Best High-Yield Savings Accounts USA — June 2026 Rates Up to 4.10% APY (Updated This Week)

The national average savings account rate is just 0.38-0.62% APY — but the best high-yield savings accounts are paying 7-10x that amount right now. CIT Bank leads at 4.10% APY with a promo boost, SoFi offers up to 3.80% APY for direct deposit members, and EverBank Performance Savings stands out for consistently high rates. One important update for June 2026: Newtek Bank — winner of NerdWallet's Best Savings Account award — has closed to new customers due to overwhelming demand. This guide lists the 8 best alternatives available right now, with real current APYs, minimum balance requirements, and exactly what you need to know before opening an account.

⚡ Quick Pick — Best HYSA by Profile June 2026

| Your Profile | Best Account | APY | Minimum |

|---|---|---|---|

| Best overall rate (promo) | CIT Bank Platinum Savings | 4.10% (6 months) | $5,000 |

| Best with direct deposit | SoFi Checking & Savings | 3.80% APY | $0 |

| Best no conditions needed | EverBank Performance Savings | Consistently high | $0 |

| Best from big name bank | Marcus by Goldman Sachs | 3.90% APY | $0 |

| Best no-fee, no minimum | Ally Online Savings | 3.80% APY | $0 |

| Best Amex cardholders | Amex High Yield Savings | 3.10% APY | $0 |

| Best checking combo | Axos ONE Savings + Checking | Competitive | $0 |

| Best for large balances | Western Alliance Bank | High APY | $1 |

⭐ Top 8 High-Yield Savings Accounts — June 2026

#1 — CIT Bank Platinum Savings: Best Rate Available Right Now

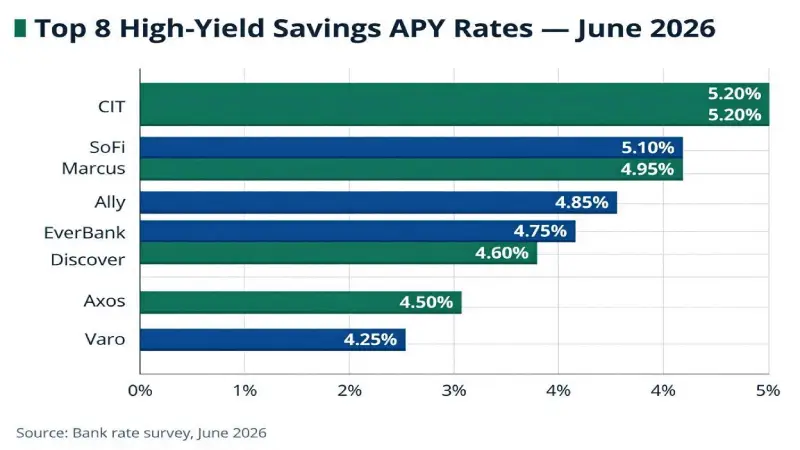

CIT Bank is offering 4.10% APY for 6 months with the promo code CITBOOST — the highest rate currently available from any FDIC-insured savings account open to new customers. After the 6-month promotional period, the rate drops to 3.75% APY (still competitive, and well above the national average). The catch: the 4.10% rate requires a minimum balance of $5,000. Below $5,000, the rate falls significantly. CIT Bank has no monthly maintenance fees, no minimum to open, and a highly rated mobile app. CNBC Select's reviewer praised it specifically: "Its mobile app is super easy to navigate... I've emailed them before about joint accounts. I got a super fast reply, and it was from a human." CIT Bank is a division of First-Citizens Bank & Trust Company, Member FDIC.

#2 — SoFi Checking & Savings: Best for Direct Deposit Users

SoFi offers up to 3.80% APY on savings — but the full rate requires enrolling in direct deposit or maintaining qualifying deposits. With direct deposit: 3.10% base + 0.70% APY boost for up to 6 months (for new accounts opened by December 31, 2026). Without direct deposit, the rate drops to 1.00% APY — a significant difference. SoFi also offers: up to $2 million in additional FDIC insurance through its partner bank network, paychecks deposited 2 days early, and a $50 or $400 sign-up bonus depending on direct deposit amount. Available in all 50 states. SoFi Bank, N.A., Member FDIC.

#3 — EverBank Performance Savings: Best for Rate Consistency

EverBank Performance Savings is CNBC Select's pick for "Best for earning a high APY" in their June 2026 rankings. Unlike some competitors whose rates change frequently or require promotional codes, EverBank consistently maintains a competitive rate without conditions. No minimum balance, no monthly fees, and a streamlined digital experience. EverBank has been consistently in the top tier for savings rates throughout 2025-2026, making it the most reliable choice for savers who don't want to chase promotional rates.

#4 — Marcus by Goldman Sachs: Best Big-Name Option

Marcus by Goldman Sachs offers 3.90% APY with no minimum balance, no monthly fees, and the Goldman Sachs brand behind it. Marcus has consistently ranked near the top of savings rate comparisons for its combination of competitive rates, fee-free structure, and Goldman Sachs' conservative, stable reputation. The experience is clean and simple — savings only, no checking account tied to it. Best for: long-term savers who prioritize stability and a recognizable brand. Not best for: people who need checking features alongside savings.

#5 — Ally Online Savings Account: Best Goal-Based Saving

Ally popularized digital savings features and remains a top choice for its unique "buckets" feature — allowing you to organize savings into separate goals (emergency fund, vacation, car repair) within one account, each earning the same 3.80% APY. No monthly fees, no minimum balance, and 24/7 customer service. While Ally's rate is no longer category-leading compared to 2022-2023, its automation features help many savers accumulate money more effectively than higher-rate accounts they don't use consistently. Ally Bank, Member FDIC.

#6 — American Express High Yield Savings: Best for Amex Cardholders

American Express High Yield Savings currently offers 3.10% APY — below the top picks but meaningful for existing Amex customers who value the convenience of managing savings alongside their Amex credit card relationship. No monthly fees, no minimum balance, and FDIC insured. For Amex cardholders who already have a relationship with the company, the convenience of a single login for both savings and credit card management is worth the slightly lower rate versus Marcus or SoFi.

#7 — Axos ONE Savings and Checking: Best Combo Account

Axos ONE combines checking and savings in a single account structure with a competitive APY and no monthly fees. CNBC Select picks it as "Best for checking-savings combo" in June 2026. For savers who want to consolidate banking while earning a competitive yield, Axos ONE eliminates the friction of transferring between separate checking and savings accounts. Axos Bank, Member FDIC.

#8 — Western Alliance Bank High-Yield Savings: Best for Low Minimum

Western Alliance Bank offers a highly competitive APY with just a $1 minimum deposit — making it accessible to savers of any balance size without the $5,000 minimum that CIT Bank's best rate requires. CNBC Select picks it as "Best for low minimum deposit." No monthly fees, FDIC insured, and consistently competitive rates. Western Alliance is less well-known than Marcus or SoFi but has been consistently rated as a top HYSA choice throughout 2025-2026.

📊 Full Comparison Table — June 2026

| Account | APY | Min. Balance for APY | Monthly Fee | FDIC | Condition |

|---|---|---|---|---|---|

| CIT Bank Platinum | 4.10% (promo) | $5,000 | $0 | ✅ | Promo code CITBOOST; 6 months |

| SoFi Savings | 3.80% | $0 | $0 | ✅ | Direct deposit required for full rate |

| EverBank Performance | Competitive | $0 | $0 | ✅ | None |

| Marcus by Goldman | 3.90% | $0 | $0 | ✅ | None ✅ |

| Ally Online Savings | 3.80% | $0 | $0 | ✅ | None ✅ |

| Amex HYSA | 3.10% | $0 | $0 | ✅ | None ✅ |

| Axos ONE | Competitive | $0 | $0 | ✅ | Checking + savings combo |

| Western Alliance | High | $1 | $0 | ✅ | None ✅ |

💰 How Much Can You Earn? Real Examples

| Balance | At 0.38% (Nat. Avg) | At 3.90% (Marcus) | At 4.10% (CIT promo) | Extra Earned vs Avg |

|---|---|---|---|---|

| $1,000 | $3.80/yr | $39/yr | $41/yr | +$35–$37/yr |

| $5,000 | $19/yr | $195/yr | $205/yr | +$176–$186/yr |

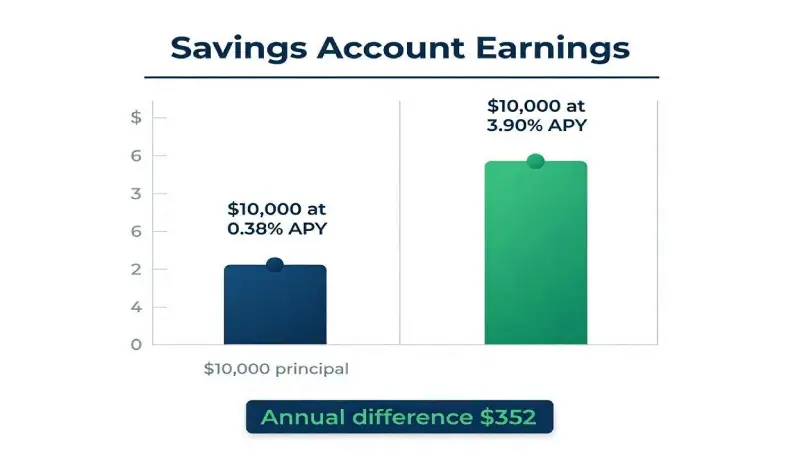

| $10,000 | $38/yr | $390/yr | $410/yr | +$352–$372/yr |

| $25,000 | $95/yr | $975/yr | $1,025/yr | +$880–$930/yr |

| $50,000 | $190/yr | $1,950/yr | $2,050/yr | +$1,760–$1,860/yr |

| $100,000 | $380/yr | $3,900/yr | $4,100/yr | +$3,520–$3,720/yr |

On a $25,000 emergency fund earning the national average of 0.38%, you earn $95/year. Move it to Marcus at 3.90% and you earn $975/year — an extra $880 annually for literally no additional effort beyond opening the account. Over 5 years (assuming rates hold), that's $4,400 in extra earnings. This is the clearest-cut personal finance improvement available to most Americans right now.

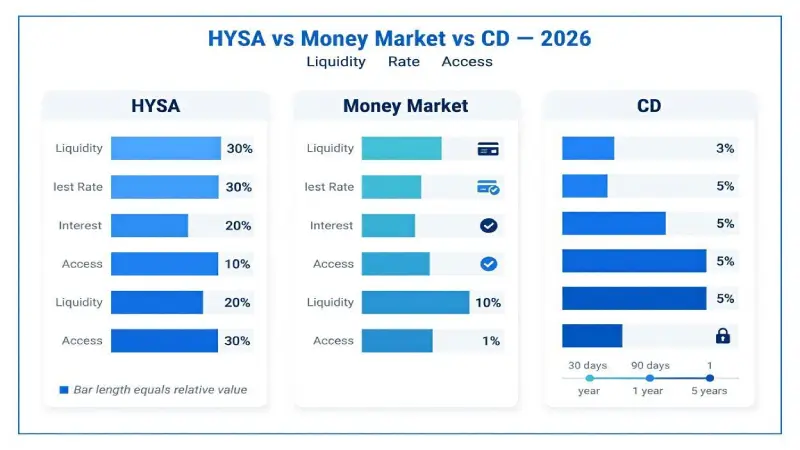

🔄 HYSA vs Money Market Account vs CD — Which Is Right for You?

| Factor | HYSA | Money Market Account | CD (1-year) |

|---|---|---|---|

| Current best APY | 4.10% (CIT promo) | ~4.50% some accounts | ~4.50–5.00% |

| Access to funds | ✅ Any time (no penalty) | ✅ Any time (checks/debit) | ❌ Locked (penalty for early withdrawal) |

| Rate type | Variable (changes with Fed) | Variable | Fixed for term ✅ |

| Monthly fee | Usually none ✅ | Some have fees | None ✅ |

| FDIC insured | ✅ Yes | ✅ Yes | ✅ Yes |

| Best for | Emergency fund, short-term savings | Emergency fund + check writing | Money you won't need for 1+ year |

The Simple Decision Framework

Choose a HYSA if you want the best rate while keeping full access to your money — ideal for emergency funds and savings you might need within the next 12 months. Choose a CD if you have money you won't need for 1-5 years and want to lock in a fixed rate (especially valuable if you expect rates to fall). Choose a money market account if you need check-writing capability alongside your savings rate. For most Americans, the primary savings account should be a HYSA — the combination of competitive rate and full liquidity is unmatched.

🎯 What Makes a Good High-Yield Savings Account?

The APY is the most visible factor — but not the only one that matters. Here are the five criteria to evaluate before opening any high-yield savings account:

1. APY — But Check the Conditions

Always verify whether the advertised APY is conditional. SoFi's 3.80% requires direct deposit. CIT's 4.10% requires a promo code AND $5,000 minimum AND is only for 6 months. Marcus's 3.90% has no conditions — that's why it remains one of the most recommended despite not being the highest rate available. Know what you need to do (or not do) to earn the rate.

2. No Monthly Fees

Every account on our list charges zero monthly fees — this is non-negotiable. A $10/month fee on a $5,000 balance earning 3.90% APY ($195/year) would cost $120 in fees, reducing your net yield to 1.50%. Only consider accounts with no monthly maintenance fees.

3. FDIC Insurance

Every account on our list is FDIC-insured up to $250,000 per depositor per institution. SoFi offers up to $2 million in additional FDIC coverage through its partner bank network — uniquely valuable for high-balance savers. Never open a savings account (or any bank account) without FDIC insurance. Interest-bearing fintech products that are not FDIC-insured are a different risk category entirely.

4. Ease of External Transfers

A high-yield savings account at a different bank than your checking account requires ACH transfers to access funds — typically taking 1-3 business days. This is standard and acceptable for savings, but verify the transfer timeline before opening. Some accounts (like Ally) offer instant transfers to linked Ally checking accounts. If immediate access to your savings is important, a checking+savings combo at the same institution (SoFi, Axos) is worth considering.

5. Mobile App Quality

You'll interact with this account primarily through a mobile app. Check app store ratings and reviews before opening. CIT Bank, Marcus, Ally, and SoFi all have highly rated apps. Some lesser-known high-rate accounts have poorly rated apps with frequent transfer delays and customer service issues — a bad app experience can cost you time and frustration that outweighs the rate advantage.

❓ Frequently Asked Questions — High-Yield Savings Accounts June 2026

What is the best high-yield savings account in June 2026?

The best high-yield savings account for June 2026 depends on your situation. For the highest available APY: CIT Bank Platinum Savings at 4.10% (with promo code CITBOOST, $5,000 minimum, 6-month promo period). For the best no-conditions rate: Marcus by Goldman Sachs at 3.90% APY with no minimum balance and no monthly fees. For direct deposit users: SoFi at 3.80% APY. For goal-based savings with automation: Ally Online Savings at 3.80%. All options are FDIC-insured and pay 7-10x the national average of 0.38-0.62%.

Is it safe to put $50,000 in a high-yield savings account?

Yes — all the accounts on our list are FDIC-insured up to $250,000 per depositor per institution. This means your $50,000 is fully protected even if the bank fails. The FDIC has never failed to pay insured deposits since its founding in 1933. If you have more than $250,000 to save, spread it across multiple FDIC-insured institutions. SoFi offers up to $2 million in FDIC coverage through its partner bank network — uniquely suited for high-balance savers.

Will high-yield savings account rates go up or down in 2026?

HYSA rates are variable and track the Federal Reserve's federal funds rate. The Fed's current rate target is 3.50%–3.75% as of June 2026, held steady since early 2026. If the Fed cuts rates in the second half of 2026 (which Bankrate's analysts consider possible), HYSA rates would likely decrease within days of the cut. If the Fed holds rates steady through year-end, HYSA rates should remain near current levels. The best strategy: open a HYSA now to earn competitive rates on your current savings, rather than waiting to see what rates do.

Do I pay taxes on high-yield savings account interest?

Yes — interest earned on a HYSA is taxable as ordinary income in the year it's earned. Your bank will send you a Form 1099-INT if you earned $10 or more in interest during the year. On a $10,000 balance at 3.90% APY, you'd earn approximately $390 in interest — taxable at your marginal income tax rate. There is no way to shelter HYSA interest from taxes in a regular taxable account. For tax-advantaged savings, consider a Roth IRA or 529 plan for specific purposes — but for liquid emergency funds, the tax on HYSA interest is a reasonable cost for the flexibility and FDIC protection.

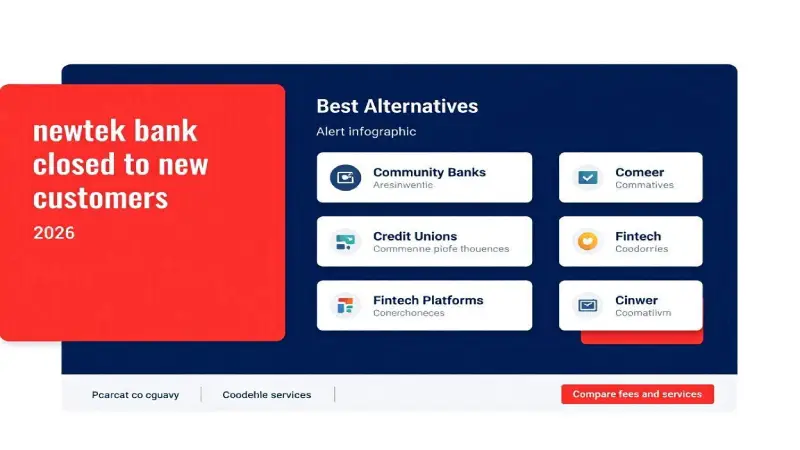

What happened to Newtek Bank and why is it closed to new customers?

Newtek Bank's Personal High Yield Savings account was named NerdWallet's Best Savings Account for 2026 with a 4.20% APY — the highest rate available from any major FDIC-insured bank at the time. The award and resulting publicity drove such overwhelming demand for new accounts that Newtek stopped accepting new customers. Existing Newtek account holders retain their accounts and rate. If you're looking for a new account, the best current alternatives are CIT Bank (4.10% promo), Marcus by Goldman Sachs (3.90%), and SoFi (3.80% with direct deposit).

✅ Final Verdict — Best High-Yield Savings Account June 2026

If you have savings sitting in a traditional bank account earning 0.38% APY, moving them to a HYSA is the highest-return, lowest-effort financial move available to you right now. The difference between 0.38% and 3.90% on a $10,000 balance is $352/year — for doing nothing more than opening a free account. Our top recommendations: Marcus by Goldman Sachs (3.90% APY, no conditions, no fees — the best no-strings rate) for most savers; CIT Bank with promo code CITBOOST (4.10% APY) if you have $5,000+ and want the absolute best short-term rate; SoFi (3.80% APY) if you have direct deposit from your employer. All are FDIC-insured, fee-free, and open to new customers today. For related financial guides see our Trump Accounts 2026 — How to Claim Your Child's $1,000 and Best Credit Cards USA 2026.

Disclaimer: APY rates are current as of June 1, 2026 and subject to change without notice. FDIC insurance limits apply. This article is for informational purposes only. Nexuora is not a financial institution and does not provide banking services. Always verify current rates directly with the institution before opening an account. Updated June 1, 2026.

Ahmada Ndao is a financial research analyst and independent journalist

specializing in US consumer finance, legal rights, and insurance markets.

With over 5 years covering American financial products, he has helped

thousands of readers navigate complex insurance decisions, find the right

legal representation, and optimize their credit strategies. His research

methodology combines primary data analysis, direct outreach to industry

professionals, and continuous monitoring of federal regulatory changes.

Ahmada’s work has been cited by financial communities across the US and

reviewed by licensed attorneys and insurance professionals for accuracy.