Cheapest Homeowners Insurance USA 2026 — How to Cut Your Premium by $500/Year Without Losing Coverage

Homeowners insurance premiums rose 21% in 2025 alone — and the average American now pays $2,285/year for $300,000 in dwelling coverage. If your renewal notice arrived with a premium increase you didn't expect, you're not alone. But there's good news: most homeowners are significantly overpaying, and the strategies to reduce that bill are well-established. According to Insurify's 2026 data, the difference between the most expensive and cheapest home insurer for the same home can exceed $1,000/year. This guide gives you the 6 cheapest homeowners insurance companies available in 2026 — plus 10 proven strategies to cut your current premium by $300–$700 without sacrificing meaningful coverage.

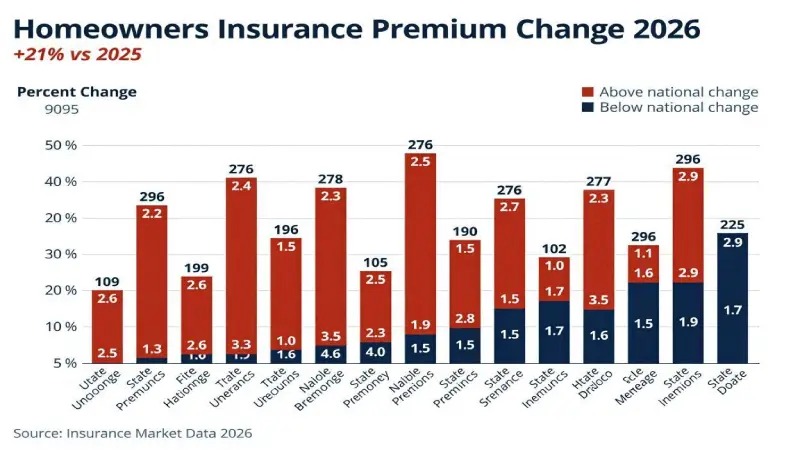

📈 Why Home Insurance Got So Expensive in 2026

Understanding why your premium increased helps you identify where you have leverage to reduce it. Four factors are driving the 2026 surge:

Construction cost inflation: According to Insurify, since 2020, the cost to replace a home has increased 34%. Insurance premiums must keep pace with the replacement cost they guarantee — so even if you've made no claims and your home hasn't changed, your insured value (and premium) rose automatically. Catastrophic weather events: California wildfires, Florida hurricanes, Gulf Coast flooding, and Midwest tornadoes in 2024-2025 produced record insured losses. Insurers raised premiums industry-wide to rebuild reserves. Reinsurance costs: Insurance companies buy their own insurance (reinsurance) to cover catastrophic losses. Reinsurance costs rose significantly in 2024-2025, and those costs flow directly into policyholder premiums. Market withdrawal: State Farm and Allstate stopped writing new homeowners policies in California in 2023. Other carriers have restricted coverage in Florida, Louisiana, and coastal regions — reducing competition and allowing remaining carriers to raise rates.

⚡ Quick Pick — Cheapest Homeowners Insurance by Profile

| Your Profile | Cheapest Option | Est. Annual Premium |

|---|---|---|

| Military / veteran | USAA | ~$1,940/yr ✅ |

| Bundling home + auto | Auto-Owners or Erie | 15-25% below average |

| New home (built last 10 yrs) | Travelers or State Farm | Up to 15% discount |

| Budget overall (non-USAA) | Auto-Owners Insurance | Consistently below average |

| Midwest/East homeowner | Erie Insurance | Below state avg in eligible states |

| Claims-free 5+ years | Amica Mutual | Dividend policy returns 5-20% |

| High-value home ($750K+) | Chubb or AIG Private Client | Specialized — get individual quotes |

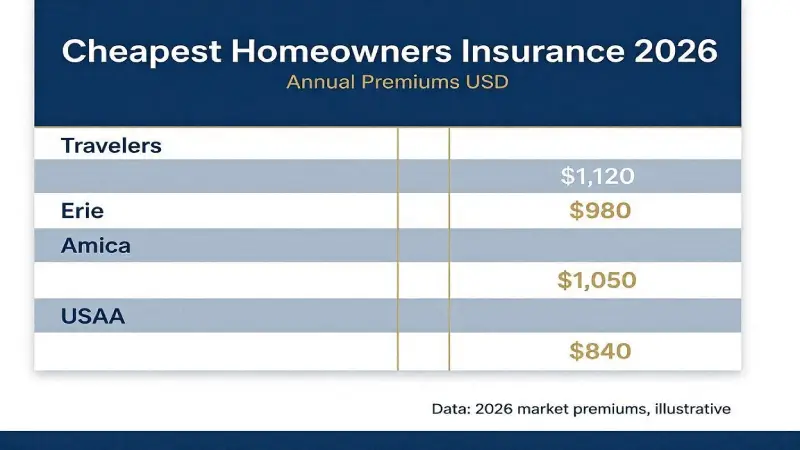

💰 The 6 Cheapest Homeowners Insurance Companies 2026

#1 — USAA: Cheapest Overall (Military Families Only)

USAA has the cheapest sample rate in U.S. News' 2026 study at approximately $1,940/year for $300,000 in dwelling coverage — $345/year below the national average of $2,285. USAA also earns the highest J.D. Power customer satisfaction scores of any major insurer. The limitation: USAA is exclusively available to active military, veterans, and their immediate families. If you qualify, there is no reason to compare anywhere else. For our full analysis, see our Best Homeowners Insurance USA 2026 guide.

#2 — Auto-Owners Insurance: Cheapest for Non-Military

Auto-Owners Insurance consistently offers below-average premiums for homeowners without military affiliation. Available in 26 states through independent agents, Auto-Owners earns high customer satisfaction scores and low NAIC complaint ratios. Their bundling discount (home + auto) is among the most generous available — often producing combined savings of 20-25%. The limitation: only available in 26 states and exclusively through independent agents (no direct online binding). Find an agent at auto-owners.com.

#3 — Erie Insurance: Best for Midwest and East Coast

According to NerdWallet, Erie offers guaranteed replacement cost coverage as standard — most competitors charge extra for this. Their multi-policy discount saves 15-25% on home + auto bundles. U.S. News notes Erie draws a low proportion of NAIC complaints — signaling strong claims satisfaction. Erie operates in 12 Midwest and East Coast states plus Washington D.C. If Erie is available in your state, it is consistently among the most competitive options.

#4 — Travelers: NerdWallet's Budget-Friendly Pick 2026

NerdWallet's 2026 review gives Travelers 4.4 out of 5 stars for overall performance. At $2,710/year average, Travelers is above the national average — but their discount stack is one of the deepest available: new home discount, claims-free discount, green home discount, protective device discount, and a unique Decreasing Deductible program that adds a $100 credit to your deductible annually. U.S. News ranks Travelers as the No. 2 best option for home + auto bundles. Note: Travelers has availability restrictions in 18+ states including Alaska, California, and Florida — check availability in your state first. For a full Travelers alternative, see our Liberty Mutual Homeowners Insurance Review 2026.

#5 — State Farm: Largest Network + Competitive Bundling

State Farm averages $2,415/year — $130/year below the national average — with a 17% home + auto bundle discount that can bring total combined premiums significantly below competitors. State Farm's 19,000+ agent network means local service in every state. Our full Best Homeowners Insurance comparison ranks State Farm as the top choice for most non-military homeowners nationally.

#6 — Amica Mutual: Best for Long-Term Policyholders

Amica is a mutual insurance company — meaning policyholders are owners who receive dividends. Amica's dividend policies return 5-20% of annual premiums as dividends each year, effectively reducing your net annual cost. Over 10 years, a 10% dividend on a $2,200 premium saves $2,200 cumulatively. Amica has the lowest NAIC complaint index of any major homeowners insurer (0.43 — less than half the industry average). The trade-off: higher base premiums before the dividend. Available nationwide through direct enrollment at amica.com.

🎯 10 Proven Ways to Cut Your Home Insurance Premium by $300–$700

Strategy 1 — Bundle Home + Auto (Save 17-25%)

The single highest-impact discount available. According to U.S. News, bundling home and auto policies with the same insurer saves 17-25% on the home policy at most major carriers. On a $2,285/year home premium, 20% savings = $457/year. Over 5 years, that's $2,285 in cumulative savings. If you currently have your home and auto with different companies, get a combined quote from State Farm, Travelers, Auto-Owners, or Liberty Mutual. Their combined home + auto pricing frequently beats the sum of two separate policies at competing insurers.

Strategy 2 — Raise Your Deductible (Save 15-25%)

Insurify confirms that raising your deductible from $500 to $1,000 saves up to 25% on premiums. The math: on a $2,285 premium, 20% savings = $457/year. Moving from $500 to $2,500 deductible can save 25-35%. The trade-off: make sure you can afford the higher deductible out of pocket. Rule of thumb: only raise your deductible to an amount you have in your emergency fund. Put the annual savings into your high-yield savings account — see our Best High-Yield Savings Accounts June 2026 guide.

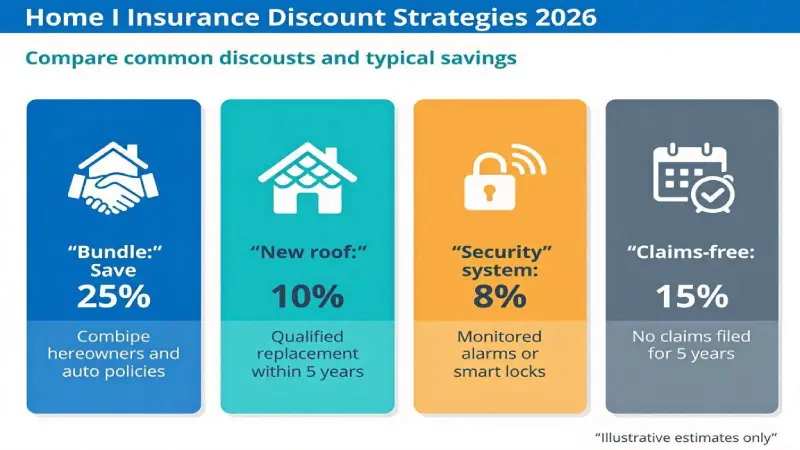

Strategy 3 — New Roof Discount (Save 5-15%)

A new roof is the single largest factor in reducing home insurance cost for older homes. Most insurers give a 5-15% discount for a roof replaced in the last 5 years. If your roof is approaching 15-20 years old, proactively replacing it (especially with impact-resistant Class 4 shingles) can both lower your premium and avoid future claim complications. Some carriers — like Liberty Mutual's Better Roof Replacement endorsement — will pay to replace your damaged roof with impact-resistant materials at claim time. See our Liberty Mutual Review 2026 for details on this specific coverage.

Strategy 4 — Install Security and Smart Home Devices (Save 5-15%)

Smoke detectors, burglar alarms, fire alarms, deadbolt locks, and automatic sprinkler systems all qualify for discounts at most major carriers. Smart home systems (leak detectors, water shutoff valves, smart smoke detectors) increasingly qualify for additional savings. Travelers specifically rewards protective devices with discounts. Nationwide's smart home program provides free or discounted leak detection devices that can also qualify you for premium savings.

Strategy 5 — Claims-Free Discount (Save 10-15%)

Most insurers reward policyholders who haven't filed claims in the past 3-5 years with 10-15% discounts. If you're claims-free, call your insurer and ask explicitly for the claims-free discount — it's not always applied automatically. Additionally, consider whether small claims are worth filing: a $600 repair claim may cost you more in lost claims-free discount (potentially $228-$342/year) than the claim itself pays out.

Strategy 6 — Improve Your Credit Score (Save Up to 20%)

In 44 states, insurers use credit-based insurance scores to set premiums (California, Massachusetts, and Maryland prohibit this). According to Insurify, maintaining good credit history significantly reduces premiums. Improving from fair to good credit can save 10-20% on home insurance premiums. Pay down credit card balances below 30% utilization and pay all bills on time — these are the two highest-impact credit score improvements available.

Strategy 7 — Pay Annually Instead of Monthly (Save 3-6%)

Most insurers charge an installment fee for monthly payment plans. Paying the full annual premium upfront eliminates this fee. On a $2,285 premium, 5% savings = $114/year. If you use a credit card with cashback rewards to pay the annual premium, you also earn rewards on the payment. See our Best Credit Cards USA 2026 guide for cards that maximize rewards on insurance payments.

Strategy 8 — Shop at Renewal (Potential Save $200-$600)

Loyalty to a home insurer is almost never financially rewarded. Most carriers offer their best rates to new customers, not renewing ones. Insurify recommends getting at least 3 quotes at every renewal — your current insurer's quote, plus two competitors. Insurance comparison platforms like Policygenius and Insurify let you compare multiple carriers simultaneously in minutes.

Strategy 9 — Early Shopper Discount (Save Up to 8%)

Travelers, Erie, and several other carriers offer discounts of 5-8% if you get a quote 7-60 days before your current policy expires. Shopping before your renewal date — not when it arrives — gives you leverage and qualifies you for this discount. Set a calendar reminder 60 days before your renewal.

Strategy 10 — Review and Right-Size Your Coverage

Many homeowners are over-insured. Common examples: insuring your home at market value rather than replacement cost (they're not the same); carrying scheduled jewelry or art coverage for items you no longer own; maintaining high liability limits beyond what your assets justify. Review your Coverage A (dwelling) amount with your insurer annually to ensure it reflects current construction costs — not market value, which includes land that isn't insurable. Removing coverage you don't need directly reduces your premium.

🧮 Real Savings Calculator — How Much Can You Save?

| Strategy | Estimated Saving | On $2,285 Premium | Effort Required |

|---|---|---|---|

| Bundle home + auto | 17-25% | $388–$571/yr ✅ | Medium (switch insurer) |

| Raise deductible ($500→$2,500) | 15-25% | $343–$571/yr ✅ | Low (one phone call) |

| Claims-free discount | 10-15% | $229–$343/yr | Low (ask your insurer) |

| New roof | 5-15% | $114–$343/yr | High (capital required) |

| Security system | 5-15% | $114–$343/yr | Medium (install device) |

| Pay annually | 3-6% | $69–$137/yr | Low (payment method) |

| Early shopper discount | 5-8% | $114–$183/yr | Low (shop 60 days early) |

| Credit score improvement | 10-20% | $229–$457/yr | Medium (time required) |

Realistic combined savings scenario: Bundle home + auto (20% = $457) + raise deductible to $2,500 (20% applied after bundle = $365 on reduced base) + claims-free discount (10% = $183) = total annual savings of approximately $500–$700 on a $2,285 starting premium. That's $400-$600 per year in your pocket, permanently, from three changes that take less than 2 hours to execute.

🔥 What to Do If You Live in a High-Risk State

Florida

Florida's homeowners insurance market is in crisis — multiple carriers have exited, and remaining insurers have raised rates dramatically. If you can't find affordable coverage: Citizens Property Insurance (Florida's insurer of last resort) provides coverage when private market options are unavailable or unaffordable. Rates are regulated but typically higher than private market. Fortifying your home through the My Safe Florida Home program can qualify for meaningful discounts.

California

State Farm and Allstate no longer write new homeowners policies in California. For California homeowners who've been non-renewed: the California FAIR Plan provides basic fire coverage as a last resort. Surplus lines carriers (through an independent broker) offer non-admitted coverage for higher-risk properties. Travelers, Nationwide, and Mercury Insurance remain active in most California markets.

Louisiana

Louisiana homeowners face some of the highest premiums in the country following repeated hurricane losses. The Louisiana Citizens Property Insurance Corporation provides coverage for homeowners who cannot find private market coverage. Consider wind mitigation improvements — fortified roof construction can reduce wind premiums significantly.

❓ Frequently Asked Questions — Cheapest Homeowners Insurance 2026

What is the cheapest homeowners insurance company in 2026?

USAA offers the cheapest homeowners insurance rates nationally at approximately $1,940/year for $300,000 in dwelling coverage — but is exclusively available to military members, veterans, and their immediate families. For non-military homeowners, Auto-Owners Insurance and Erie Insurance consistently offer below-average rates in their operating states. State Farm averages $2,415/year nationally — below the $2,285 average. Travelers at $2,710/year is above average but offers extensive discounts that can significantly reduce the effective premium. Always compare at least 3-4 quotes for your specific property, location, and profile.

How can I lower my homeowners insurance premium?

The three highest-impact strategies to lower your home insurance premium are: (1) Bundle home and auto with the same insurer — saves 17-25% on the home policy; (2) Raise your deductible from $500 to $1,000 or $2,500 — saves 15-25%; (3) Ask your insurer what discounts you qualify for that aren't currently applied — claims-free, security device, new home, and annual payment discounts are commonly missed. Combining strategies 1 and 2 alone can save $500-$700/year on a typical $2,285 premium.

Is it worth raising my homeowners insurance deductible?

Yes — for most homeowners, raising the deductible is the most efficient premium reduction available. Increasing from $500 to $1,000 typically saves 10-20% on premiums. Increasing to $2,500 can save 25-35%. The rule: only raise your deductible to an amount you have in an accessible savings account (not your long-term retirement savings). If you have a $2,500 emergency fund, a $2,500 deductible is appropriate. Put the annual premium savings into your emergency fund to build it faster — see our Best High-Yield Savings Accounts guide for where to keep that money earning the most interest.

Does bundling home and auto insurance always save money?

Usually, but not always. Bundling saves 17-25% on the home policy at most major carriers — but this discount is applied to the home premium only. In some cases, the bundled auto premium at the same carrier is higher than a standalone auto quote from a competitor, offsetting the home savings. Always compare: (a) your current home insurer's bundle quote, (b) a competitor's standalone home quote, and (c) the total combined bundle cost at 2-3 different insurers. The total combined package price is what matters — not the individual policy discounts.

Why did my homeowners insurance go up so much in 2025-2026?

Four factors drove the 21% average homeowners insurance premium increase in 2025: (1) Construction cost inflation of 34% since 2020, which forces insurers to increase Coverage A limits and premiums to maintain adequate replacement cost coverage; (2) Record catastrophic losses from California wildfires, Florida and Gulf Coast hurricanes, and Midwest severe weather events; (3) Rising reinsurance costs as reinsurers priced in climate-related risk increases; (4) Market withdrawal by major carriers from high-risk states, reducing competition. These factors affect the entire industry, not just your specific insurer or property.

✅ Final Verdict — How to Cut Your Home Insurance Bill in 2026

The average homeowner is overpaying for home insurance — not because the market is unfair, but because most people never shop at renewal and never ask about available discounts. The three actions that take less than 2 hours and save the most money: (1) Get quotes from at least 3 competitors before your next renewal (use Policygenius or Insurify); (2) Ask your current insurer what discounts you qualify for that aren't applied; (3) Raise your deductible to match your emergency fund level. Combined, these three actions can realistically save $400-$700/year on a typical premium — permanently. For a complete comparison of the best homeowners insurance providers beyond price, see our Best Homeowners Insurance USA 2026 guide and our Liberty Mutual Homeowners Insurance Review 2026. For managing the savings from your reduced premium, see our Best High-Yield Savings Accounts June 2026.

Disclaimer: Premium estimates based on U.S. News, NerdWallet, and Insurify rate studies as of June 2026. Individual premiums vary by location, home age, coverage amounts, and personal profile. Always obtain personalized quotes before switching insurers. Nexuora is not affiliated with any insurer listed. Updated June 4, 2026.

Ahmada Ndao is a financial research analyst and independent journalist

specializing in US consumer finance, legal rights, and insurance markets.

With over 5 years covering American financial products, he has helped

thousands of readers navigate complex insurance decisions, find the right

legal representation, and optimize their credit strategies. His research

methodology combines primary data analysis, direct outreach to industry

professionals, and continuous monitoring of federal regulatory changes.

Ahmada’s work has been cited by financial communities across the US and

reviewed by licensed attorneys and insurance professionals for accuracy.