Best High Interest Savings Accounts Canada 2026 — Top HISA Rates, FHSA Explained & TFSA vs RRSP vs HISA Compared

The Bank of Canada held its overnight rate at 2.25% on March 18, 2026 — meaning Canadian HISA rates will stay at current levels for at least another six weeks, making this the best window in years to lock in a high-interest savings strategy before rates potentially decline further. The best high interest savings account in Canada for 2026 is the EQ Bank Personal Account, which has consistently offered one of the most competitive everyday interest rates on the market. But EQ Bank is just one of a rapidly expanding field of digital and online banks offering Canadians rates 4–6x higher than the Big Five banks — with no monthly fees, no minimum balance requirements, and full CDIC deposit insurance. This guide ranks the best high interest savings accounts in Canada for 2026 using real rates verified on March 21, 2026, explains the FHSA (Canada's newest registered account), compares TFSA vs HISA vs RRSP with specific examples, and gives every Canadian the complete strategy to maximize their savings in the current rate environment.

Key Facts — Best HISA Canada 2026

- EQ Bank Personal Account is Canada's best overall HISA — 2.75% with no fees, no minimum balance, full CDIC coverage, Schedule I chartered bank (same regulatory tier as TD and RBC)

- KOHO Everything offers the highest everyday rate at 3.50% — but the $19/month fee only makes sense if you spend $800+/month on the KOHO card

- Simplii Financial offers the best promotional rate — 4.50% for the first 5 months on new accounts (0.30%–1.50% after), plus $300 cash bonus for new clients

- Neo Financial offers up to 3.00% with a $650 welcome bonus for new accounts funded by March 22, 2026

- Oaken Financial offers 2.80% — best for those who prefer a dedicated savings-only account with no spending features

- Bank of Canada held at 2.25% on March 18, 2026 — no rate cuts expected for most of 2026, meaning HISA rates are stable

- HISA interest is taxable — report on T5 slip at your marginal rate. To avoid tax, hold your HISA inside a TFSA (contribution room permitting)

- FHSA 2026: First Home Savings Account allows $8,000/year (lifetime $40,000) — tax-deductible contributions AND tax-free withdrawals for first home purchase

- TFSA 2026 limit: $7,000 annual contribution room — cumulative limit $95,000 for those eligible since 2009

- Verify current rates at Ratehub.ca and HighInterestSavings.ca — rates update daily

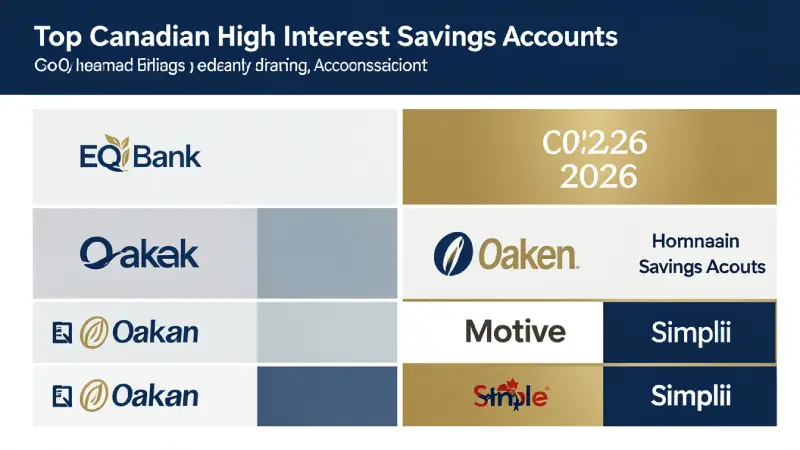

Best High Interest Savings Accounts Canada 2026 — Rates Verified March 21, 2026

| Account | Everyday Rate | Promo Rate | Monthly Fee | Min Balance | CDIC |

|---|---|---|---|---|---|

| EQ Bank Personal Account | 2.75%* | — | $0 | None | ✅ Yes |

| KOHO Everything | 3.50% | — | $19/month | None | ✅ Yes (via Peoples Trust) |

| Simplii Financial HISA | 0.30–1.50% | 4.50% (5 months) | $0 | None | ✅ Yes |

| Neo Financial Savings | 3.00% | Up to $650 bonus | $0 | None | ✅ Yes (via Concentra) |

| Oaken Financial HISA | 2.80% | — | $0 | None | ✅ Yes |

| Tangerine Savings | 0.70% | 4.50% (new clients, 5 months) | $0 | None | ✅ Yes |

| Laurentian Bank HISA | 2.20–3.20% | 3.20% over $100K | $0 | None | ✅ Yes |

| Motive Financial Savvy | 2.80% | — | $0 | None | ✅ Yes |

| Scotiabank MomentumPLUS | 0.80% | Varies by term | $0 | None | ✅ Yes |

| Big 5 Banks (avg TD/RBC/BMO) | 0.40–0.80% | Occasional promotions | $0–$4 | None–$500 | ✅ Yes |

*EQ Bank 2.75% rate requires monthly direct deposit of at least $2,000. Base rate without direct deposit: 1.00%. Rates as of March 21, 2026 — verify at each institution before applying.

Strengths

- 2.75% everyday rate — no promotional gimmicks

- No monthly fees, no minimum balance, no transfer fees

- Schedule I chartered bank — same regulatory tier as Big Six

- Full CDIC deposit insurance ($100,000 per category)

- No-FX-fee prepaid card for international spending

- TFSA, RRSP, and FHSA versions available

Limitations

- Full 2.75% requires $2,000/month direct deposit (1.00% without)

- No physical branches — digital only

- Transfers to external banks can take 1–2 business days

Strengths

- 4.50% promotional rate — highest available for new clients

- $300 cash bonus + $50 Skip gift card for new chequing clients

- No minimum balance, no monthly fees

- CDIC insured via CIBC ownership

- Free unlimited Interac e-Transfers

Limitations

- Rate drops to 0.30–1.50% after 5-month promotional period

- Best used as a short-term strategy, then transfer to EQ Bank

Strengths

- 3.00% everyday rate — higher than EQ Bank standard

- $650 welcome bonus — exceptional new account incentive

- No fees, no minimum balance

- CDIC insured via Concentra Bank

Limitations

- $650 bonus requires March 22, 2026 deadline for funding

- Newer institution — less established history than EQ Bank

- Rate may change more frequently than established players

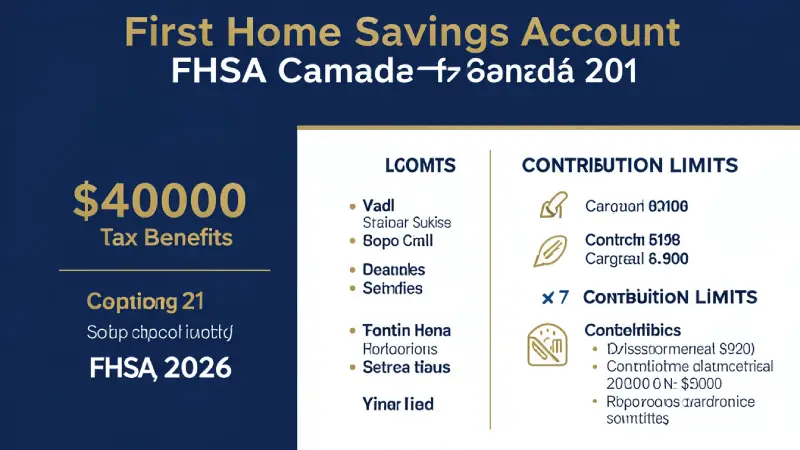

The FHSA — Canada's Best New Savings Account Explained

The First Home Savings Account (FHSA) launched in April 2023 and is arguably the most powerful savings tool ever introduced in Canada for eligible first-time homebuyers. It combines the best features of both the RRSP and TFSA into a single account designed specifically for saving toward a first home purchase.

| Feature | FHSA Details |

|---|---|

| Annual Contribution Limit | $8,000 per year |

| Lifetime Contribution Limit | $40,000 total |

| Tax Deduction | Yes — contributions reduce your taxable income (like RRSP) |

| Withdrawals for First Home | 100% tax-free (like TFSA) |

| Non-Home Withdrawal | Taxed as income (like RRSP withdrawal) |

| Eligibility | Canadian residents, 18+, first-time homebuyer (no owned home in past 4 years) |

| Account Duration | Must use within 15 years of opening, or transfer to RRSP |

| Carry-Forward Room | Up to $8,000 of unused room carries forward one year |

| Can Hold HISA Inside | Yes — earn interest tax-sheltered |

| Couples Advantage | Each partner can open separately — $80,000 combined tax-free |

💡 FHSA + HBP strategy: The FHSA can be combined with the RRSP Home Buyers' Plan (HBP) — allowing first-time buyers to withdraw up to $35,000 from their RRSP in addition to their full FHSA balance. A couple using both accounts could access $40,000 FHSA + $35,000 RRSP + $40,000 partner FHSA + $35,000 partner RRSP = $150,000 in tax-sheltered funds for a first home down payment. This combination is the most powerful first-home financial tool available anywhere in the developed world. Open your FHSA immediately if you are eligible — contribution room does not accumulate until the account is open at Canada.ca.

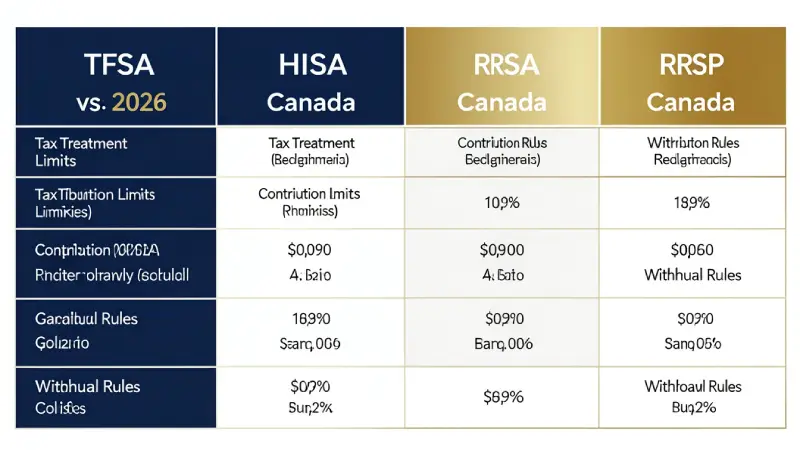

TFSA vs HISA vs RRSP — Which Account is Right for You?

| Account | Tax on Contribution | Tax on Growth | Tax on Withdrawal | 2026 Limit | Best For |

|---|---|---|---|---|---|

| TFSA | No deduction | Tax-free | Tax-free | $7,000/yr (cumulative $95,000) | Most goals — emergency fund, short/mid-term savings, retirement |

| FHSA | Tax-deductible ✅ | Tax-free | Tax-free (first home) | $8,000/yr ($40,000 lifetime) | First-time homebuyers ONLY — the most powerful account available |

| RRSP | Tax-deductible ✅ | Tax-deferred | Taxed as income | 18% of prior year income (max $31,560 in 2026) | Retirement savings (expect lower tax bracket in retirement) |

| HISA (unregistered) | No deduction | Taxable annually (T5) | No tax | Unlimited | Emergency fund, short-term savings beyond TFSA/FHSA room |

| GIC | No deduction | Taxable (unless registered) | No tax | Unlimited (term locked) | When you can lock up funds for 1–5 years for higher guaranteed rates |

✅ The optimal Canadian savings priority order for 2026:

1st — TFSA: Fill your TFSA first. Tax-free growth on every dollar, withdrawals tax-free at any time, for any purpose. 2026 limit: $7,000 (cumulative $95,000 if eligible since 2009).

2nd — FHSA (if buying a home): Open immediately if eligible. $8,000/year, tax-deductible AND tax-free on withdrawal — the best of RRSP and TFSA in one account.

3rd — RRSP: After TFSA is maxed, contribute to RRSP especially if in a high tax bracket — the deduction reduces current-year taxes most effectively at 40%+ marginal rates.

4th — Unregistered HISA: For savings beyond registered account limits — use EQ Bank at 2.75% or Simplii promotion at 4.50% for 5 months.

Bank of Canada Rate Outlook 2026 — What It Means for Your Savings

The Bank of Canada's decision to hold its overnight lending rate at 2.25% on March 18 means at least another six weeks of the status quo for Canadian savers. The Bank isn't expected to raise the overnight rate for most of 2026, so GIC and HISA rates might be as good as they're going to get for the foreseeable future.

What this means for your strategy:

- Lock in GIC rates now if you won't need the funds for 1–3 years. GIC rates are currently 3.5–4.5% for 1-year terms — higher than most everyday HISA rates and guaranteed for the full term

- Keep your emergency fund in a HISA for liquidity — the 2.75% from EQ Bank is reasonable for funds you may need within 90 days

- HISA rates may decrease further if the Bank of Canada cuts rates in late 2026 — which some economists predict. Use promotional rates (Simplii 4.50%, Tangerine 4.50%) while they are available

- A high interest savings account and a tax free savings account (TFSA) seem similar, but are typically used for very different purposes. A HISA is a basic savings account with a competitive interest rate, designed to help you grow your savings while keeping your money easily accessible. On the other hand, a TFSA is a tax-advantaged account that allows you to invest and save money without paying taxes on the interest, dividends, or capital gains earned within the account.

How to Maximize Your Savings Strategy — Checklist 2026

Canadian HISA Savings Optimization Checklist — 2026

- Open a TFSA immediately if you haven't — every year you don't open one, you permanently lose that year's contribution room ($7,000 in 2026)

- If you are a first-time homebuyer, open an FHSA immediately — contribution room begins accumulating from the day you open the account at canada.ca

- Hold your HISA inside your TFSA whenever possible — you earn the same interest rate but the income is completely tax-free

- Open an EQ Bank account for ongoing everyday savings — 2.75% with no fees, full CDIC protection, and no minimum balance

- Capture promotional rates: Simplii 4.50% for 5 months on new accounts — use for a lump sum while the promo runs, then transfer to EQ Bank

- If you can't meet EQ Bank's $2,000/month direct deposit: Oaken Financial at 2.80% has no conditions and no fees

- For savings you won't need for 1+ years: compare GIC rates — currently 3.5–4.5% for 1-year terms at Oaken, EQ Bank, and Peoples Trust — higher than everyday HISA rates

- Never keep more than $100,000 at one institution per category — CDIC covers only $100,000 per insured category per bank

- Report all HISA interest on your tax return via T5 slip — interest earned in unregistered accounts is taxable income

- Review rates every 3 months at Ratehub.ca — promotional offers change frequently and switching takes minutes

FAQ — Best HISA Canada 2026

Ahmada Ndao is a financial research analyst and independent journalist

specializing in US consumer finance, legal rights, and insurance markets.

With over 5 years covering American financial products, he has helped

thousands of readers navigate complex insurance decisions, find the right

legal representation, and optimize their credit strategies. His research

methodology combines primary data analysis, direct outreach to industry

professionals, and continuous monitoring of federal regulatory changes.

Ahmada’s work has been cited by financial communities across the US and

reviewed by licensed attorneys and insurance professionals for accuracy.