Mortgage Rates Forecast June 2026 — Will the Fed Cut Rates on June 17? What Every Homebuyer Must Know Before Locking In

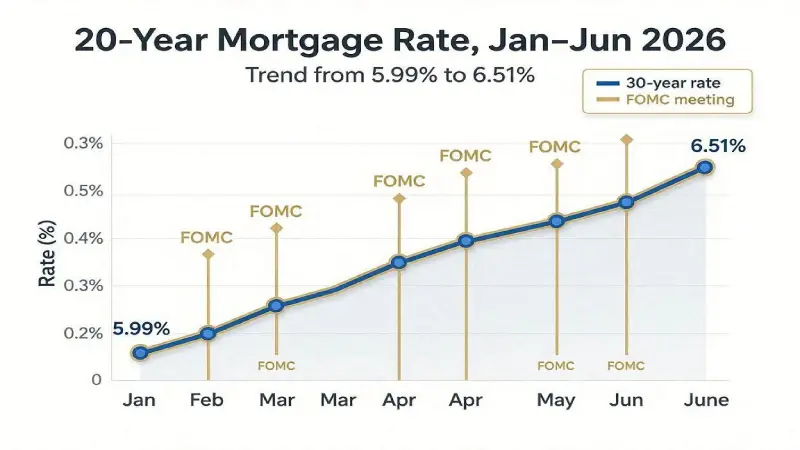

The 30-year fixed mortgage rate hit 6.51% on May 21, 2026 — up from 5.99% in January, a nearly 9% increase in five months. The Federal Reserve meets on June 17, 2026 with a new chairman — and markets are closely watching for any signal on rate direction. Should you lock in now at 6.51%? Wait for a potential post-meeting dip? Or hold off until later in the year when Bankrate's senior analyst predicts rates could fall below 6% for the first time since 2022? This guide gives you the complete picture: exactly where rates stand, every major expert forecast for June through December 2026, what the June 17 Fed meeting means, and a clear framework for deciding whether to lock now or wait.

📊 Where Mortgage Rates Stand Right Now — June 2026

| Loan Type | Current Rate (June 1, 2026) | 1 Month Ago | 1 Year Ago |

|---|---|---|---|

| 30-year fixed | 6.51% | 6.36% | ~7.00% |

| 15-year fixed | ~5.90% | ~5.75% | ~6.40% |

| 5/1 ARM | ~6.10% | ~5.95% | ~6.60% |

| FHA 30-year | ~6.20% | ~6.05% | ~6.70% |

| VA 30-year | ~6.00% | ~5.85% | ~6.45% |

| Jumbo 30-year | ~6.75% | ~6.60% | ~7.20% |

📅 What Happened to Mortgage Rates in 2026 So Far

| Date | 30-Year Rate | Key Driver |

|---|---|---|

| January 14, 2026 | 5.99% | Lowest since 2022 — post-Fed cut optimism |

| February 2, 2026 | 5.99% | Stable — Fed held rates steady |

| March 2026 | Rising | Iran conflict + surging oil prices + rising inflation |

| April 2026 | ~6.20% | Strong jobs report; inflation concerns |

| May 21, 2026 | 6.51% | Continued upward pressure; 10-yr Treasury yield rising |

| June 1, 2026 | ~6.51% | Holding ahead of June 17 Fed meeting |

The 2026 rate story is one of dashed hopes. Many buyers and homeowners started the year expecting rates to continue the downward trajectory from 2025. Instead, a combination of geopolitical shocks (Middle East conflict driving oil prices higher), persistent inflation above the Fed's 2% target, and a new Fed chairman with uncertain policy direction pushed rates nearly 10% higher from January to May. The CBS News analysis summed it up precisely: "Between the beginning of January and the end of May, mortgage interest rates rose by close to 10%, on average."

🏦 The June 17 Fed Meeting — 3 Scenarios

The Federal Reserve's June 17, 2026 meeting is the most important near-term event for mortgage rates. The current federal funds rate target range is 3.50%–3.75% — held steady since early 2026. Markets are pricing a very low probability of a cut at this meeting. Here are the three scenarios and their likely mortgage rate impact:

| Scenario | Probability | Likely Mortgage Rate Impact | What to Do |

|---|---|---|---|

| Fed holds rates (most likely) | ~80% | Rates stay near 6.51% — mild upward or downward drift of 0.1-0.2% | Lock now if buying; rates unlikely to improve significantly |

| Fed signals future cuts (possible) | ~15% | Rates could dip 0.2-0.3% on optimism alone — before any actual cut | Float if you can — may get brief window of lower rates post-meeting |

| Fed signals rate increase (unlikely) | ~5% | Rates could jump 0.3-0.5% immediately | Lock immediately if you have this fear |

Why the New Fed Chairman Matters

With a new Federal Reserve chairman in 2026, mortgage markets are particularly attentive to the language used in post-meeting statements. The new chairman's communication style and perceived hawkishness or dovishness can move mortgage rates even without a change in the actual federal funds rate. Markets will be parsing every word of the June 17 statement for signals about the second half of 2026. The 10-year Treasury yield — which mortgage rates closely track — has been rising in recent weeks, and a hawkish surprise from the new chair could push it higher still.

🔮 Expert Forecasts — Where Mortgage Rates Are Headed June–December 2026

| Forecaster | H2 2026 Forecast | Key Assumption |

|---|---|---|

| Bankrate (Ted Rossman) | Could fall below 6% — as low as 5.5% possible | Fed cuts + recession scare; inflation must cooperate |

| Fannie Mae | Hover around 6% through rest of 2026 and into 2027 | Gradual easing, no major catalyst |

| Zillow | Above 6% full year 2026 | Inflation stickiness; conservative forecast |

| Norada Real Estate | 6.0%–6.4% range likely; dips to 5.5% if all conditions align | Fed policy + inflation + global events |

| MIDFLORIDA | 5.5%–6% possible by late 2026 | Inflation on target + Fed cuts |

| Bright MLS (Sturtevant) | Slightly lower rates help affordability; 5%–6% range | Moderate improvement in affordability |

The Consensus View

The majority of forecasters expect 30-year rates to average between 6.0% and 6.5% for the second half of 2026 — essentially sideways from current levels. The bull case (rates falling to 5.5%) requires: inflation returning to the Fed's 2% target, the Fed cutting rates at least twice in H2 2026, and no new geopolitical shocks. The bear case (rates rising toward 7%) requires persistent inflation or a policy error. The base case is modest drift around current levels with high volatility around Fed meetings and economic data releases.

💰 Real Payment Impact by Rate Change

| Loan Amount | At 5.5% | At 6.0% | At 6.51% | At 7.0% |

|---|---|---|---|---|

| $250,000 | $1,420/mo | $1,499/mo | $1,581/mo | $1,663/mo |

| $350,000 | $1,987/mo | $2,098/mo | $2,213/mo | $2,329/mo |

| $400,000 | $2,271/mo | $2,398/mo | $2,529/mo | $2,661/mo |

| $500,000 | $2,839/mo | $2,998/mo | $3,161/mo | $3,327/mo |

| $600,000 | $3,406/mo | $3,597/mo | $3,794/mo | $3,992/mo |

On a $400,000 loan, the difference between locking at 6.51% today versus waiting for a potential 6.0% rate is $131/month — or $47,160 over 30 years. If rates instead rise to 7%, locking today at 6.51% would save $132/month versus future buyers. This symmetry illustrates why the lock-or-wait decision is fundamentally a risk management question: what is the probability of rates falling versus rising, and what is the cost of being wrong in each direction?

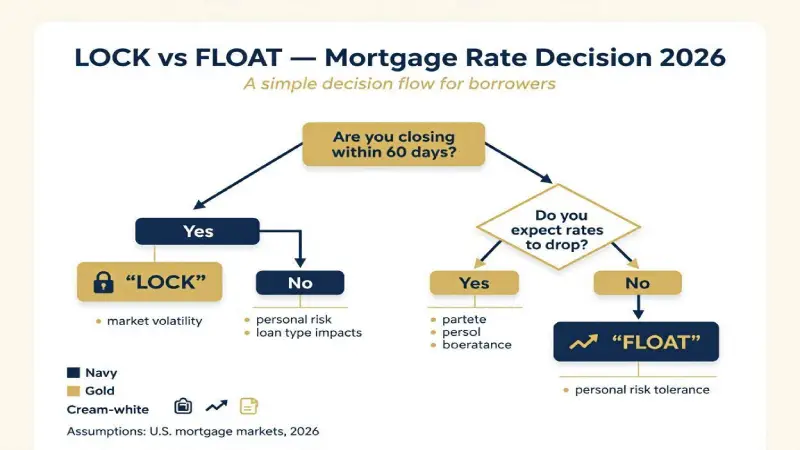

🔒 Should You Lock In Now or Wait?

| Your Situation | Recommendation | Reasoning |

|---|---|---|

| Closing in under 30 days | Lock now | Too close to closing to risk rate movement |

| Closing in 30–60 days | Consider locking with float-down option | Float-down lets you capture lower rates if they fall; protects against rises |

| Closing in 60–90 days | Float until closer to June 17 | June 17 Fed meeting may provide clarity; monitor 10-year Treasury |

| Just starting to look | Get pre-approved now, lock when ready | Pre-approval doesn't require locking; locks rates for 60–90 days |

| Fear of rates rising to 7%+ | Lock immediately | Peace of mind worth the potential missed savings |

| Flexibility on timing | Float and monitor | Watch 10-year Treasury yield; if it falls, rates follow |

The Float-Down Option — Best of Both Worlds

Many lenders offer a "float-down" option — you lock a rate today, but if rates fall before your closing, you get the lower rate. Float-down options typically cost 0.25-0.50% of the loan amount ($1,000-$2,000 on a $400,000 loan) but provide insurance against the frustration of watching rates fall after you've locked. In a high-volatility rate environment like June 2026, float-down options are worth considering for buyers within 60 days of closing.

The 10-Year Treasury Signal

The most reliable leading indicator for mortgage rate direction is the 10-year US Treasury yield. Mortgage rates track the 10-year Treasury closely — when Treasury yields fall, mortgage rates typically follow within days. Monitor the 10-year Treasury yield daily (available free at TreasuryYields.gov or any financial news site). If the 10-year yield drops significantly around the June 17 Fed meeting, it's a signal that mortgage rates may follow.

🎯 How to Get the Best Mortgage Rate in June 2026

1. Compare at Least 4 Lenders

The CFPB estimates that borrowers who get 4+ quotes save an average of 0.5% on their rate versus borrowers who use only one lender. On a $400,000 loan, 0.5% is $133/month and $47,880 over 30 years. Get quotes from your bank, a credit union, at least one online lender (Rocket Mortgage, Better.com, LoanDepot), and a mortgage broker who can access multiple lenders simultaneously.

2. Improve Your Credit Score Before Applying

Credit score has an enormous impact on the rate you receive. A borrower with a 760+ FICO score typically gets rates 0.5-1.0% lower than a borrower with a 680 score. Pay down credit card balances below 30% utilization, avoid new credit inquiries for 90 days before applying, and dispute any errors on your credit report. Even a 20-point credit score improvement can save $50-100/month on a typical mortgage.

3. Consider Mortgage Points

Buying mortgage points (paying 1% of the loan amount upfront to reduce the rate by approximately 0.25%) makes sense if you plan to stay in the home long-term. At current rates, one point on a $400,000 loan costs $4,000 and reduces your rate by ~0.25% — saving $60/month. Break-even: approximately 67 months (5.5 years). If you plan to stay 7+ years, buying 1-2 points is usually worthwhile.

4. Consider a 15-Year Mortgage

The 15-year fixed rate is approximately 5.90% today — 0.61% below the 30-year rate. On a $300,000 loan, the 15-year has a higher monthly payment ($2,520 vs $1,897) but saves approximately $175,000 in total interest versus the 30-year. For buyers who can afford the higher monthly payment, the 15-year delivers dramatically better lifetime economics.

🔄 Should You Refinance Now?

For existing homeowners considering refinancing, the calculus depends almost entirely on your current rate. The general rule: refinancing makes financial sense if you can reduce your rate by at least 0.75-1.0% and plan to stay in the home long enough to recoup closing costs (typically 2-3 years).

| Your Current Rate | Refinance at 6.51%? | Why |

|---|---|---|

| 3.0%–3.5% (pandemic era) | ❌ No | Current rates are 3% higher — refinancing would cost you significantly |

| 4.0%–5.0% | ❌ No | Still above current market rates — don't refinance |

| 6.5%–7.0% | ⚠️ Maybe — watch June 17 | Could benefit if rates dip to 6.0%–6.2% after Fed meeting |

| 7.0%–8.0% | ✅ Yes — shop now | Current 6.51% rate is meaningfully lower; refinancing makes sense |

| 8.0%+ | ✅ Absolutely | Refinancing to 6.51% saves $200-400/month on most loan sizes |

❓ Frequently Asked Questions — Mortgage Rates June 2026

What is the current 30-year mortgage rate in June 2026?

The average 30-year fixed mortgage rate is approximately 6.51% as of June 1, 2026, according to Freddie Mac's weekly survey. This is up from 5.99% in January 2026 — an increase of roughly 9% driven by Middle East conflict, rising oil prices, and persistent inflation above the Fed's 2% target. The 15-year fixed rate is approximately 5.90%, and FHA 30-year rates are approximately 6.20%. Individual rates vary by lender, credit score, down payment, and loan type — get multiple quotes for your specific situation.

Will mortgage rates go down in June 2026?

Mortgage rates may dip slightly around the June 17 Federal Reserve meeting if the new chairman signals future rate cuts — but most forecasters don't expect a dramatic decline in June. The consensus is that rates will stay in the 6.1%–6.5% range through summer 2026. Bankrate's senior analyst believes rates could fall below 6% by late 2026 if inflation cooperates, but this is the bull case, not the base case. Buyers shouldn't plan around a significant rate drop in June — the risk of waiting and seeing rates rise is real.

Should I lock my mortgage rate now or wait for rates to drop?

If you're closing within 30 days, lock now — too close to closing to risk rate movement. If closing in 30-60 days, consider a float-down lock (locks today's rate with the ability to capture lower rates if they fall). If closing in 60-90 days, you can float until after the June 17 Fed meeting for more clarity. Most housing economists advise against waiting significantly — the downside risk (rates rising to 7%) is as plausible as the upside (rates falling to 6%). The payment difference between locking at 6.51% versus a hypothetical 6.0% is about $131/month on a $400,000 loan — weigh whether that potential savings is worth the risk of rates moving higher.

What will happen to mortgage rates after the June 17 Fed meeting?

Markets are pricing approximately 80% probability that the Fed holds rates steady at the June 17 meeting (current range: 3.50%–3.75%). If the Fed holds and the new chairman's language is neutral, mortgage rates will likely stay near current levels of 6.5%. If the chairman signals future cuts, rates could dip 0.2-0.3% on optimism. If the chairman sounds hawkish, rates could jump 0.3-0.5%. The June 17 meeting's most important element will be the post-meeting statement language — watch for words like "patient" (holding rates) or "data-dependent" (signaling flexibility).

What mortgage rate can I get with a 760 credit score?

With a 760+ FICO credit score and a 20% down payment, you typically qualify for the best advertised rates — approximately 0.5-1.0% below what borrowers with 680 scores receive. At current market conditions, a 760+ score borrower might receive quotes of 6.1%–6.3% for a conventional 30-year mortgage, versus 6.7%–7.0% for a 680 score borrower. Improving your credit score from 720 to 760 before applying can save $50-100/month on a $400,000 mortgage. Always get multiple quotes — rates vary by lender even for identical credit profiles.

✅ Final Verdict — Mortgage Rates June 2026

Mortgage rates at 6.51% in June 2026 are frustrating for buyers who watched rates hit 5.99% in January — but they remain below the 7-8% range of 2023 and are historically within the normal range. The most important action for any homebuyer right now: get quotes from at least 4 lenders before locking. The spread between the best and worst lender quote for the same borrower can exceed 0.5% — a difference worth more than any rate movement anticipated from the June 17 Fed meeting. Watch the 10-year Treasury yield for signals; lock before the June 17 meeting if you're risk-averse. For related financial guides see our Best High-Yield Savings Accounts June 2026 and Best Homeowners Insurance USA 2026.

Disclaimer: Mortgage rate data is based on Freddie Mac weekly survey and lender data current as of June 1, 2026. Rates are subject to daily change. Individual rates vary significantly by lender, credit score, down payment, and loan type. This article is for informational purposes only and does not constitute financial or mortgage advice. Nexuora is not a lender. Updated June 1, 2026.

Ahmada Ndao is a financial research analyst and independent journalist

specializing in US consumer finance, legal rights, and insurance markets.

With over 5 years covering American financial products, he has helped

thousands of readers navigate complex insurance decisions, find the right

legal representation, and optimize their credit strategies. His research

methodology combines primary data analysis, direct outreach to industry

professionals, and continuous monitoring of federal regulatory changes.

Ahmada’s work has been cited by financial communities across the US and

reviewed by licensed attorneys and insurance professionals for accuracy.