My Employer Just Paused Their 401(k) Match — What to Do Now (And How Much It Really Costs You)

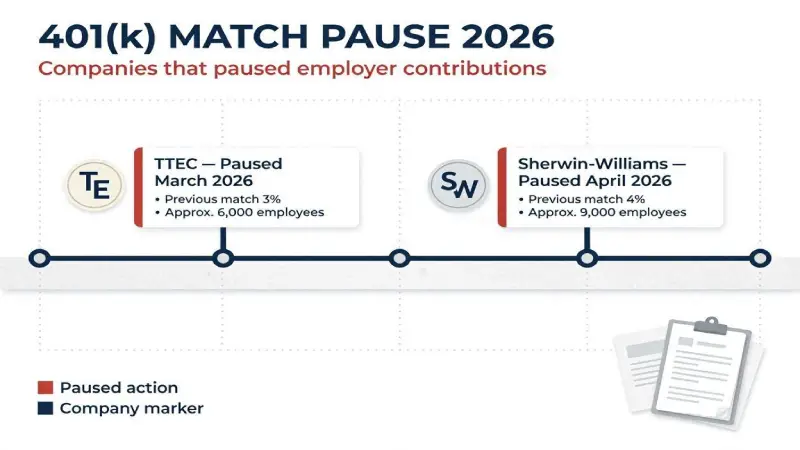

TTEC just paused its 401(k) match for 16,000 US employees. Sherwin-Williams, Drexel University, and others did it before them — and according to Fortune, economists warn this is just the beginning. The last time employer 401(k) pauses happened at this scale was during the 2008 recession and early COVID-19 pandemic. If your employer just announced a match suspension, you need to act immediately — not to panic, but to replace the lost contribution with smarter alternatives. This guide explains exactly what a paused match costs you in real dollars, whether to keep contributing anyway, and the six moves that protect your retirement when your employer stops pulling their weight.

🏢 Which Companies Have Already Paused Their 401(k) Match in 2026

| Company | Action | Details | Status |

|---|---|---|---|

| TTEC | Paused 3% match | 16,000 US employees affected; Q2 2026 through end of 2026; review early 2027 | 🔴 Currently paused |

| Sherwin-Williams | Temporary pause | Paused October 2025; resumed February 2026 with makeup contribution | ✅ Restored |

| Drexel University | Temporary pause | Paused and restored within the year | ✅ Restored |

| IBM | Structural change | Moved from traditional match to Retirement Benefit Account (RBA) defined-benefit plan | ⚠️ Changed permanently |

| Deloitte / Zoom | Benefits reduction | Broader benefits package reductions in 2026 | ⚠️ Ongoing |

According to HR Brew, employers are increasingly pausing 401(k) matches as an alternative to layoffs during economic strain — a trend last seen during the 2008 recession and early COVID-19 pandemic. The Street noted that what distinguishes the TTEC case is the candor: most companies cutting benefits in this cycle have used language about "streamlining" or "prioritizing long-term growth." TTEC named the trade-off explicitly: the 401(k) match is being suspended to fund AI. This transparency makes it a cleaner case study for a dynamic almost certainly playing out less visibly at many more employers.

💰 How Much Does a Paused 401(k) Match Actually Cost You?

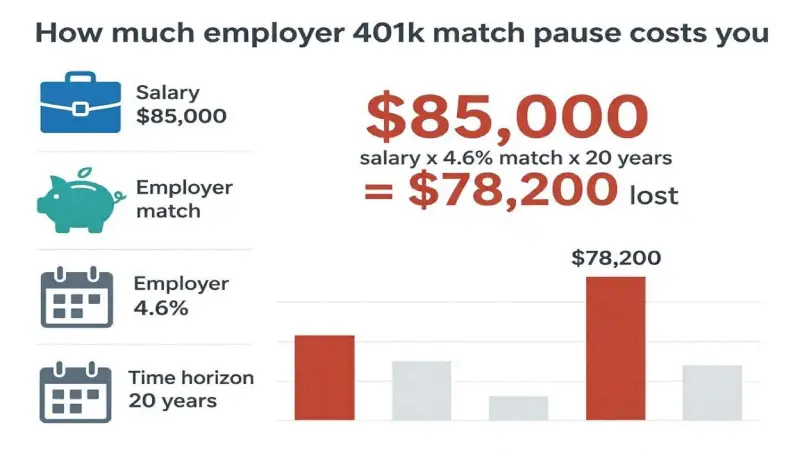

According to AOL Finance, if you earn $85,000 per year and your employer offers a 4.6% match of $3,910, your employer would contribute a total of $78,200 across 20 years — not accounting for raises or investment growth. With compound investment returns at historical market averages, that $78,200 in employer contributions could grow to $200,000+ by retirement.

| Your Salary | Match Rate | Annual Match Lost | Over 5 Years | Over 20 Years | At Retirement (with growth) |

|---|---|---|---|---|---|

| $50,000 | 3% | $1,500/yr | $7,500 | $30,000 | ~$80,000 est. |

| $75,000 | 3% | $2,250/yr | $11,250 | $45,000 | ~$120,000 est. |

| $85,000 | 4.6% | $3,910/yr | $19,550 | $78,200 | ~$210,000 est. |

| $100,000 | 4% | $4,000/yr | $20,000 | $80,000 | ~$215,000 est. |

| $120,000 | 6% | $7,200/yr | $36,000 | $144,000 | ~$385,000 est. |

*Retirement estimates assume 7% average annual growth from the date of each missed contribution. Actual returns vary. Use a retirement calculator for personalized projections.

🤔 Should You Still Contribute to Your 401(k) Without a Match?

The 401(k) match is often called "free money" — and it's the reason most financial advisors recommend contributing at least enough to capture the full match before doing anything else with your savings. When the match disappears, the calculus changes — but stopping contributions entirely is almost never the right answer.

When You Should Absolutely Keep Contributing

Continue contributing to your 401(k) without a match if: you're in a high tax bracket (the pre-tax contribution still reduces your taxable income significantly); you don't have high-interest debt (above 7%); your emergency fund is solid (3-6 months of expenses); or your plan has strong low-cost index fund options. The tax deferral benefit alone — especially if you're in the 22%, 24%, or 32% bracket — often justifies continued 401(k) contributions even without a match. As Kiplinger explains, employer 401(k) matches have long been a core part of workplace compensation — and their removal raises key questions about taxes and savings strategy.

When You Might Reduce Your 401(k) Contribution

Consider temporarily reducing (not stopping) your 401(k) contribution to the IRS minimum needed for tax benefits if: you have credit card debt above 15% APR; your emergency fund has less than 1 month of expenses; or your 401(k) plan charges high fees and has no good index fund options. In those cases, redirect the difference to a Roth IRA or high-yield savings account — not to spending.

📊 Tax Impact — What Changes When the Match Disappears

Kiplinger's analysis identifies an often-overlooked tax dimension: employer 401(k) contributions are not visible on your paycheck, but they reduce the total taxable compensation you're deferring. When they disappear:

| Scenario | Before Match Pause | After Match Pause | Tax Impact |

|---|---|---|---|

| Your contribution (6%) | Pre-tax, reduces W-2 | Same — no change | No change |

| Employer match (3%) | Added to account, not taxed yet | Gone — not deposited | Less total retirement savings |

| Total retirement savings | 9% of salary | 6% of salary | Retirement gap created |

| Your taxable income | Salary minus your 6% contribution | Same — employer contribution wasn't pre-tax to you anyway | No direct change to your W-2 |

The key tax insight: The employer match was never deducted from your taxable income — it was a separate employer expense. So your W-2 doesn't change when the match pauses. However, your total retirement savings rate drops significantly. The tax-efficient response: increase your own 401(k) contribution to maintain your savings rate — every additional dollar you contribute pre-tax still reduces your W-2 income and your tax bill. The 2026 401(k) contribution limit is $23,500 ($31,000 if age 50+). See the IRS contribution limits page for current figures.

🎯 6 Moves to Protect Your Retirement When the Match Disappears

Move 1 — Max Your Roth IRA First ($7,500 limit for 2026)

Without a match, the Roth IRA immediately becomes the most attractive retirement vehicle for most workers. Unlike a 401(k), a Roth IRA grows completely tax-free — you contribute after-tax dollars, and all growth and qualified withdrawals are tax-free in retirement. The 2026 Roth IRA contribution limit is $7,000 ($8,000 if 50+). Income limits apply: phase-out begins at $150,000 for single filers and $236,000 for married filing jointly. Open a Roth IRA at Fidelity, Vanguard, or Schwab — all offer zero-commission index funds and no account fees.

Move 2 — Use Your HSA as a Stealth Retirement Account

If you have a High-Deductible Health Plan (HDHP), your Health Savings Account is the most tax-advantaged account available — triple tax advantaged (contributions pre-tax, growth tax-free, withdrawals tax-free for medical expenses). After age 65, HSA funds can be withdrawn for any purpose like a traditional IRA. The 2026 HSA contribution limit is $4,300 (individual) or $8,550 (family). Contribute the maximum and invest it in index funds rather than leaving it in cash. See our guide on best savings strategies for 2026.

Move 3 — Increase Your Own 401(k) Contribution to Compensate

If your employer was matching 3% and you were contributing 6%, your total savings rate was 9%. To maintain that rate, increase your contribution to 9%. This preserves the tax deferral benefit while replacing the lost employer contribution with your own. The IRS allows up to $23,500 in employee 401(k) contributions in 2026 ($31,000 if 50+). Most workers are far below this limit and have room to increase.

Move 4 — Open a Taxable Brokerage Account for Flexibility

Once your Roth IRA is maxed, a taxable brokerage account at Fidelity, Schwab, or Robinhood offers no contribution limits, full investment flexibility, and liquidity. Returns are taxable but long-term capital gains rates (0%, 15%, or 20%) are typically lower than ordinary income rates. For workers who may need flexibility before retirement age, a brokerage account complements tax-advantaged accounts well.

Move 5 — Redirect Saved Employer Match to Trump Accounts (If Eligible)

If you have a child born 2025-2028, the new Trump Account allows up to $5,000/year in contributions with employer contributions of up to $2,500/year — tax-free to the employee. Redirecting some of your lost 401(k) match into a Trump Account for your child is a creative alternative that maintains employer-contributed tax-advantaged savings in a different vehicle.

Move 6 — Ask Your Employer About the Restoration Timeline

Fortune's analysis found that most companies that pause matches restore them: Sherwin-Williams and Drexel University both resumed their matches within the year. Ask your HR department directly: What are the conditions for restoring the match? Is there a makeup contribution planned? Is there a specific financial metric that triggers restoration? The answers tell you how to plan. Sherwin-Williams made a makeup contribution when it restored the match — employees who stayed received retroactive compensation.

🔄 Will Your Employer Restore the Match — Historical Data

| Historical Period | % of Companies That Paused Matches | % That Restored Within 12 Months |

|---|---|---|

| 2001 recession | ~16% of large employers | ~72% restored within 18 months |

| 2008–2009 recession | ~19% of large employers | ~68% restored within 2 years |

| COVID-19 (2020) | ~25% of S&P 500 companies | ~82% restored by end of 2021 |

| 2026 (current) | Growing trend | Too early to measure — Sherwin-Williams restored within 4 months |

Historical data is encouraging: the vast majority of employers who pause 401(k) matches eventually restore them. The risk is the minority who don't — and the opportunity cost of the gap period. Craig Copeland of the Employee Benefits Research Institute told AOL Finance that employers favor match pauses over layoffs precisely because they're reversible — suggesting most current pauses are intended to be temporary.

💼 Should You Negotiate or Change Jobs?

The loss of a 401(k) match is a real compensation reduction — quantifiable and significant. That makes it a legitimate basis for salary negotiation or job search evaluation.

Negotiating a Salary Increase to Compensate

If your employer paused a 3% match on a $85,000 salary, they've effectively cut your total compensation by $2,550/year. That's a concrete number to bring to your manager in a salary review conversation: "My total compensation has effectively decreased by $2,550 due to the match suspension — I'd like to discuss adjusting my base salary to reflect this." Not all employers will agree, but the math is objective and the ask is reasonable.

Using the Match Pause as a Job Search Signal

A 401(k) match pause is a genuine financial distress signal. TTEC's Q1 2026 revenue declined 7% year-over-year — that context matters. Before deciding whether to stay, review your company's financial health: revenue trend, profitability, debt levels, and sector outlook. A pause at a company with strong fundamentals and a clear restoration plan is very different from a pause at a company with declining revenue and no clear timeline. Check our financial guides for managing personal finances through employer uncertainty.

❓ Frequently Asked Questions — Employer Paused 401(k) Match 2026

Should I still contribute to my 401(k) if my employer paused the match?

Yes, in most cases. Even without an employer match, 401(k) contributions reduce your taxable income dollar-for-dollar — a significant benefit if you're in the 22% or higher tax bracket. The main exception: if you have high-interest debt (above 7-8% APR), consider paying that down before maximizing your 401(k) without a match. For most workers, the order should be: (1) contribute enough to 401(k) to capture any remaining partial match, (2) max Roth IRA ($7,000 in 2026), (3) max HSA if eligible, (4) return to 401(k) up to the $23,500 limit.

What is the 401(k) contribution limit for 2026?

The IRS 2026 401(k) employee contribution limit is $23,500 — up from $23,000 in 2025. Workers age 50 and older can contribute an additional $7,500 catch-up contribution, for a total of $31,000. The total combined limit (employee + employer contributions) is $70,000 in 2026. When your employer pauses their match, you have room to increase your own contributions up to the $23,500 employee limit to partially offset the lost employer money.

Can my employer legally pause or eliminate the 401(k) match?

Yes — employer 401(k) matching contributions are generally discretionary, not legally required. Unless your employment contract specifically guarantees a match amount, your employer can reduce or suspend matching contributions with proper notice. Most 401(k) plan documents include language giving the employer the right to change or eliminate matching contributions. The only exception is if the match was promised as part of a binding employment contract — in which case consult an employment attorney.

What happens to my existing 401(k) balance when the match is paused?

Nothing — your existing 401(k) balance is completely unaffected by a match pause. All previously vested employer contributions remain yours. Your own contributions also remain yours immediately (they're always 100% vested). The pause only affects new employer contributions going forward — your accumulated balance continues to grow with the market, and you can continue making your own contributions. A match pause does not affect your existing money in any way.

Is a Roth IRA better than a 401(k) without a match?

For many workers, yes. Without the match, the Roth IRA's tax-free growth advantage often outweighs the 401(k)'s pre-tax contribution benefit — especially for workers who expect to be in a higher tax bracket in retirement. A Roth IRA also has no required minimum distributions, more investment options than most 401(k) plans, and allows penalty-free withdrawal of contributions (not earnings) at any time. The ideal strategy when a match is paused: contribute just enough to your 401(k) for the tax deduction if you're in a high bracket, then max your Roth IRA ($7,000 in 2026) before contributing further to your 401(k).

✅ Final Verdict — What to Do When Your Employer Pauses the Match

A paused 401(k) match is real compensation lost — but it doesn't have to derail your retirement. The immediate playbook: (1) don't stop contributing to your 401(k) — the tax benefit remains; (2) open or max a Roth IRA ($7,000 limit) immediately as the first alternative; (3) use your HSA as a stealth retirement account if you have an HDHP; (4) ask HR directly about the restoration timeline and conditions. The longer-term signal: review your company's financial health. A match pause at a struggling company with declining revenue is a very different situation from a temporary pause at a fundamentally strong employer navigating a rough quarter. Sherwin-Williams restored its match within 4 months and added a makeup contribution. Companies like TTEC have temporarily suspended their match, with hopes to resume it based on business performance. Most do restore. Plan as if they won't — celebrate if they do. For related retirement and savings guides see our Trump Accounts 2026 guide, Best High-Yield Savings Accounts June 2026, and Best Credit Cards USA 2026.

Disclaimer: This article is for informational purposes only and does not constitute financial advice. 401(k) rules and contribution limits are subject to IRS regulation and may change. Consult a qualified financial advisor for personalized retirement planning advice. Updated June 4, 2026.

Ahmada Ndao is a financial research analyst and independent journalist

specializing in US consumer finance, legal rights, and insurance markets.

With over 5 years covering American financial products, he has helped

thousands of readers navigate complex insurance decisions, find the right

legal representation, and optimize their credit strategies. His research

methodology combines primary data analysis, direct outreach to industry

professionals, and continuous monitoring of federal regulatory changes.

Ahmada’s work has been cited by financial communities across the US and

reviewed by licensed attorneys and insurance professionals for accuracy.