The right business credit card can be one of the most powerful financial tools in your company’s arsenal in 2026. Beyond simply separating personal and business expenses, the best cards now deliver significant cashback, travel rewards worth thousands of dollars, and signup bonuses large enough to fund a meaningful business expense.

But with dozens of options available — from big-bank cards like Chase and American Express to startup-focused products like Brex — choosing the right card requires careful analysis of your actual spending patterns, business structure, and financial goals.

We spent over 120 research hours comparing business card options, analyzing data from CFPB credit card market reports, evaluating rewards redemption values, and reviewing thousands of verified cardholder accounts to produce this comprehensive ranking.

Key Takeaways

- Chase Ink Business Preferred offers the highest signup bonus value among cards with a sub-$100 annual fee

- Amex Blue Business Cash provides the simplest 2% cashback with no annual fee — ideal for consistent spenders

- Capital One Spark Cash Plus remains the strongest unlimited cashback card for high-spending businesses

- Brex is the best option for funded startups that cannot meet personal guarantee requirements

- New LLCs can qualify using personal credit history at most major issuers

- Combining a travel card with a flat-rate cashback card often maximizes total rewards value

Best Business Credit Cards Ranked for 2026

Our complete ranking evaluates each card across six criteria: rewards rate, signup bonus value, annual fee, approval accessibility, business-specific benefits, and customer service quality.

| Credit Card | Best For | Annual Fee | Top Rewards | Signup Bonus Value | Our Rating |

|---|---|---|---|---|---|

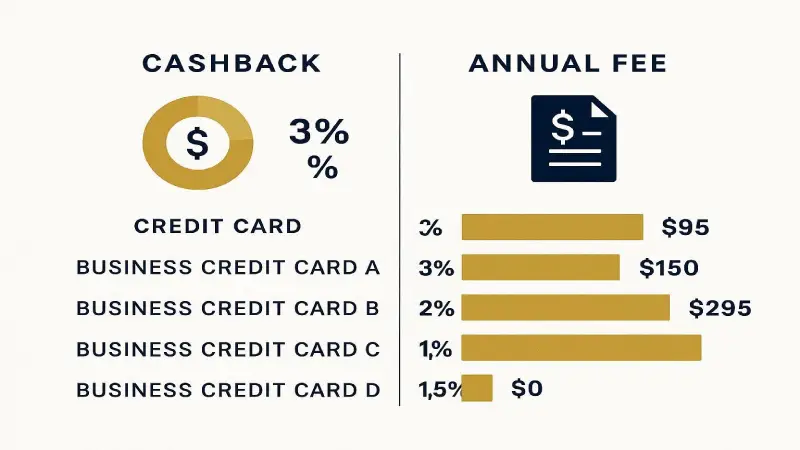

| Chase Ink Business Preferred | Travel rewards | $95 | 3x points on travel & select categories | ~$1,250 | ★★★★★ 4.9 |

| Amex Blue Business Cash | Simple cashback | $0 | 2% cashback on all purchases | $250 | ★★★★½ 4.7 |

| Capital One Spark Cash Plus | High spenders | $150 | Unlimited 2% cashback | $2,000 | ★★★★½ 4.6 |

| Brex Business Card | Funded startups | $0 | Category-based startup rewards | Varies | ★★★★ 4.4 |

| Bank of America Business Advantage | Low APR / flexibility | $0 | 1.5–3% cashback | $300 | ★★★★ 4.3 |

| Chase Ink Business Cash | Office & internet spending | $0 | 5% on select categories | $350 | ★★★★ 4.5 |

| Amex Business Gold Card | Premium travel | $295 | 4x points in top 2 categories | ~$1,800 | ★★★★ 4.4 |

Signup bonus values are approximate based on standard redemption rates as of May 2026. Point valuations use Nexuora’s average redemption methodology. Terms and availability are subject to change.

Best Cashback Business Credit Cards

Cashback cards are the most popular category for small business owners in 2026 because they deliver simple, predictable value without requiring knowledge of complex points systems or travel redemption strategies.

American Express Blue Business Cash™ Card

Best for: Established small businesses with consistent monthly spending under $50,000/year

The Amex Blue Business Cash earns a flat 2% cashback on all eligible purchases up to $50,000 per calendar year, then 1% after that. For most small businesses, this cap is rarely reached, making it an effectively unlimited 2% card with no annual fee — one of the strongest no-fee cashback structures available anywhere in 2026.

✓ Pros

- No annual fee

- Simple flat-rate structure

- Amex Expanded Buying Power feature

- Expense management tools

- Intro APR offer on purchases

✗ Cons

- 2% capped at $50,000/year

- Amex not accepted everywhere

- Modest signup bonus vs competitors

Capital One Spark Cash Plus

Best for: High-revenue businesses spending $150,000+ annually

The Capital One Spark Cash Plus is a charge card (not a revolving credit card) that offers unlimited 2% cashback with no cap. The annual fee of $150 is effectively refunded if you spend $150,000+ per year. The tiered signup bonus — up to $2,000 in cash — makes this one of the highest-value signup bonuses available on any business cashback card in 2026.

✓ Pros

- Unlimited 2% — no cap

- Massive signup bonus potential

- Annual fee refunded at $150K+ spend

- No preset spending limit

- Free employee cards

✗ Cons

- Must pay balance in full monthly

- $150 annual fee

- Requires excellent credit

Looking for the best personal cashback cards for your business owners? See our guide: Best Cashback Credit Cards USA 2026

Best Travel Rewards Business Credit Cards

Travel rewards cards deliver significantly higher per-dollar value than cashback cards — but only if you redeem points strategically for flights, hotels, or transfers to airline and hotel loyalty programs. For businesses where decision-makers travel frequently, the right travel card can deliver 3–5 cents of value per dollar spent, far exceeding any cashback rate.

Chase Ink Business Preferred® Credit Card

Best for: Travel-heavy businesses and entrepreneurs who transfer to airline/hotel partners

The Chase Ink Business Preferred is widely regarded as the single best business credit card for travel rewards in 2026. It earns 3x Chase Ultimate Rewards points on travel, shipping, advertising on social media and search engines, and internet/cable/phone services — covering the spending categories most common to modern businesses.

Chase Ultimate Rewards points are worth approximately 1.25–2.0 cents each when redeemed through the Chase Travel portal or transferred to partners like United Airlines, Hyatt, British Airways, and Marriott.

✓ Pros

- Massive signup bonus relative to $95 fee

- Flexible Ultimate Rewards ecosystem

- Cell phone protection benefit

- Trip delay and cancellation insurance

- 3x on digital advertising spend

✗ Cons

- 3x capped at $150,000/year

- Requires good-to-excellent credit

- Points devalue if transferred poorly

American Express® Business Gold Card

Best for: Businesses with high spending concentrated in 1–2 categories

The Amex Business Gold Card automatically earns 4x Membership Rewards points in the two categories where your business spends the most each month. Eligible categories include airfare, digital advertising (including Google and Facebook ads), shipping, restaurants, gas stations, and select technology providers. For agencies or eCommerce businesses with high digital ad spend, this card’s rewards rate can be extraordinary.

Best Business Credit Cards for Startups and LLCs

Startups and newly formed LLCs face unique challenges when applying for business credit cards. Many premium cards require 2+ years of business history or minimum revenue thresholds that new companies cannot meet. Several specialized options address this gap.

| Card | Personal Guarantee? | Business Age Req. | Annual Fee | Best Feature |

|---|---|---|---|---|

| Brex Business Card | Not required (some) | None | $0 | Software-integrated expense management |

| Capital on Tap | Yes | 1 year | $0 | Easy approval for small businesses |

| Amex Blue Business Cash | Yes | None (uses personal credit) | $0 | No-fee 2% cashback from day one |

| Chase Ink Business Cash | Yes | None (uses personal credit) | $0 | 5% cashback on office categories |

| Ramp Corporate Card | Not required | None | $0 | AI-powered spend management platform |

Brex Business Card

Brex remains the leading business card product designed specifically for startups in 2026. Unlike traditional issuers, Brex evaluates businesses based on bank balances, investors, and revenue trajectory rather than personal credit scores. For VC-backed startups or businesses with strong cash balances, Brex can provide credit limits that would be impossible to achieve through traditional channels.

Brex integrates directly with accounting software including QuickBooks, Xero, and NetSuite, making it particularly attractive for startups building financial infrastructure from scratch.

New LLC Credit Card Strategy

For entrepreneurs who just formed an LLC, the fastest path to business credit is to apply for cards that evaluate your personal credit history during the early years. According to the U.S. Small Business Administration, building dedicated business credit — separate from personal credit — is one of the most important financial steps for any new company.

Best Business Credit Cards With No Annual Fee

No-fee business cards have become significantly more competitive in recent years. The gap in rewards between no-fee and premium cards has narrowed substantially, making the no-fee tier an excellent default choice for most small businesses.

| Card | Cashback / Rewards Rate | Signup Bonus | Notable Benefit |

|---|---|---|---|

| Amex Blue Business Cash | 2% flat cashback | $250 | Expanded Buying Power feature |

| Chase Ink Business Cash | 5% on select categories | $350 | 5% on office supply stores, internet, and cable |

| Chase Ink Business Unlimited | 1.5% unlimited cashback | $350 | Simple flat rate, no category tracking |

| Bank of America Business Advantage Cash Rewards | 3% in chosen category | $300 | Choose your highest-earning category |

| Brex Business Card | Varies by category | Varies | No personal guarantee for eligible startups |

No-Fee vs. Premium Cards: Which Wins?

For businesses spending under $60,000/year, a no-fee card like the Chase Ink Business Cash or Amex Blue Business Cash typically delivers better net value than a premium card. Above $100,000 in annual business spending, premium cards with strong signup bonuses and higher rewards rates generally pull ahead — sometimes by thousands of dollars per year.

How Business Credit Cards Work

Business credit cards function similarly to personal credit cards in their basic mechanics, but they include a set of business-specific features that make them genuinely useful as financial management tools — not just a payment method.

Employee Cards and Spending Controls

Most business credit cards allow you to issue free or low-cost employee cards with individualized spending limits. This eliminates the need for employees to use personal cards for business expenses and then seek reimbursement — a process that creates accounting complexity and delays.

Expense Management Integration

Premium business cards now integrate directly with major accounting platforms. According to QuickBooks research, businesses that integrate credit card data with accounting software reduce bookkeeping time by an average of 40% and experience fewer categorization errors at tax time.

Higher Credit Limits

Business credit cards typically offer credit limits 2–5x higher than comparable personal cards for the same applicant profile. This reflects the higher spending needs of commercial entities compared to individual consumers.

Business Credit History

When you use a dedicated business card responsibly, your company begins building its own credit profile with business credit bureaus — Dun & Bradstreet, Experian Business, and Equifax Business. A strong business credit profile opens the door to better loan rates, higher credit limits, and net-30 vendor relationships that can dramatically improve cash flow.

How to Choose the Right Business Credit Card

With dozens of options available, matching a card to your actual business profile is more important than chasing the highest headline rewards rate. Here’s how to think through the selection process.

Step 1: Analyze Your Spending Categories

Pull your last 3 months of business bank statements and categorize expenses by type — travel, advertising, office supplies, utilities, meals, shipping, etc. This reveals where you can earn the most with category-multiplier cards versus where a flat-rate card is simpler and more lucrative.

Step 2: Evaluate Annual Fee Breakeven

A card with a $95 annual fee like the Chase Ink Preferred needs to deliver at least $95 more in rewards than a no-fee alternative to justify the cost. For most businesses spending $2,000+ per month on the card’s bonus categories, this breakeven is reached quickly.

Step 3: Consider Your Travel Frequency

Travel rewards cards deliver their best value to cardholders who understand how to use airline and hotel transfer partners. If you won’t be booking premium flights or hotel stays using points, a simpler cashback card will almost always deliver more usable value.

Step 4: Understand Approval Requirements

Premium travel cards like the Amex Business Gold or Chase Ink Preferred typically require a personal credit score above 700. New businesses or entrepreneurs rebuilding credit should start with more accessible options and graduate to premium products after 12–18 months of responsible usage.

Step 5: Factor in Your Business Structure

Sole proprietors, partnerships, LLCs, and corporations have different tax reporting requirements and different risk profiles that affect card selection. An LLC owner using a business card solely for business expenses simplifies Schedule C reporting and helps substantiate the business-use deductibility of expenses under IRS guidelines for ordinary and necessary business expenses.

For freelancers and sole proprietors, see our related guide: Best Credit Cards for Freelancers and Self-Employed in 2026

How to Maximize Business Credit Card Rewards in 2026

Getting a great business card is only the first step. Strategic usage can significantly amplify the value you extract from any rewards program.

Pair a Travel Card with a Flat-Rate Cashback Card

Many experienced business card users maintain two cards: a category-specific travel card (Chase Ink Preferred, Amex Business Gold) for their highest-spend categories, and a flat-rate cashback card (Capital One Spark Cash Plus, Amex Blue Business Cash) for everything else. This combination typically delivers blended rewards rates of 2.5–4% across all spending.

Maximize the Signup Bonus

The largest single return on any business credit card is often the signup bonus. Strategically timing a card application to coincide with a known large purchase — equipment, event sponsorship, an annual software subscription — is a common way to meet minimum spend requirements without altering normal spending patterns.

Leverage Employee Cards

Issuing employee cards consolidates company spending onto a single rewards account. Business owners who do not issue employee cards are frequently leaving significant rewards on the table as employees use personal cards for business expenses.

Set Up Auto-Pay

Late fees and interest charges are the single fastest way to negate any rewards value. Setting up automatic full balance payment ensures you never pay interest on a rewards card — maintaining the fundamental premise that rewards cards are only beneficial when you carry no balance.

Frequently Asked Questions

Conclusion: Best Business Credit Cards by Profile in 2026

There is no single « best » business credit card — the right choice depends entirely on your business spending pattern, travel frequency, credit profile, and financial priorities. Here’s our final recommendation by business type:

| Business Type | Recommended Card | Primary Reason |

|---|---|---|

| Frequent traveler / consultant | Chase Ink Business Preferred | Best travel rewards value with modest $95 fee |

| Small business with consistent spending | Amex Blue Business Cash | Simple 2% cashback, no fee, reliable |

| High-revenue business ($150K+ spend) | Capital One Spark Cash Plus | Unlimited 2%, massive signup bonus |

| Funded startup or tech company | Brex or Ramp | No personal guarantee, software integration |

| New LLC or freelancer | Chase Ink Business Cash | No fee, easy approval, strong 5% categories |

| High digital ad spender | Amex Business Gold | 4x points on top 2 spending categories including ads |

For most early-stage businesses, we recommend starting with a no-fee card to build business credit history, then upgrading to a premium travel or high-cashback card once your monthly spending volume justifies the annual fee.

Before applying, always use a business card comparison tool to verify current signup bonus terms — issuers update offers frequently and the best available bonuses change quarterly.

See also: Best Small Business Financing Options 2026 | How to Build Business Credit as a New LLC

Methodology: Nexuora researchers evaluated 34 business credit cards based on publicly available terms as of May 2026. Rewards valuations use our standard point-value methodology averaging cash redemption rates and travel transfer partner values. Annual fee breakeven calculations assume consistent spending at estimated rewards rates. Individual results will vary based on actual spending patterns and redemption choices. Card terms change frequently — always verify current offers directly with the issuer.

Ahmada Ndao is a financial research analyst and independent journalist

specializing in US consumer finance, legal rights, and insurance markets.

With over 5 years covering American financial products, he has helped

thousands of readers navigate complex insurance decisions, find the right

legal representation, and optimize their credit strategies. His research

methodology combines primary data analysis, direct outreach to industry

professionals, and continuous monitoring of federal regulatory changes.

Ahmada’s work has been cited by financial communities across the US and

reviewed by licensed attorneys and insurance professionals for accuracy.