iSelect Car Insurance Review Australia 2026 — Is It Worth Using? Real Pros, Cons & Best Alternatives

iSelect is one of Australia's most recognisable insurance comparison platforms — appearing on television, partnering with major brands, and processing millions of insurance quote requests annually. But is it actually the best way to find cheap car insurance in Australia in 2026? As an expert comparison platform reviewer, we analysed how iSelect works, what it genuinely does well, where it falls short, what it costs you (spoiler: more than you think), and what alternatives give you better results. Whether you are renewing your comprehensive cover, shopping for third party property damage, or simply trying to understand the Australian car insurance market, this complete 2026 review tells you exactly what to expect from iSelect — and when to use it versus going direct.

🔍 What Is iSelect Australia — How It Works in 2026

iSelect Limited (ASX: ISU) is an Australian financial services comparison company founded in 2000 and publicly listed on the ASX. The business model is straightforward: iSelect partners with insurance companies, utility providers, and financial product issuers, allowing consumers to compare multiple offers in a single interface. For car insurance specifically, iSelect receives a referral commission from partner insurers when a consumer purchases a policy through the iSelect platform.

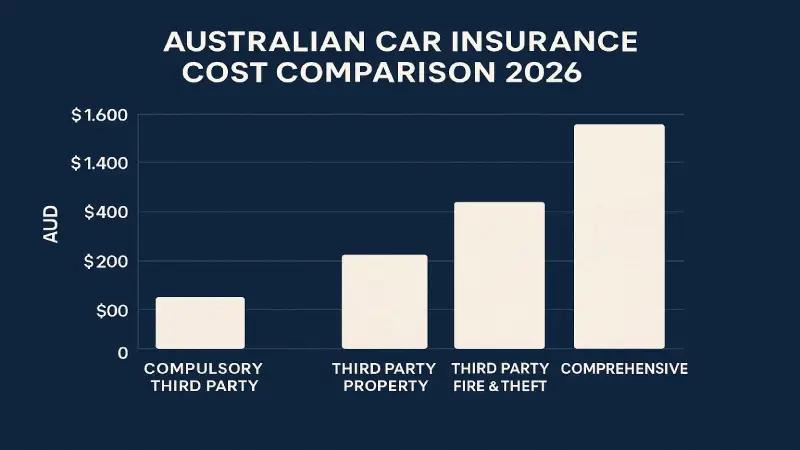

When you visit iSelect to compare car insurance, the process works as follows. You enter your vehicle details — make, model, year, registration — along with your personal information including age, address, licence history, and the type of cover you want (comprehensive, third party fire and theft, or third party property only). iSelect's system queries its panel of partner insurers and returns a list of quotes ranked by price. You can then review policy details, compare cover levels, and click through to purchase directly from the insurer or through the iSelect interface.

iSelect's Car Insurance Panel in 2026

iSelect does not compare every car insurer in Australia. It compares a curated panel of partner insurers who have commercial agreements with iSelect. In 2026, iSelect's car insurance panel includes partners from the following major groups: IAG (which underwrites NRMA, CGU, SGIO, SGIC, and Swann), Suncorp (which underwrites AAMI, GIO, Apia, Shannons, and Bingle), Allianz Australia, QBE Insurance, and Budget Direct. Woolworths Insurance, Youi, and several other insurers are not on the iSelect panel — meaning you will not see their quotes when using iSelect, even if they offer lower prices for your specific profile.

iSelect vs the Full Market

The Australian car insurance market has approximately 40+ active underwriters. iSelect's panel covers perhaps 60–70% of available products by premium volume — but critically misses some of the most competitive pricing from direct-only insurers. ASIC data from 2025 suggests that consumers who compare on a single platform miss an average of AU$220 in potential annual savings versus those who check at least two comparison sites plus one or two direct insurer sites.

🏢 Which Insurers Does iSelect Compare in 2026?

| Insurer / Brand | Parent Group | On iSelect? | Known For |

|---|---|---|---|

| NRMA Insurance | IAG | ✅ Yes | NSW/ACT/QLD leader · Strong claims service |

| AAMI | Suncorp | ✅ Yes | Strong brand · Cheaper rates for many profiles |

| Budget Direct | Auto & General | ✅ Yes | Consistently cheapest for many profiles |

| Allianz | Allianz SE (Germany) | ✅ Yes | Premium coverage · Good rental car |

| GIO | Suncorp | ✅ Yes | NSW/ACT specialist · Good CTP add-ons |

| QBE Insurance | QBE Group | ✅ Yes | Agreed value specialist |

| Youi | OUTsurance (SA) | ❌ Not on iSelect | Pay-as-you-drive · Usage-based pricing · Often cheapest for low mileage |

| Woolworths Insurance | Hollard | ❌ Not on iSelect | Competitive pricing for Woolworths shoppers |

| RACV / RAA / RACT / RAC | State motoring clubs | ❌ Not on iSelect | Member benefits · Often very competitive in their states |

| Coles Insurance | Hollard | ❌ Not on iSelect | Competitive for Coles loyalty customers |

| Bingle | Suncorp | ⚠️ Sometimes | Cheapest Suncorp option · Basic cover only |

| Huddle | IAG | ❌ Not on iSelect | Digital-only · IAG-backed · Competitive |

✅ iSelect Pros — What It Genuinely Does Well

1. Fast side-by-side premium comparison

iSelect's core value is speed and convenience. Entering your details once and receiving multiple quotes simultaneously from partner insurers genuinely saves time versus visiting each insurer's website individually. For a standard comprehensive car insurance comparison across iSelect's panel of 8–12 partner insurers, the process takes approximately 5–8 minutes — versus 40–60 minutes if you visited each insurer separately. For time-poor consumers who want a reasonable starting-point comparison quickly, this efficiency is real.

2. Independent advisors available for complex situations

Unlike pure digital comparison tools, iSelect offers access to human insurance advisors who can discuss your specific situation — unusual vehicle types, high-value vehicles, novice drivers, complex claims histories, or specific coverage questions. For straightforward mainstream vehicles, the digital self-service tool is sufficient. For complex situations, the advisor access is genuinely valuable and differentiates iSelect from fully automated comparison tools.

3. Policy detail comparison — not just price

iSelect's interface allows you to click into each quote and review policy features side-by-side — excess levels, rental car cover, windscreen cover, new-for-old cover, emergency accommodation cover, and agreed versus market value options. This feature-level comparison helps consumers avoid choosing a lower-premium policy that lacks a critical feature they need — a common mistake when comparing only on price.

4. Compliant and regulated

iSelect holds an Australian Financial Services Licence (AFSL) — meaning it is regulated by ASIC and must comply with responsible disclosure obligations. The comparison results must be genuine, the commission structure must be disclosed, and the advice (where provided) must meet professional standards. This regulatory compliance makes iSelect a trustworthy platform — unlike some offshore comparison sites that operate without ASIC oversight.

5. Customer service and after-sale support

iSelect provides genuine after-sale customer support — you can call them with questions about your policy after purchase, and they maintain a complaints resolution process. This is more than most digital-only comparison tools provide and gives consumers an additional layer of support beyond the insurer's own service teams.

❌ iSelect Cons — Critical Limitations to Know Before Using

1. Does not cover the full market

This is iSelect's most significant limitation. The Australian car insurance market includes Youi, the state motoring clubs (RACV, RAA, RACT, RAC), Woolworths Insurance, Coles Insurance, Huddle, and other providers that are not on iSelect's panel. For some driver profiles — particularly low-mileage drivers (where Youi's pay-as-you-drive pricing excels), RACV members in Victoria, or RAA members in South Australia — the cheapest available policy will not appear in iSelect's results. If you rely exclusively on iSelect, you may miss your cheapest option.

2. Policies may cost more than going direct

Some Australian insurers offer lower premiums when consumers go direct — bypassing comparison platforms — because the insurer retains the referral commission that would otherwise be paid to the comparison site. AAMI, Budget Direct, and Youi in particular have been observed offering prices through their direct channels that were not replicated on comparison platforms. Always check the insurer's direct website quote after finding your best iSelect result — you may find a lower premium for the same policy.

3. Commission-based ranking creates potential bias

iSelect earns higher commissions from some insurers than others. While ASIC regulations require disclosure and prohibit deliberately misleading rankings, the commercial structure creates inherent tension between presenting the genuinely best product for each consumer and the economic incentive to feature higher-commission partners prominently. iSelect discloses this in its Financial Services Guide — but many consumers do not read it. The displayed ranking of results may reflect commission levels, not just price or quality.

4. Personal information is shared broadly

When you enter your details on iSelect, your information is shared with partner insurers who may use it for marketing purposes beyond the immediate quote request. If you are sensitive about data sharing — particularly if you do not want multiple insurers contacting you — using iSelect means accepting this data sharing. Reading iSelect's privacy policy before entering personal details is recommended.

5. Limited information about insurer claims performance

iSelect's comparison interface focuses on price and policy features but provides limited context about insurer claims satisfaction — arguably the most important factor in car insurance quality. An insurer that is AU$80/year cheaper but takes twice as long to settle claims or disputes more claims is a worse product overall. ASIC's Moneysmart platform, the Insurance Council of Australia's data, and independent consumer reviews provide claims performance context that iSelect's interface does not.

💰 How iSelect Makes Money — And Why It Matters

Understanding iSelect's business model is essential to using it intelligently. iSelect's revenue comes from referral commissions paid by partner insurers when a consumer purchases a policy through the iSelect platform. These commissions typically range from AU$40 to AU$200 per policy sold, varying by insurer, policy type, and premium size. iSelect is required by its AFSL to disclose this commission structure — which it does in its Financial Services Guide and Product Disclosure Statement.

What Commission Means for You

The commission structure has two practical implications for consumers. First, the commission is typically factored into the premium — meaning the price you see through iSelect may be marginally higher than the same insurer's direct rate, because the insurer must cover the commission cost within their pricing. Second, iSelect has commercial incentives to feature and recommend higher-commission partners, even if ASIC regulations constrain the most egregious forms of this bias.

This does not make iSelect dishonest — it makes it a commercial business operating within regulatory constraints. But it does mean that iSelect's results should be treated as a valuable starting point for comparison, not as a comprehensive and unbiased market sweep. Supplementing iSelect results with direct quotes from the top 2–3 insurers — plus Youi and your state motoring club — gives you a more complete picture.

The Free Comparison Illusion

iSelect is free to use for consumers — but the "free" cost is paid through insurance premiums. When you buy through iSelect, a portion of your premium funds the referral commission. Whether this commission represents good value depends on whether iSelect's convenience and advice genuinely saved you more than the commission cost. For consumers who would otherwise spend 3+ hours researching individually, the time savings may well justify the cost. For savvy comparison shoppers who would check multiple sources anyway, the commission represents an unnecessary cost.

🚗 Best Car Insurance in Australia 2026 — Full Market Comparison

Beyond iSelect's panel, here is a complete picture of the best car insurance options in Australia in 2026 — including insurers that iSelect does not compare.

| # | Insurer | Best For | Avg Premium (Comprehensive) | Claims Rating | On iSelect? |

|---|---|---|---|---|---|

| 🥇 1 | Budget Direct | Cheapest comprehensive — most profiles | AU$1,020–$1,480/yr | ⭐⭐⭐⭐ | ✅ Yes |

| 🥈 2 | Youi | Low mileage · Young drivers · Pay-as-you-drive | AU$940–$1,380/yr | ⭐⭐⭐⭐⭐ | ❌ Not on iSelect |

| 🥉 3 | NRMA Insurance | NSW/ACT/QLD · Best claims service · New car replacement | AU$1,180–$1,720/yr | ⭐⭐⭐⭐⭐ | ✅ Yes |

| 4 | AAMI | Loyal customers · Multi-policy discount · Good app | AU$1,080–$1,560/yr | ⭐⭐⭐⭐ | ✅ Yes |

| 5 | RACV | Victoria · Member benefits · Agreed value | AU$1,120–$1,680/yr | ⭐⭐⭐⭐⭐ | ❌ Not on iSelect |

| 6 | Allianz | Agreed value · Premium cover · Rental car | AU$1,240–$1,840/yr | ⭐⭐⭐⭐ | ✅ Yes |

| 7 | Bingle | Absolute cheapest — basic cover only | AU$680–$980/yr | ⭐⭐⭐ | ⚠️ Sometimes |

| 8 | Woolworths Insurance | Everyday Rewards customers · Competitive pricing | AU$960–$1,420/yr | ⭐⭐⭐ | ❌ Not on iSelect |

For a complete and detailed review of all major Australian car insurance providers, see our full guide: Best Car Insurance Australia 2026 — Full Market Comparison.

💵 Average Car Insurance Costs Australia by State 2026

| State / Territory | Avg Comprehensive 2026 | Primary Cost Driver | Cheapest Insurer |

|---|---|---|---|

| New South Wales | AU$1,680/yr 🔴 | High density · CTP + comprehensive stack | Budget Direct / Youi |

| Queensland | AU$1,580/yr 🔴 | Hail risk · Flood risk · High theft zones | Bingle / Budget Direct |

| Victoria | AU$1,420/yr | Dense urban · High repair costs | RACV / Budget Direct |

| Western Australia | AU$1,380/yr | Long driving distances · Moderate risk | RAC / Budget Direct |

| South Australia | AU$1,240/yr | Lower density · Moderate risk | RAA / Budget Direct |

| Tasmania | AU$1,080/yr 🟢 | Low density · Lower risk | RACT / Budget Direct |

| ACT | AU$1,320/yr | High-income demographic · Higher-value vehicles | NRMA / Budget Direct |

| Northern Territory | AU$1,820/yr 🔴 | Remote driving · Limited insurer competition | AAMI / NRMA |

Key Factors That Affect Your Individual Premium

Beyond state averages, your specific premium reflects your individual risk profile. The factors Australian insurers weight most heavily are: your vehicle's make, model, and year (repair cost, theft rate, safety ratings); your age and driving experience — under-25 drivers pay 40–120% more than 30–50 year olds; your postcode (insurers have granular suburb-level risk data); your annual mileage (lower mileage = lower risk = lower premium with usage-sensitive insurers like Youi); your claims history over the past 3–5 years; and the type of cover you select (comprehensive, third party fire and theft, or third party property only).

🔄 Best iSelect Alternatives for Car Insurance in Australia 2026

Compare the Market Australia

Compare the Market is iSelect's primary direct competitor in the Australian comparison market. It covers a different but partially overlapping insurer panel and includes some providers not available on iSelect. Running both iSelect and Compare the Market simultaneously — entering your details on each — takes approximately 12–15 minutes total and typically reveals 3–5 quote differences that help you identify the full market range. Compare the Market is most useful as the second platform in a two-platform comparison strategy.

Finder.com.au

Finder is a broader financial comparison platform that covers car insurance alongside credit cards, home loans, and other financial products. Its car insurance comparison panel partially overlaps with iSelect's but includes some unique partners. Finder's editorial content and expert reviews provide additional context about insurer quality that iSelect's interface does not. For consumers who want both price comparison and qualitative research in one platform, Finder is the strongest single-site alternative.

Direct Quotes — The Non-Negotiable Step

Regardless of which comparison platform you use, always get direct quotes from Youi and your state motoring club before finalising your decision. Youi is not on any major comparison platform and consistently offers competitive pricing — particularly for low-mileage drivers and regional motorists. Your state motoring club (RACV in Victoria, RAA in South Australia, RAC in Western Australia, NRMA in NSW/ACT, RACT in Tasmania, AANT in NT) often offers competitive rates with member benefits that no comparison site can replicate. Checking these two direct sources typically adds 15 minutes but can reveal savings of AU$150–$400/year.

ASIC Moneysmart

The Australian Securities and Investments Commission's Moneysmart platform provides free, non-commercial car insurance guidance including a premium calculator, guidance on choosing the right cover type, and information about your rights in a claims dispute. Moneysmart does not sell insurance and receives no commission — making it the most neutral information source available for Australian consumers. It is the right first stop before any commercial comparison platform.

🎯 How to Use iSelect Correctly — Expert Strategy for 2026

Given iSelect's strengths and limitations, here is the optimal strategy for using it as part of a comprehensive car insurance comparison:

Step 1 — Use ASIC Moneysmart first (10 minutes)

Before entering your details on any commercial platform, use ASIC's Moneysmart guide to determine what type of cover you actually need — comprehensive, third party fire and theft, or third party property only. Many Australians pay for comprehensive cover on vehicles whose market value does not justify the comprehensive premium. Moneysmart's tool helps you make this assessment objectively before you start comparing premiums.

Step 2 — Run iSelect for panel coverage (8 minutes)

Enter your details on iSelect and note the top three results. Screenshot or copy the premium, excess, and key feature summary for each. Do not purchase yet. This gives you the reference range for the majority of the Australian car insurance market that iSelect covers.

Step 3 — Run Compare the Market simultaneously (8 minutes)

Enter the same details on Compare the Market. Compare the top results with your iSelect shortlist. Note any insurers that appear on Compare the Market but not iSelect — these represent market segments iSelect missed.

Step 4 — Get a Youi direct quote (5 minutes)

Visit youi.com.au and get a direct quote. Youi's pricing model is based on personalised risk assessment — they ask more detailed questions than most comparison platforms to generate a more precisely calibrated premium. For some profiles (low mileage, regional drivers, over-30s with clean records), Youi's quote will be significantly lower than anything on iSelect or Compare the Market.

Step 5 — Check your state motoring club (5 minutes)

Get a quote from your state's motoring club — RACV (VIC), RAA (SA), RAC (WA), NRMA (NSW/ACT), RACT (TAS), AANT (NT). If you are already a member, the discount applies automatically. If you are not a member, calculate whether the membership cost plus the insurance premium is lower than your best comparison site result.

Step 6 — Choose and negotiate (5 minutes)

Armed with quotes from 4–6 sources, you now have genuine market pricing. Contact your preferred insurer directly and ask whether they can match or beat your lowest quote — even when going direct to an iSelect partner, many insurers have discretion to adjust pricing for direct customers who mention a competing quote. Purchase directly from the insurer's website to potentially avoid the comparison platform commission markup.

💡 How to Get the Cheapest Car Insurance in Australia 2026

1. Choose market value over agreed value for older vehicles

Agreed value cover (where the insurer pays a fixed, pre-agreed amount if your car is written off) costs 15–25% more than market value cover (where the insurer pays what your car was worth at the time of loss). For vehicles older than 5–7 years, market value cover is almost always the more cost-effective choice because the agreed value premium difference exceeds the settlement difference in most cases. For new or near-new vehicles where market value drops sharply, agreed value provides meaningful protection — but review annually as the premium differential may not justify the benefit as the vehicle ages.

2. Increase your excess to reduce your premium

Choosing a higher voluntary excess — the amount you contribute toward any claim — directly reduces your premium. Moving from a AU$500 standard excess to a AU$1,500 voluntary excess typically reduces comprehensive cover premiums by 12–22%. For drivers who have not made a claim in 5+ years, the higher excess represents good expected-value economics: the premium savings over 5 years typically exceed the excess differential on a single claim. Do not choose an excess level you could not afford to pay in a genuine emergency.

3. Use Youi's pay-as-you-drive for low-mileage savings

Youi's KiloMeter insurance product prices your premium based on your actual annual mileage — drivers who cover under 10,000 km/year can save 20–35% versus standard annual comprehensive cover. This product is particularly valuable for: remote workers who rarely commute, retirees who drive primarily for leisure, urban residents with good public transport access, and second-vehicle owners in multi-car households. Youi is not on iSelect — you must quote directly at youi.com.au.

4. Bundle home and car insurance with the same insurer

Most Australian insurers offer multi-policy discounts of 5–15% when you hold both home and car insurance with them. NRMA, AAMI, Allianz, and Budget Direct all offer meaningful bundle discounts. The calculation is straightforward: if bundling saves 10% on a AU$1,400 car policy, that is AU$140/year — potentially more than any comparison platform quote difference. Always request a bundle quote from your current home insurer before switching car insurers on price alone.

5. Review and compare every renewal — never auto-renew

Australian insurers routinely offer more competitive rates to new customers than to renewing policyholders — the loyalty penalty is real and documented. ASIC data from 2025 found that consumers who had not compared in the previous two years were paying an average of AU$280 more than comparable new customers at the same insurer. Never auto-renew without first running a comparison — even if your insurer's renewal letter looks reasonable, the market may have moved significantly since your last review.

❓ Frequently Asked Questions — iSelect Car Insurance Australia 2026

Is iSelect a legitimate car insurance comparison site?

Yes — iSelect is a legitimate, ASIC-regulated financial services comparison company holding an Australian Financial Services Licence (AFSL). It is publicly listed on the ASX (ticker: ISU) and must comply with Australian consumer protection laws. However, legitimate does not mean comprehensive or unbiased. iSelect earns referral commissions from partner insurers, covers only a portion of the Australian car insurance market (missing major providers like Youi, state motoring clubs, and Woolworths Insurance), and may not always surface the cheapest available policy for your specific profile. Use it as one of several comparison tools, not as your only source.

Does iSelect cover all car insurance companies in Australia?

No — iSelect compares only its panel of partner insurers, which covers approximately 60–70% of the Australian car insurance market by premium volume. Notable insurers not on the iSelect panel include Youi (consistently one of the cheapest for low-mileage and young drivers), the state motoring clubs (RACV, RAA, RAC, NRMA, RACT, AANT), Woolworths Insurance, Coles Insurance, and Huddle. For a complete market comparison, supplement iSelect with a direct Youi quote and a quote from your state motoring club at minimum.

Is it cheaper to buy car insurance through iSelect or direct?

It depends on the insurer. Some insurers price identically through comparison platforms and direct channels. Others offer slightly lower rates direct — because buying direct avoids the referral commission that the insurer would otherwise pay to iSelect. As a general rule, after finding your best iSelect result, visit the winning insurer's own website and request a direct quote for identical cover. If the direct quote is lower, purchase direct. If identical, it makes no difference where you purchase. Never pay more than the iSelect price when buying direct — there is no logical reason to do so.

What is the cheapest car insurance in Australia in 2026?

The cheapest car insurance in Australia in 2026 depends on your state, vehicle, age, and driving history — but Budget Direct and Youi consistently appear as the most price-competitive options for comprehensive cover. Bingle (a Suncorp brand) offers the cheapest absolute premiums but with more limited coverage. For low-mileage drivers, Youi's KiloMeter pay-as-you-drive product can be the cheapest overall option — but Youi is not available on iSelect's comparison platform, requiring a direct quote at youi.com.au. Average comprehensive premiums nationally range from AU$940 to AU$1,680 depending on state and profile.

How much does car insurance cost in Australia in 2026?

Average comprehensive car insurance in Australia costs approximately AU$1,020–$1,680 per year in 2026, depending on state. NSW and Queensland are the most expensive states (AU$1,580–$1,680 average) due to CTP structure, hail risk, and litigation rates. Tasmania and South Australia are the cheapest (AU$1,080–$1,240 average). Individual premiums vary significantly based on your vehicle, age, postcode, annual mileage, and claims history. Young drivers under 25 typically pay 40–120% more than the state average. The most cost-effective strategy is comparing at least 3–4 quotes from different sources, including direct quotes from Youi and your state motoring club.

Should I use iSelect, Compare the Market, or Finder for car insurance?

Use all three — plus direct quotes. Each comparison platform covers a partially different panel of insurers, meaning the cheapest result on iSelect may not be the cheapest on Compare the Market or Finder. Running all three platforms takes approximately 20–25 minutes total and reveals the complete range of comparison-site pricing. But the most important step is getting direct quotes from Youi and your state motoring club — both of which are absent from all major comparison platforms but frequently offer the market's most competitive pricing for specific driver profiles. The optimal strategy: iSelect + Compare the Market + Finder + Youi direct + motoring club direct = complete market sweep.

✅ Final Verdict — iSelect Car Insurance Australia 2026

iSelect is a useful, legitimate, and time-efficient starting point for Australian car insurance comparison — but not a complete market sweep. Its strengths are speed, convenience, side-by-side policy comparison, and access to human advisors for complex situations. Its critical limitations are partial market coverage (missing Youi, motoring clubs, and others), commission-influenced structure, and the absence of substantive claims performance data.

The right approach: use iSelect for your initial comparison, supplement with Compare the Market and Finder for additional coverage, always check Youi and your state motoring club directly, and compare every renewal rather than auto-renewing. Australian drivers who follow this multi-platform strategy consistently find premiums AU$200–$500 lower than single-platform comparison shoppers. For our complete guide to the best car insurance options in Australia — including detailed insurer reviews — see our full article on Best Car Insurance Australia 2026. For international car insurance comparisons, see our guides on best auto insurance USA 2026 and Progressive vs Geico vs State Farm vs Allstate.

Disclaimer: This article is for informational purposes only and does not constitute financial or insurance advice. Premium ranges are approximate averages based on publicly available Australian market data — individual quotes vary significantly. iSelect panel coverage and partner relationships may change. Always read the Product Disclosure Statement before purchasing any insurance policy. Nexuora is not affiliated with iSelect or any insurer mentioned. Updated April 20, 2026.

Ahmada Ndao is a financial research analyst and independent journalist

specializing in US consumer finance, legal rights, and insurance markets.

With over 5 years covering American financial products, he has helped

thousands of readers navigate complex insurance decisions, find the right

legal representation, and optimize their credit strategies. His research

methodology combines primary data analysis, direct outreach to industry

professionals, and continuous monitoring of federal regulatory changes.

Ahmada’s work has been cited by financial communities across the US and

reviewed by licensed attorneys and insurance professionals for accuracy.