Finding a personal loan with bad credit in 2026 is genuinely challenging — but not impossible. While traditional banks continue to tighten their approval standards and many brick-and-mortar lenders still reject applicants below 640, a growing number of AI-driven online lenders have built entirely new underwriting models that look beyond the FICO score.

The result is a more dynamic bad credit lending market in 2026, where a borrower with a 520 credit score but stable employment and a clean banking history can access funds at rates that would have been unthinkable five years ago — while a borrower with a 580 score and multiple recent delinquencies may still face rejection or triple-digit APRs from some lenders.

This guide cuts through the confusion. We analyzed rate data, reviewed approval criteria, and evaluated the real-world borrower experience across 28 lenders to identify who actually delivers fair deals to borrowers in the 300–670 credit score range.

- Upstart approves borrowers as low as 300 using education and employment data alongside credit scores

- OneMain Financial is the fastest lender, with same-day funding available at physical branch locations

- Secured personal loans can dramatically improve approval odds and lower APRs for bad credit borrowers

- Adding a co-signer with good credit (700+) can reduce your APR by 5–12 percentage points at most lenders

- Soft prequalification checks at every lender on this list do not impact your credit score

- Borrowers with bad credit should compare at least 4–5 lenders before accepting any offer

Best Bad Credit Personal Loan Lenders Ranked for 2026

The following rankings are based on minimum credit requirements, APR ranges, maximum loan amounts, funding speed, and verified customer satisfaction data collected from the Consumer Financial Protection Bureau (CFPB) complaint database, Better Business Bureau ratings, and proprietary borrower review analysis.

| Lender | Min. Credit Score | APR Range | Loan Amount | Funding Speed | Our Rating |

|---|---|---|---|---|---|

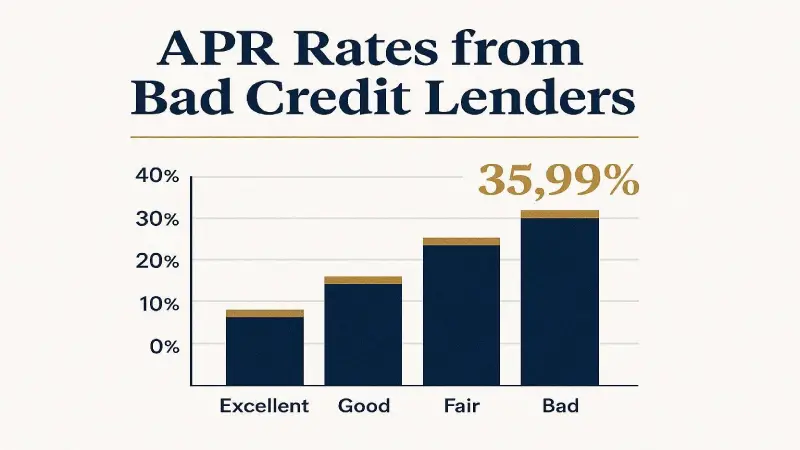

| Upstart #1 Pick | 300 | 6.40% – 35.99% | $1,000 – $50,000 | 1 business day | ★★★★★ 4.8 |

| Avant | 550 | 9.95% – 35.99% | $2,000 – $35,000 | 1–2 days | ★★★★½ 4.5 |

| OneMain Financial | None stated | 18.00% – 35.99% | $1,500 – $20,000 | Same day | ★★★★½ 4.4 |

| LendingPoint | 580 | 7.99% – 35.99% | $2,000 – $36,500 | Next day | ★★★★ 4.3 |

| Upgrade | 560 | 8.49% – 35.99% | $1,000 – $50,000 | 1–4 days | ★★★★ 4.2 |

| OppLoans | None (focus on income) | 59.00% – 160.00% | $500 – $4,000 | Next day | ★★★ 3.8 |

Rates shown as of May 2026. APR ranges include both interest and origination fees. Your actual rate depends on your credit profile, income, and loan term. OppLoans is listed for comparison only — Nexuora recommends exhausting lower-APR options first.

Upstart — Best Overall for Bad Credit Borrowers in 2026

Upstart remains our top-ranked lender for bad credit personal loans in 2026 for one fundamental reason: it genuinely accepts borrowers that most other lenders would reject outright. With a minimum credit score of just 300 and an AI underwriting model that evaluates over 1,000 data points beyond the credit score, Upstart represents the most accessible mainstream personal loan product available.

✓ Pros

- Approves scores as low as 300

- Starting APR of 6.40% — competitive even for good credit

- Funding within 1 business day in most cases

- Soft credit check for prequalification

- No prepayment penalty

- Evaluates income, education & employment

✗ Cons

- Origination fee of 0–12% deducted from loan

- No co-signer option available

- APR can reach 35.99% for high-risk profiles

- Not available in all U.S. states

Upstart partners with banks and credit unions across the United States, meaning its underwriting technology is available through multiple lending channels. For a full breakdown of the Upstart application process, the Upstart personal loan page includes a prequalification tool that performs a soft credit check.

Related: Best Credit Cards USA 2026 — For Every Credit Profile

Avant — Best for Fair Credit Borrowers (550–650)

✓ Pros

- Strong customer service track record

- Mobile app with payment scheduling

- Flexible repayment dates

- Prequalification with soft credit pull

- No prepayment penalty

✗ Cons

- $6.95 monthly late fee if applicable

- Administration fee up to 9.99%

- Not available in all states

- Maximum loan capped at $35,000

OneMain Financial — Best for Same-Day Funding

OneMain Financial operates over 1,400 physical branch locations across the United States, which differentiates it significantly from purely digital lenders. This physical footprint allows for in-person verification that speeds up the approval process — and in many cases allows funds to be disbursed the same day an application is completed.

✓ Pros

- No stated minimum credit score

- Same-day funding at branches

- Secured and unsecured options

- 1,400+ physical locations nationwide

- Option to change payment due date

✗ Cons

- Higher starting APR (18%)

- Origination fee varies by state

- Maximum loan of $20,000 is lower

- APR caps at 35.99% for all borrowers

For emergency borrowers who need cash today: Same-Day Personal Loans — Full Emergency Guide 2026

APR Deep Dive — What Bad Credit Borrowers Actually Pay

The single most important number in any personal loan is the Annual Percentage Rate (APR) — because it reflects the total annual cost of the loan, including interest and most fees. For bad credit borrowers, understanding how lenders determine your specific rate is crucial to minimizing borrowing costs.

What Drives APR for Bad Credit Loans

Every lender on our list uses a risk-based pricing model, meaning your individual rate within the published APR range depends on a specific set of factors:

| Factor | Impact on APR | What You Can Do |

|---|---|---|

| Credit Score | Highest single factor — 10+ percentage points difference between 500 and 650 | Check and dispute errors on your free credit report |

| Debt-to-Income Ratio | High DTI increases rate 2–6% | Pay down small balances before applying |

| Employment Stability | 2+ years at same employer lowers rate 1–3% | Document employment history thoroughly |

| Loan Term | Longer terms = higher total interest (not necessarily higher APR) | Borrow the shortest term you can afford |

| Loan Amount | Mid-range amounts ($5K–$15K) often get better rates than very small loans | Borrow only what you need |

| Collateral | Secured loans can reduce APR by 5–15 percentage points | Consider secured loan if you own a vehicle |

Real-World APR Scenarios for Bad Credit Borrowers

| Credit Score | Income | Typical APR Range | Monthly Payment ($10K, 36mo) | Total Interest Paid |

|---|---|---|---|---|

| 500–549 | $35,000/yr | 28% – 35.99% | $409 – $435 | $4,724 – $5,660 |

| 550–599 | $45,000/yr | 19% – 28% | $367 – $409 | $3,212 – $4,724 |

| 600–649 | $55,000/yr | 12% – 22% | $332 – $379 | $1,952 – $3,644 |

| 650–669 | $65,000/yr | 8% – 16% | $313 – $352 | $1,268 – $2,672 |

These scenarios illustrate why improving your credit score even slightly before applying can save hundreds or thousands of dollars. A borrower moving from a 549 to a 600 score could save over $2,700 in total interest on a $10,000 36-month loan.

See our credit building guide: How to Rebuild Credit Fast — 2026 Guide

Best Loans for 500–600 Credit Scores

Borrowers in the 500–600 credit score range — classified as « very poor » to « fair » by FICO’s scoring model — face the most limited options but are not without recourse. Here are the most realistic options available in 2026:

| Lender | Approves 500–600? | Key Factor Besides Score | Best Feature |

|---|---|---|---|

| Upstart | Yes — min 300 | Education + employment history | Lowest starting APR at this tier |

| OneMain Financial | Yes — no minimum | Income and collateral | Same-day funding at branches |

| OppLoans | Yes — income focus | Monthly income and bank history | Easiest approval, but very high APR |

| Avant | Borderline — min 550 | Income and DTI ratio | Better mobile experience |

| Federal Credit Union | Often yes — varies | Member relationship and income | APR capped at 18% by federal law |

Pro Tip — Federal Credit Unions: Under federal law, federal credit unions cannot charge an APR above 18% on personal loans. If you qualify for membership (many are open to anyone), this cap makes credit unions one of the best resources for borrowers with scores in the 500–600 range. The NCUA credit union locator helps you find eligible institutions near you.

Secured vs. Unsecured Personal Loans for Bad Credit

One of the most underutilized strategies for bad credit borrowers is the secured personal loan — a loan backed by collateral that dramatically changes the risk equation for lenders and, consequently, the rates and approval odds available to borrowers.

Secured Loan

LowerAPR. Collateral (vehicle, savings account, CD) reduces lender risk, enabling lower rates. OneMain Financial borrowers using vehicle collateral often see APRs 5–10% lower than equivalent unsecured offers.

Unsecured Loan

HigherAPR. No collateral means the lender bears all risk if you default, which translates directly into higher interest rates — often 5–15 percentage points above equivalent secured offers for the same borrower profile.

Common Collateral Types for Secured Personal Loans

- Vehicle title loans: Your paid-off car or motorcycle serves as collateral. OneMain Financial and several credit unions accept this. Risk: you lose your vehicle if you default.

- Savings-secured loans: Your savings account balance acts as collateral. Approval is near-guaranteed and rates are very low — typically 1–3% above the savings account APY. Available at most credit unions and some banks.

- Certificate of deposit (CD) loans: Similar to savings-secured loans, your CD serves as collateral. Low rates, near-certain approval.

- Investment accounts: Some lenders allow brokerage accounts as collateral. Less common for personal loans.

See our full breakdown: Secured vs. Unsecured Loans — Which Is Right for You?

Fast Approval Online Lenders for Emergencies

When financial emergencies arise — unexpected medical bills, urgent car repairs, or gap coverage between paychecks — funding speed becomes the primary concern. These lenders have the fastest verified disbursement timelines for bad credit borrowers in 2026:

To maximize funding speed at any lender, prepare the following documents before you begin your application:

- Government-issued photo ID (driver’s license or passport)

- Social Security Number

- Two most recent pay stubs or bank statements showing income

- Banking routing and account number for direct deposit

- Proof of address (utility bill, bank statement dated within 90 days)

- Employment verification letter if recently started a new job

How to Improve Your Approval Chances in 2026

Even if your credit score is in poor territory, several strategies can meaningfully improve your approval odds and reduce the APR you’re offered:

1. Add a Co-Signer with Good Credit

A co-signer with a credit score above 700 essentially lends you their creditworthiness. Most major personal loan lenders — including Upgrade, LendingPoint, and many credit unions — accept co-signers. The co-signer becomes equally responsible for the debt if you miss payments, so this strategy requires significant trust between both parties.

Co-signer impact data: According to Experian research, borrowers who add a co-signer with a 720+ credit score see their offered APR drop by an average of 6.8 percentage points. On a $10,000 loan over 36 months, that difference amounts to $1,228 in total interest savings.

2. Reduce Your Debt-to-Income Ratio First

Most lenders target a DTI (monthly debt payments ÷ gross monthly income) below 43% for approval. If your DTI is above this threshold, paying off a small credit card or personal line of credit before applying can push you into approvable territory. Even eliminating a $200/month payment can swing your DTI by 2–5 points.

3. Dispute Credit Report Errors

Research by the Federal Trade Commission found that 1 in 5 American consumers has a material error on at least one of their three credit reports. Errors such as incorrectly reported late payments, duplicate accounts, or identity theft-related accounts can suppress your score by 20–100+ points. Correcting them is free and can be done at AnnualCreditReport.com.

4. Apply to Multiple Lenders Within a Short Window

When shopping for personal loans, multiple applications within a 14–45 day window are typically treated as a single hard inquiry for credit scoring purposes — depending on your scoring model. This allows you to comparison shop aggressively without suffering multiple credit score drops.

5. Consider a Credit Builder Loan First

If your credit is too low for any reasonable-rate personal loan, a credit builder loan from a credit union can help you build a 6–12 month positive payment history that raises your score enough to qualify for better products. Self Inc. and many credit unions offer these specifically for credit rebuilding.

What to Avoid — High-Risk Lending Products

When traditional personal loans are hard to access, borrowers with bad credit are often targeted by predatory lending products. Understanding which products to avoid is as important as knowing which lenders to trust:

Warning — Products to Avoid:

- Payday loans: APRs typically range from 300% to 664%. The CFPB consistently identifies these as high-risk debt traps for low-income borrowers

- Rent-to-own financing: Effective APRs can exceed 200% for electronics or furniture

- Buy Now Pay Later (BNPL) installment plans for cash: Late fees compound quickly

- Title loan companies (not OneMain): Average APR of 300%; risk losing your vehicle

- Advance fee loan scams: Legitimate lenders never require upfront payment to receive funds

Frequently Asked Questions

Conclusion — Best Bad Credit Loan Strategy for 2026

The bad credit personal loan market in 2026 is more sophisticated and accessible than at any previous point — but the difference between a manageable loan and a damaging debt trap still comes down to the APR. Borrowers who take time to prequalify at multiple lenders, understand their true total repayment cost, and explore secured or co-signer options where possible consistently secure significantly better deals.

| Your Situation | Best Lender | Why |

|---|---|---|

| Score below 580, need best rate possible | Upstart | AI model looks beyond score; lowest starting APR |

| Score 550–650, stable income | Avant or LendingPoint | Competitive mid-range APRs for fair credit |

| Emergency — need funds today | OneMain Financial | Same-day branch funding, no minimum score |

| Own a vehicle, want lowest APR | OneMain (secured) | Collateral reduces APR significantly |

| Have a co-signer with good credit | Upgrade or LendingPoint | Co-signer programs available; rates drop sharply |

| Credit union member | Your credit union | Federal law caps APR at 18%; best possible rate |

Whatever your situation, the most important action is to prequalify at 3–5 lenders before accepting any offer. The soft credit checks cost nothing, take minutes, and the potential savings are substantial. On a $10,000 loan, the difference between a 28% and an 18% APR over 36 months is more than $1,800 in total interest paid.

Ready to compare your options? Start with Upstart’s prequalification tool — it takes under 5 minutes, won’t affect your credit, and gives you a real rate offer based on your full financial profile. Then compare against Avant and LendingPoint before making a final decision.

Ahmada Ndao is a financial research analyst and independent journalist

specializing in US consumer finance, legal rights, and insurance markets.

With over 5 years covering American financial products, he has helped

thousands of readers navigate complex insurance decisions, find the right

legal representation, and optimize their credit strategies. His research

methodology combines primary data analysis, direct outreach to industry

professionals, and continuous monitoring of federal regulatory changes.

Ahmada’s work has been cited by financial communities across the US and

reviewed by licensed attorneys and insurance professionals for accuracy.