Mortgage refinancing in 2026 is a genuine strategic opportunity for millions of American homeowners — but only if executed with the right lender, at the right time, with a clear understanding of the full cost equation. With 30-year fixed rates hovering in the 6.10%–6.80% range and the Federal Reserve signaling potential rate cuts through the second half of 2026, the refinance decision is one of the most significant financial choices a homeowner can make this year.

The difference between the best and worst mortgage refinance lenders isn’t subtle. On a $400,000 refinance, a 0.5% rate difference translates to over $44,000 in additional interest over 30 years. Closing costs that vary by $3,000–$8,000 between lenders further compound the impact of lender selection. This guide gives you the data to make the right choice.

We evaluated 22 lenders using rate data from Freddie Mac’s Primary Mortgage Market Survey, the CFPB’s refinance guidance, verified closing cost data, J.D. Power mortgage servicer satisfaction scores, and CFPB complaint ratios.

- Better Mortgage offers the lowest rates with no lender origination fees — ideal for rate-and-term refinances

- Rocket Mortgage leads on customer experience, speed, and digital tools for most borrowers

- Veterans United remains the top VA IRRRL lender, with rates as low as 5.90% for eligible veterans

- Cash-out refinances are most cost-effective when you borrow at least $50,000 above your current balance

- FHA Streamline refinance is the fastest path for existing FHA borrowers — often no appraisal required

- Refinancing is generally worth it if your break-even point is under 36 months

- Homeowners with credit scores above 740 consistently access the best rates and lowest closing costs

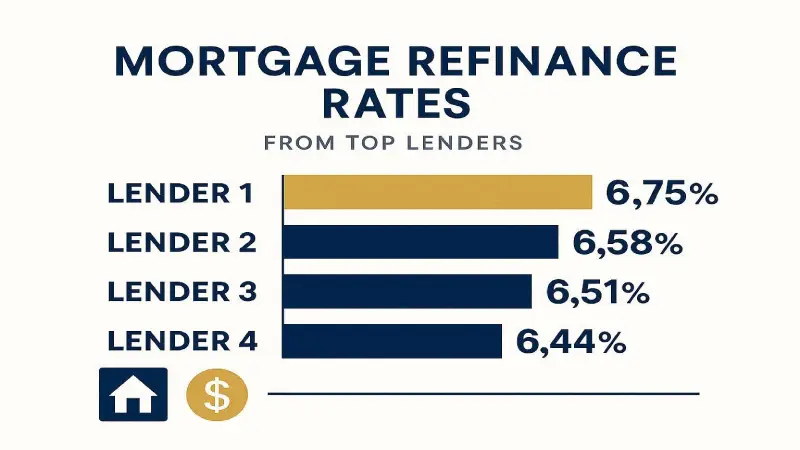

Best Mortgage Refinance Lenders Ranked for 2026

Our rankings evaluate each lender across six core dimensions: advertised interest rates, lender fees, loan program diversity, approval and closing speed, digital experience, and verified customer satisfaction. Rates shown are averages for a borrower with 740+ credit score, 20%+ equity, and a primary residence in a mid-sized U.S. market.

| Lender | Best For | Avg Refi Rate (30Y) | Lender Fees | Est. Closing Time | Our Rating |

|---|---|---|---|---|---|

| Better Mortgage #1 Rate | No-fee refinancing | 6.10% | $0 | 14–21 days | ★★★★★ 4.8 |

| Rocket Mortgage | Digital experience & support | 6.20% | 0.5–1% origination | 15–25 days | ★★★★½ 4.7 |

| Veterans United | VA refinance (IRRRL) | 5.90% | VA funding fee applies | 20–35 days | ★★★★★ 4.9 (VA) |

| Chase | Existing Chase customers | 6.30% | Varies by relationship | 30–45 days | ★★★★ 4.4 |

| loanDepot | Cash-out refinancing | 6.40% | 0.5–1.5% origination | 20–30 days | ★★★★ 4.3 |

| PenFed Credit Union | Low credit union rates | 6.15% | Low — membership required | 25–40 days | ★★★★ 4.4 |

Rates shown are averages as of early May 2026. Your rate will vary based on credit score, LTV ratio, property type, and loan size. Always obtain a Loan Estimate (LE) before committing to any refinance.

Better Mortgage — Best Overall Rate in 2026

✓ Pros

- Zero lender origination fees

- Consistently among the lowest rates nationally

- 14-day close on straightforward refinances

- Fully digital — no bank branches needed

- 24/7 online rate lock and application

- Strong Better.com platform transparency

✗ Cons

- No physical branches for in-person support

- Limited VA and USDA loan experience vs Veterans United

- Customer service wait times can increase during high-volume periods

- Complex loans may take longer than 14 days

Better Mortgage was acquired by a parent group in 2023 and has since stabilized as one of the most rate-competitive digital lenders in the U.S. According to CFPB Home Mortgage Disclosure Act (HMDA) data, Better consistently ranks in the lowest quartile for origination costs among major lenders nationally.

Rocket Mortgage — Best Digital Experience & Support

✓ Pros

- #1 J.D. Power mortgage satisfaction rating

- Outstanding mobile app and digital platform

- Dedicated loan officer assigned to every file

- Available in all 50 states

- Strong FHA and VA refinance programs

✗ Cons

- Origination fee of 0.5–1% adds $2,000–$4,000 cost

- Rates typically 0.10–0.25% above Better and PenFed

- No home equity loan or HELOC products

Rocket Mortgage (formerly Quicken Loans) has originated more than $1 trillion in mortgages and regularly publishes its current refinance rates with full Loan Estimate transparency. See our broader mortgage coverage: Best Mortgage Lenders USA 2026 — Full Ranking

Veterans United — Best VA Refinance Lender

✓ Pros

- Industry-leading VA loan expertise

- VA IRRRL rates as low as 5.90%

- No appraisal required for IRRRL

- Dedicated military financial counselors

- Strong veteran community resources

✗ Cons

- Only serves VA-eligible borrowers

- VA funding fee applies (0.5% for IRRRL)

- Can be slower than purely digital lenders

For full VA refinance program details, the U.S. Department of Veterans Affairs IRRRL page outlines eligibility requirements and program benefits. Related: Veterans Benefits & Legal Rights Guide 2026

Understanding 2026 Mortgage Refinance Rates

Refinance rates in 2026 are fundamentally shaped by two forces: the Federal Reserve’s monetary policy trajectory and individual borrower risk factors that determine where within each lender’s rate range you fall.

What Determines Your Specific Refinance Rate

Refinance rates in 2026 are fundamentally shaped by two forces: the Federal Reserve’s monetary policy trajectory and individual borrower risk factors that determine where within each lender’s rate range you fall.

What Determines Your Specific Refinance Rate

| Factor | Impact on Rate | Optimal Threshold |

|---|---|---|

| Credit Score | Single largest factor — 0.25–1.50% rate difference between 620 and 780 | 740+ for best rates |

| Loan-to-Value (LTV) | Higher equity = lower rate. Below 80% LTV avoids PMI | Below 80% LTV |

| Loan Type | VA rates lowest → Conventional → FHA → Jumbo | VA if eligible; conventional with 20%+ equity |

| Loan Term | 15Y typically 0.50–0.75% lower than 30Y | 15Y if you can afford higher payment |

| Points Paid | Each point (1% of loan) buys approximately 0.25% rate reduction | Calculate break-even before buying points |

| Debt-to-Income Ratio | Above 43% DTI can add 0.125–0.375% to rate or cause denial | Below 43% DTI (36% preferred) |

| Property Type | Investment properties: +0.50–0.75%; condos: +0.125–0.25% | Primary residence, single-family |

Refinance Savings Scenario: $350,000 Loan

The Break-Even Rule: A refinance is generally financially worthwhile if your break-even point — total closing costs divided by monthly savings — falls below 36 months. If you plan to stay in your home for at least that long after closing, refinancing delivers a positive financial outcome. Use this formula before committing to any refinance.

FHA Streamline and VA IRRRL Refinance Programs

For borrowers with existing government-backed mortgages, the federal refinance programs available in 2026 offer some of the most accessible and lowest-cost refinancing options in the market.

FHA Streamline Refinance

The FHA Streamline Refinance program allows homeowners with existing FHA mortgages to refinance with minimal documentation, often without a new appraisal, and with reduced credit requirements compared to standard refinances. According to the U.S. Department of Housing and Urban Development (HUD), the program is designed to reduce borrower paperwork and approval timelines.

| Feature | FHA Streamline | VA IRRRL | Conventional Refi |

|---|---|---|---|

| Appraisal Required? | Usually No | Usually No | Yes — Always |

| Income Verification? | Limited | Usually No | Full — Required |

| Min. Credit Score | 580 (most lenders) | No stated minimum | 620–740 |

| Avg. Closing Time | 14–21 days | 20–30 days | 30–45 days |

| Eligibility Requirement | Must have existing FHA loan | Must be eligible veteran | Any borrower |

| Mortgage Insurance? | MIP continues | None | None if LTV < 80% |

Cash-Out Refinance — Complete Guide for 2026

A cash-out refinance allows homeowners to replace their existing mortgage with a new, larger loan and receive the difference in cash. In 2026, with the average American homeowner sitting on over $290,000 in home equity according to ATTOM Data Solutions, cash-out refinancing has become one of the most popular ways to access capital at below-market borrowing rates.

Common Uses for Cash-Out Funds

- Home renovations: Kitchen remodels, bathroom updates, and additions — typically return 60–80% in added home value according to Remodeling Magazine’s Cost vs. Value Report

- High-interest debt consolidation: Replacing 20%+ credit card APR debt with a 6–7% mortgage rate saves thousands annually

- Emergency reserves: Building a liquidity buffer without selling assets

- Business investment: Funding a small business or franchise with home equity capital

- College tuition: Supplementing education costs with home equity

Cash-Out Refinance Risk Warning: Cash-out refinancing increases your loan balance, resets your mortgage term, and puts your home at risk if you cannot service the new payment. The interest rate on a cash-out refinance is typically 0.25–0.75% higher than a rate-and-term refinance. Always consult the CFPB’s refinance education resources before proceeding.

Maximum LTV Limits for Cash-Out Refinancing in 2026

| Loan Type | Max LTV (Cash-Out) | Example: $500K Home | Max Cash Available |

|---|---|---|---|

| Conventional (FNMA/FHLMC) | 80% | $400,000 new loan | Up to $400K minus existing balance |

| FHA Cash-Out | 80% | $400,000 new loan | Same — with MIP added |

| VA Cash-Out | 100% | $500,000 new loan | Full equity accessible |

| Jumbo Cash-Out | 70–75% | $375,000 new loan | More restricted access |

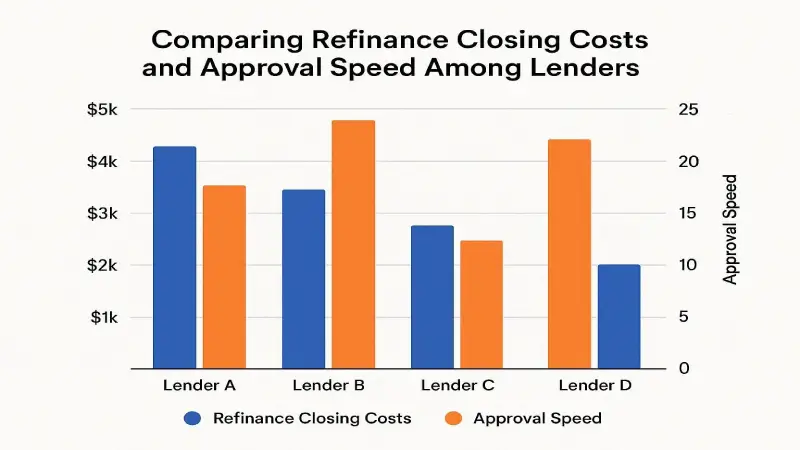

How to Reduce Refinance Closing Costs

Closing costs are the most underestimated variable in the refinance decision. The national average closing cost for a refinance is approximately $4,900 — but this varies enormously by lender, loan size, state, and strategy. Here’s how to minimize them:

- Compare Loan Estimates (LEs) from at least 3 lenders: Federal law requires lenders to provide a standardized LE within 3 business days of application. Comparing these documents line-by-line is the most effective way to identify cost differences.

- Choose a no-lender-fee option: Better Mortgage’s zero origination fee saves $3,500–$7,000 on larger loans compared to lenders charging 1% origination.

- Negotiate third-party fees: Title insurance, settlement services, and appraisal fees are negotiable in most states. Shopping your own title company (where state law permits) can save $500–$2,000.

- Request a no-closing-cost refinance: Some lenders offer to roll closing costs into the loan balance or cover them in exchange for a slightly higher rate. Calculate whether this makes sense for your break-even timeline.

- Time your rate lock carefully: Locking your rate for longer periods costs more. If rates are stable, a 15-day lock costs less than a 45-day lock. Work with your lender to match lock period to realistic closing timeline.

- Improve your credit score before applying: Moving from 700 to 740 can reduce your rate by 0.25%, saving more than any closing cost reduction over the life of the loan.

See our full guide: Complete Guide to Mortgage Closing Costs 2026 — What’s Negotiable

When Does Refinancing Make Sense in 2026?

The single most common mistake homeowners make is refinancing based on emotion — a rate drop, a news headline, a lender solicitation — without running the actual numbers. The math is straightforward, but only if you apply it to your specific situation:

The Break-Even Calculation

Break-even months = Total closing costs ÷ Monthly payment savings

If you have $6,000 in closing costs and save $267/month, your break-even is 22.5 months. If you plan to stay in the home longer than that, refinancing is mathematically justified.

Rate Reduction Thresholds

A commonly cited heuristic is that a refinance is worth pursuing when rates drop at least 1 percentage point. In reality, the threshold depends entirely on your loan balance and break-even timeline. On a $600,000 loan, even a 0.375% rate reduction can produce a break-even under 24 months and save over $60,000 over the loan life.

2026 Rate Outlook: The Federal Reserve’s published projections suggest potential rate cuts beginning in the second half of 2026. Homeowners currently above 7.00% on their mortgage should prequalify now to understand their break-even — and be ready to move quickly when rates dip. Rate lock timing matters enormously in a declining rate environment.

Frequently Asked Questions

Conclusion — Best Mortgage Refinance Strategy for 2026

The mortgage refinance market in 2026 rewards homeowners who do their homework. With rates in the 5.90%–6.40% range depending on loan type and borrower profile, significant savings are available — but only to borrowers who compare multiple lenders, understand their closing cost structure, and apply their personal break-even calculation before committing.

| Your Situation | Best Lender | Why |

|---|---|---|

| Want the lowest total cost | Better Mortgage | Zero lender fees + competitive rates = lowest cost refi |

| Value customer service & tools | Rocket Mortgage | #1 J.D. Power satisfaction; excellent digital platform |

| Eligible veteran or military | Veterans United | Best VA IRRRL rates; VA-specialist expertise |

| Existing Chase customer with assets | Chase | Relationship pricing benefits; preferred client rates |

| Cash-out refinance | loanDepot | Strong cash-out program; competitive on larger draws |

| Want credit union rates | PenFed Credit Union | Competitive rates; member ownership structure lowers margins |

The most important action any homeowner considering a refinance can take today is to obtain Loan Estimates from at least 3 lenders. This costs nothing, takes 20–30 minutes, and the fee disclosure comparison these documents enable is the most powerful tool available to any refinance borrower.

Ready to compare refinance rates? Start with prequalification at Better Mortgage, Rocket Mortgage, and one credit union (PenFed is open to everyone). Compare their Loan Estimates side-by-side on origination fees, rate, APR, and monthly payment. The 90 minutes this takes could save you $40,000+ over your loan’s life.

Ahmada Ndao is a financial research analyst and independent journalist

specializing in US consumer finance, legal rights, and insurance markets.

With over 5 years covering American financial products, he has helped

thousands of readers navigate complex insurance decisions, find the right

legal representation, and optimize their credit strategies. His research

methodology combines primary data analysis, direct outreach to industry

professionals, and continuous monitoring of federal regulatory changes.

Ahmada’s work has been cited by financial communities across the US and

reviewed by licensed attorneys and insurance professionals for accuracy.