (removing ladder fuels that allow fire to climb from ground to canopy). Remove all wood structures (pergolas, wood fences connecting to the house, wood retaining walls) or replace with non-combustible alternatives.

Zone 2 — Reduced Fuel Zone (30–100 feet)

Reduce fuel continuity — spacing and thinning of vegetation to prevent fire from spreading rapidly through the zone. Remove dead vegetation, fallen limbs, and accumulated debris. Maintain separation between tree canopies. This zone requires less intensive management than Zones 0 and 1 but significantly reduces the energy of a fire reaching your home's perimeter.

Class A Roofing and Exterior Improvements

The roof is the single most critical structural component for wildfire survival. Class A fire-rated roofing (concrete or clay tile, metal roofing, or Class A asphalt shingles) dramatically reduces ember ignition risk. If your home has wood shingle or shake roofing, replacing it with Class A material before fire season is the single highest-impact mitigation investment available. Some California insurers offer 10–20% premium discounts for verified Class A roofing. Non-combustible siding (fibre cement, stucco, brick, concrete) adds additional protection but has less impact than roofing on overall ignition probability.

❓ Frequently Asked Questions — Wildfire Insurance Claims 2026

Does homeowners insurance cover wildfire damage?

Yes — standard homeowners insurance (HO-3 policies) covers wildfire damage in virtually all US states. Wildfire is a covered peril under the dwelling coverage, other structures coverage, personal property coverage, and additional living expenses coverage of a standard HO-3 policy. Unlike flood or earthquake, wildfire is not excluded from standard policies — it is explicitly covered. However, coverage adequacy is the critical issue: if your Coverage A limit is below the actual cost to rebuild your home (which affects 67% of California wildfire victims according to 2026 data), you will receive less than full rebuilding compensation. Always verify that your Coverage A limit reflects current construction costs, which have increased 35–55% since 2022.

How long does a wildfire insurance claim take to settle?

Wildfire insurance claim settlement timelines vary widely. Partial damage claims (smoke damage, exterior fire damage without total loss) typically settle within 30–90 days. Total loss claims are significantly more complex — settlement of the dwelling component alone typically takes 6–18 months from the fire date, as it involves adjuster assessment, scope of loss development, insurer estimating, negotiation, and approval. Personal property settlements often take 3–12 months because they require detailed inventory documentation. Additional living expenses are paid on an ongoing basis throughout displacement. Major California wildfires like the 2025 events produced some claims that took 24–36 months to fully settle due to adjuster capacity constraints, contractor availability issues, and rebuilding permit backlogs.

What should I do immediately after a wildfire damages my home?

The first priority is safety — do not re-enter until authorities confirm it is safe. Once safe: call your insurer's claims line within 24–48 hours to open your claim and start ALE coverage; save all evacuation receipts (hotel, meals, pet boarding, clothing) from day one; document your property condition with time-stamped photos and video before any cleanup; do not discard any debris or damaged items until the adjuster has visited or you have your own photographs; begin emergency mitigation (boarding, tarping) to prevent additional damage, which is typically required by your policy; and consider contacting a public adjuster for total losses above $100,000. If you cannot reach your insurer or are experiencing coverage disputes, contact your state's Department of Insurance for free assistance.

What is the average wildfire insurance payout in 2026?

Average wildfire insurance payouts vary dramatically based on loss severity. For partial damage claims (smoke, exterior fire damage), average payouts range from $15,000–$80,000. For total loss claims in California — the largest wildfire insurance market — the average 2026 payout is approximately $380,000 for dwelling coverage alone, plus $95,000 for personal property, plus $45,000–$120,000 for additional living expenses over the displacement period — a total average of $520,000–$595,000 for a complete total loss claim in California. However, these averages mask significant underinsurance — many homeowners with $650,000+ actual rebuild costs receive only $380,000–$420,000 because their Coverage A limits were not updated to reflect construction cost inflation since 2022.

What is a public adjuster and should I hire one for a wildfire claim?

A public adjuster is a licensed professional who represents your interests — not the insurer's — in preparing, documenting, and negotiating your insurance claim. Unlike the insurer's adjuster (whose job is to settle claims within policy terms at the lowest reasonable cost), a public adjuster's financial incentive is aligned with yours: they typically charge 5–15% of the final settlement, so they earn more when you receive more. Multiple independent studies of California wildfire claims have found that settlements managed by public adjusters are 15–40% higher than comparable claims managed by homeowners alone — because public adjusters know the full scope of covered losses, construct comprehensive inventories, and understand how to negotiate within policy terms. For any wildfire total loss claim, hiring a public adjuster is typically worth the fee. Verify that any public adjuster you hire is licensed by your state's Department of Insurance before signing a contract.

My insurer non-renewed my California home policy — what are my options?

If a major insurer has non-renewed your California home policy, you have several options. First, work with an independent insurance broker who has access to the surplus lines market — Lloyd's of London syndicates, Palomar Insurance, and regional specialty carriers continue to write California wildfire-zone homes, though at significantly higher premiums. Second, the California FAIR Plan provides basic fire coverage as an insurer of last resort — supplement it with a Difference in Conditions (DIC) policy for liability and fuller coverage. Third, invest in qualifying wildfire mitigation improvements (Class A roofing, defensible space, ember-resistant vents) and request reconsideration from your previous insurer or new carriers under California's Safer from Wildfires programme. Fourth, contact the California Department of Insurance's consumer hotline — they can connect you with resources and verify whether your non-renewal was properly executed under California law.

✅ Final Summary — Wildfire Insurance Claims 2026

Wildfire is a covered peril — but coverage adequacy, not coverage existence, is the critical issue for most homeowners in wildfire-risk states. Update your Coverage A limit to match current rebuild costs annually, add an Extended Replacement Cost endorsement as a buffer, ensure your ALE coverage has sufficient duration for a total loss scenario, and document your personal property with a detailed home inventory stored off-site. If a wildfire damages your property, file immediately, document everything, and consider a public adjuster for total losses. For complete home insurance comparison beyond wildfire, see our guide at Best Home Insurance Companies USA 2026.

Disclaimer: This article provides general information about wildfire insurance claims. Coverage terms, state laws, and insurer availability change frequently. Always review your specific policy terms and consult a licensed insurance professional for advice on your individual situation. Nexuora does not provide legal or claims advice. Updated April 23, 2026.

Ahmada Ndao is a financial research analyst and independent journalist

specializing in US consumer finance, legal rights, and insurance markets.

With over 5 years covering American financial products, he has helped

thousands of readers navigate complex insurance decisions, find the right

legal representation, and optimize their credit strategies. His research

methodology combines primary data analysis, direct outreach to industry

professionals, and continuous monitoring of federal regulatory changes.

Ahmada’s work has been cited by financial communities across the US and

reviewed by licensed attorneys and insurance professionals for accuracy.