Key Takeaways

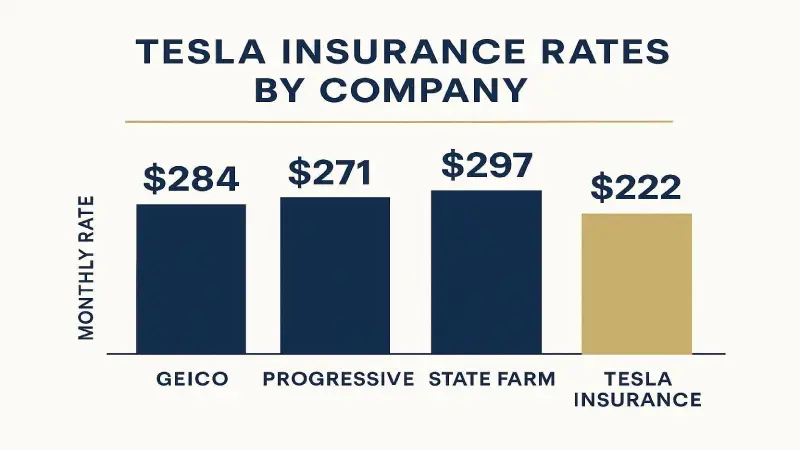

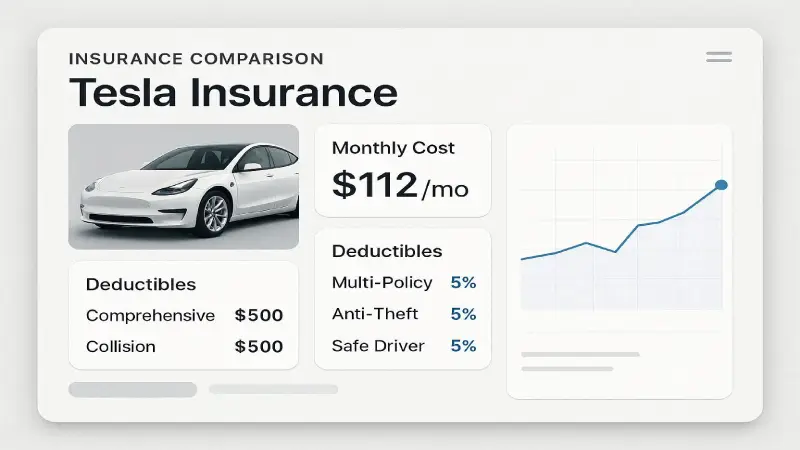

- Tesla Insurance is the cheapest option for safe drivers in states where it’s available

- GEICO offers the strongest nationwide value and easiest bundling options

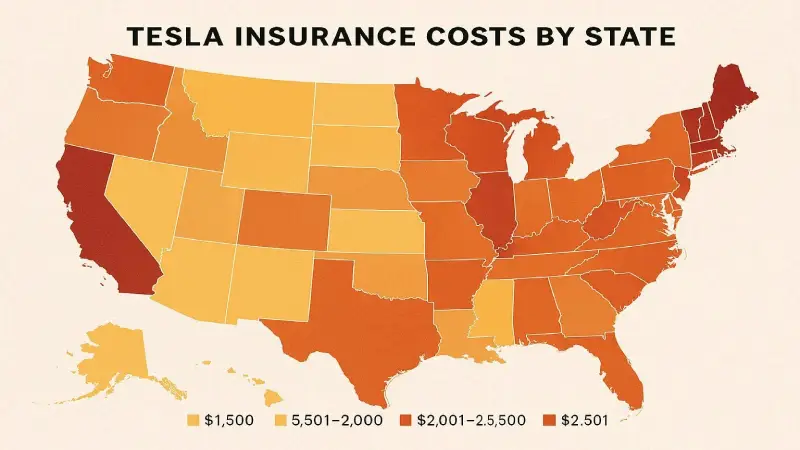

- The average Tesla owner pays $2,400–$4,200 per year for full coverage

- Florida and New York are consistently the most expensive states for Tesla insurance

- Bundling home and auto can save Tesla drivers $400–$900 per year

- Young Tesla drivers under 25 face annual premiums that can exceed $5,000

Tesla-certified repair centers are not available in every city. In regions with few Tesla-approved shops, repairs take longer and cost more, increasing insurer expenses and driving up premiums for all Tesla drivers in those areas.

Florida and New York remain the two most expensive states for Tesla insurance due to a combination of dense traffic, high lawsuit frequencies, and — in Florida’s case — ongoing hurricane and flood risks that affect comprehensive coverage pricing.

For an in-depth look at how state insurance regulations affect your premiums, see our guide: Cheapest Car Insurance by State in 2026.

GEICO insures Tesla vehicles through its traditional auto insurance framework. While it lacks the direct vehicle integration that Tesla Insurance offers, GEICO provides strong nationwide coverage with extensive bundling options.

Advantages:

- Available in all 50 states

- Home + auto bundle savings of $400–$900/year

- Larger agent and customer support network

- More stable premium structure (less fluctuation month to month)

- Multi-car discount for households with multiple vehicles

Disadvantages:

- Typically 8–18% higher premiums than Tesla Insurance for safe drivers

- No direct integration with Tesla vehicle data

- Claims processed through general auto insurance pipeline

Ahmada Ndao is a financial research analyst and independent journalist

specializing in US consumer finance, legal rights, and insurance markets.

With over 5 years covering American financial products, he has helped

thousands of readers navigate complex insurance decisions, find the right

legal representation, and optimize their credit strategies. His research

methodology combines primary data analysis, direct outreach to industry

professionals, and continuous monitoring of federal regulatory changes.

Ahmada’s work has been cited by financial communities across the US and

reviewed by licensed attorneys and insurance professionals for accuracy.