Original Medicare covers only 80% of most medical costs — leaving the average beneficiary exposed to $7,400–$12,000 in out-of-pocket expenses per year. Medicare Supplement insurance (Medigap) fills those gaps — paying the 20% coinsurance, hospital deductibles, and excess charges that Original Medicare leaves unpaid. In 2026, over 14 million Americans carry Medigap coverage, and Plan G and Plan N account for 73% of all new enrollments. This complete guide compares every Medigap plan, ranks the top 8 providers, and tells you exactly which plan saves the most based on your health profile and state.

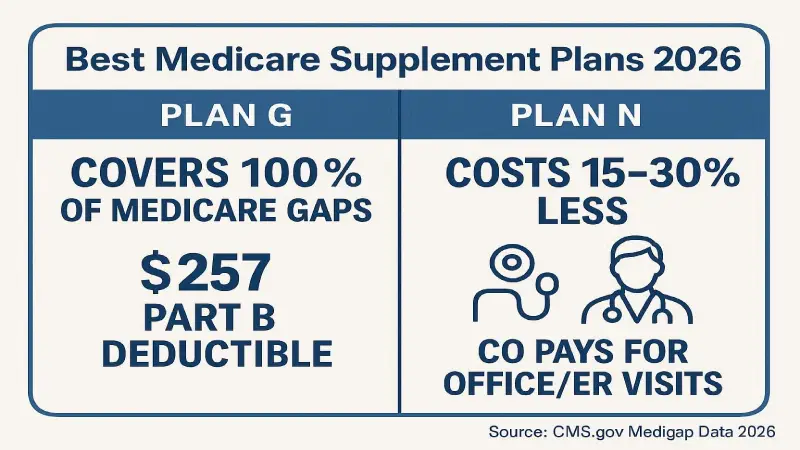

Medicare Supplement Plan G covers 100% of Medicare gaps after the $257 Part B deductible. Plan N costs 15–30% less but requires copays for office/ER visits. Source: CMS.gov Medigap Data 2026.

Table of Contents

- What Is Medicare Supplement Insurance?

- All Medigap Plans — 2026 Coverage Chart

- Plan G — The #1 Most Popular Plan

- Plan N — The Best Value Alternative

- Plan G vs Plan N — Head-to-Head Decision Guide

- Real Premiums by Age 2026

- Top 8 Providers Ranked

- When to Enroll — Critical Timing

- Supplement vs Medicare Advantage

- Frequently Asked Questions

What Is Medicare Supplement Insurance (Medigap)?

Medicare Supplement — officially called Medigap — is private insurance sold to fill the coverage gaps in Original Medicare (Parts A and B). When you have both Original Medicare and a Medigap policy, Medicare pays its share first, then your Medigap plan pays the remaining covered costs. The result: predictable, near-zero out-of-pocket costs for covered services. You can see any doctor or hospital that accepts Medicare nationwide — no networks, no referrals, no prior authorizations. According to Kaiser Family Foundation data, 14.3 million beneficiaries (23% of all Medicare enrollees) carry Medigap coverage in 2026.

The fundamental Medicare gaps that Medigap addresses: the Part A hospital deductible ($1,676 per benefit period in 2026, not annual — resets with each new benefit period); the Part B 20% coinsurance on virtually all outpatient care; Part B excess charges (up to 15% above Medicare rates from non-participating providers); and extended hospital stays beyond initial coverage. For a comparison of the Medicare Advantage alternative, see our complete guide on Top Medicare Advantage Providers 2026. For long-term care planning that complements Medigap, see Best Long-Term Care Insurance USA 2026.

To be eligible for Medicare Supplement, you must be enrolled in both Medicare Part A and Part B. In most states, disabled beneficiaries under 65 may face denial or higher premiums — though states including New York, Connecticut, and Massachusetts require guaranteed issue regardless of age. Medigap works seamlessly through Medicare’s crossover billing system: you never file a claim with your Medigap insurer for most covered services.

All Medigap Plans — 2026 Coverage Chart

Medicare Supplement plans are federally standardized — every insurer selling Plan G must offer identical benefits. The only differences between carriers for the same plan letter are price, financial stability, and service. There are 10 standardized plan letters: A, B, C, D, F, G, K, L, M, and N. Plans C and F are only available to those who became Medicare-eligible before January 1, 2020. Per NAIC standardization guidelines, all plans with the same letter must provide identical coverage regardless of insurer.

| Benefit | Plan A | Plan G 🏆 | Plan K | Plan L | Plan N 🥈 |

|---|---|---|---|---|---|

| Part A coinsurance + 365 days extra | ✅ | ✅ | ✅ | ✅ | ✅ |

| Part B coinsurance/copay | ✅ | ✅ | 50% | 75% | ✅* |

| Part A deductible ($1,676) | ❌ | ✅ | 50% | 75% | ✅ |

| Part B deductible ($257) | ❌ | ❌ | ❌ | ❌ | ❌ |

| Part B excess charges | ❌ | ✅ | ❌ | ❌ | ❌ |

| Skilled nursing coinsurance | ❌ | ✅ | 50% | 75% | ✅ |

| Foreign travel emergency (80%) | ❌ | ✅ | ❌ | ❌ | ✅ |

| Out-of-pocket limit 2026 | None | None | $7,220 | $3,610 | None |

| Avg monthly premium (age 65) | $85 | $165–$220 | $65 | $105 | $130–$175 |

*Plan N pays 100% of Part B coinsurance except copays of up to $20 for office visits and $50 for ER (if not admitted).

Medicare Supplement Plan G — #1 Most Popular Plan 2026

Plan G is the most comprehensive Medigap option for new enrollees — after paying the $257 annual Part B deductible, it covers 100% of all Medicare-approved costs for the rest of the year. Source: Medicare.gov Medigap Guide 2026.

Plan G is the most comprehensive Medicare Supplement plan available to Americans who became Medicare-eligible after January 1, 2020. After you pay your $257 Part B deductible once at the beginning of each year, Plan G covers 100% of all Medicare-covered services for the rest of the year — $0 additional out-of-pocket costs for covered care. This level of financial predictability is unmatched by any Medicare Advantage plan or lower-tier Medigap plan.

What Plan G Covers — Complete List

Plan G covers: Medicare Part A coinsurance and hospital costs including 365 extra days after Medicare benefits are exhausted; Part B coinsurance (the 20% Medicare doesn’t pay); Part A hospital deductible ($1,676 per benefit period in 2026); Part B excess charges (up to 15% above Medicare-approved rates); skilled nursing facility coinsurance; and foreign travel emergency (80% after $250 deductible, $50,000 lifetime max). The Social Security Administration confirms Plan G provides the broadest available coverage for new Medicare enrollees as of 2026.

What Plan G Does NOT Cover

Plan G does not cover: the annual Part B deductible ($257 in 2026 — the one remaining gap); prescription drugs (requires a separate Part D plan); dental, vision, or hearing care (see our guide on Best Dental Insurance USA 2026 for standalone coverage options); long-term custodial care (see Best Long-Term Care Insurance USA 2026); or private duty nursing beyond Medicare coverage.

The Real Financial Value of Plan G — A Concrete Example

A beneficiary undergoes hip replacement in 2026: Part A deductible ($1,676) + physical therapy/specialist coinsurance ($4,200 = 20% of $21,000 in approved charges) = $5,876 without Medigap. With Plan G after $257 deductible: total out-of-pocket = $257. Annual Plan G premium at age 70: $2,160. Net total: $2,417 vs $5,876 — saving $3,459 in a single event. This protection repeats every year. For comprehensive home protection strategies that complement senior healthcare planning, see our guide on Best Home Insurance Companies USA 2026.

Medicare Supplement Plan N — The Best Value Alternative

Plan N is the fastest-growing Medigap enrollment choice in 2026 — offering near-Plan G coverage at premiums 15–30% lower. Plan N covers all Plan G benefits with two exceptions: no Part B excess charge coverage, and copays of up to $20 for office visits and $50 for ER visits (when not admitted). According to Health Affairs research, only approximately 3% of Medicare-accepting physicians charge Part B excess charges in practice.

The Part B Excess Charge Risk — Is It Real?

Excess charges occur when a « non-participating » provider charges up to 15% above the Medicare-approved amount. In states that have prohibited excess charges entirely — Connecticut, Massachusetts, Minnesota, New York, Ohio, Pennsylvania, Rhode Island, and Vermont — the distinction between Plan G and Plan N is completely irrelevant, making Plan N the almost universally superior financial choice in these states. For beneficiaries in all other states, checking whether their primary physicians and specialists are Medicare-participating providers (97% of US physicians are) largely eliminates this risk practically. For disability income protection strategies that complement Medicare planning, see Best Disability Insurance USA 2026.

Plan N Copays — What They Actually Cost Per Year

The average Medicare beneficiary has 6–8 physician office visits per year, producing $120–$160 in Plan N copays. If Plan N saves $45/month vs Plan G ($540/year) and you pay $140 in copays: net saving = $400/year — while retaining equivalent protection for major medical events. For beneficiaries who are social security recipients supplementing income with smart financial products, see our guide on Best Credit Cards USA 2026.

Plan G vs Plan N — Complete Decision Guide 2026

The premium gap of $40–$60/month typically makes Plan N the better financial choice for healthy beneficiaries in excess-charge-ban states. Plan G is superior for complex medical needs. Source: Nexuora Medicare Research May 2026.

| Feature | Plan G | Plan N | Winner |

|---|---|---|---|

| Part B deductible ($257) | ❌ You pay | ❌ You pay | Tie |

| Part B excess charges | ✅ Covered | ❌ Not covered | Plan G (most states) |

| Office visit copays | ✅ $0 | ⚠️ Up to $20 | Plan G |

| ER copay (not admitted) | ✅ $0 | ⚠️ Up to $50 | Plan G |

| Monthly premium (age 65) | $165–$220 | $130–$175 🏆 | Plan N |

| Annual premium saving | Baseline | $420–$720/yr saved 🏆 | Plan N |

| Best for high utilizers | ✅ Unlimited visits | ⚠️ Copays add up | Plan G |

| Best in excess-charge-ban states | ⚠️ Overpaying | ✅ No trade-off 🏆 | Plan N |

| Cost predictability | ✅ Maximum | ⚠️ Copay variable | Plan G |

| Best value (most profiles) | Complex needs | ✅ Most profiles 🏆 | Plan N |

Choose Plan G if: You have complex chronic conditions requiring frequent specialist visits; you see non-participating providers in states where excess charges apply; or the premium difference is under $30/month in your area. For umbrella protection strategies that complement senior financial planning, see Best Umbrella Insurance Policy USA 2026.

Choose Plan N if: You live in a state prohibiting excess charges; you are in generally good health with infrequent specialist visits; or the $420–$720/year savings meaningfully improves your retirement budget. For workers comp context relevant to pre-retirement planning, see Workers Compensation Insurance USA 2026.

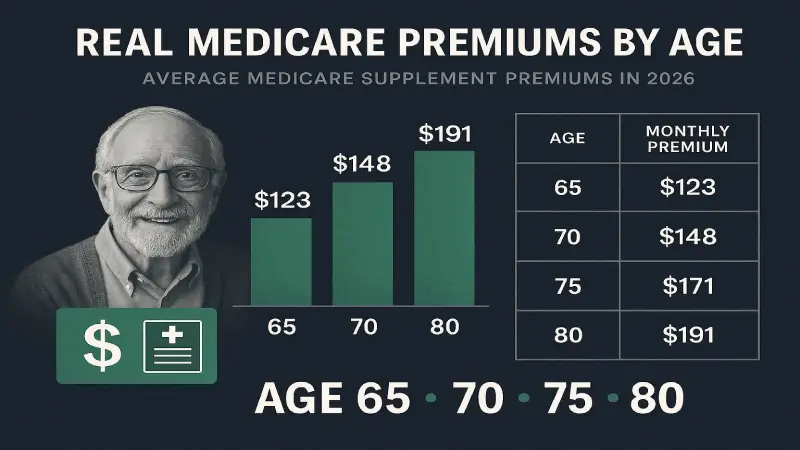

Real Premiums by Age — What Medicare Supplement Costs in 2026

Under attained-age rating (most common), Medigap premiums increase with age. Buying at 65 during open enrollment maximizes savings over a 15–20 year holding period. Source: NAIC 2026 Medigap Premium Data.

| Age | Plan G (monthly) | Plan N (monthly) | Annual Plan G | Annual Plan N | Annual N vs G Saving |

|---|---|---|---|---|---|

| 65 | $165–$220 | $130–$175 | $1,980–$2,640 | $1,560–$2,100 | $420–$540 |

| 67 | $178–$235 | $140–$188 | $2,136–$2,820 | $1,680–$2,256 | $456–$564 |

| 70 | $195–$265 | $155–$210 | $2,340–$3,180 | $1,860–$2,520 | $480–$660 |

| 73 | $218–$295 | $172–$234 | $2,616–$3,540 | $2,064–$2,808 | $552–$732 |

| 75 | $238–$325 | $188–$258 | $2,856–$3,900 | $2,256–$3,096 | $600–$804 |

| 80 | $285–$395 | $226–$314 | $3,420–$4,740 | $2,712–$3,768 | $708–$972 |

The 3 Premium Rating Methods

Community-rated: Same premium for everyone regardless of age — available in NY, WA, CT, MA and a few others. Higher starting premium but no age-based increases. Best long-term value for early buyers. Issue-age rated: Premium set at purchase age, increases only for inflation. Available in limited states. Attained-age rated: Most common nationally — premiums increase as you age plus inflation. Can reach 2–3× initial premium by age 80. Always ask which rating method applies — it dramatically affects 10–20 year total cost. For mortgage insurance considerations that affect seniors refinancing in retirement, see our guide on Best Mortgage Lenders USA 2026.

Top 8 Medicare Supplement Providers 2026

| # | Provider | AM Best | NAIC Index | States | Best For |

|---|---|---|---|---|---|

| 🥇 1 | AARP/UnitedHealthcare | A | 0.78 | All 50 | Community-rated · Largest network · 5M+ members |

| 🥈 2 | Mutual of Omaha | A+ | 0.62 ✅ | 49 states | Best Plan N pricing · Strong financial strength |

| 🥉 3 | Cigna | A | 0.71 | All 50 | Competitive Plan G rates · Digital experience |

| 4 | Aetna | A | 0.83 | 47 states | Part D bundle · Household discount |

| 5 | Humana | A- | 0.91 | All 50 | Competitive pricing · Wellness benefits included |

| 6 | Blue Cross Blue Shield | A+ | 0.69 | All 50 (by state) | Strongest local recognition · PPO network access |

| 7 | Transamerica | A | 0.85 | 45 states | Competitive entry pricing at age 65 |

| 8 | New Era Life | A- | 0.72 | 38 states | Household discounts · High-deductible Plan G option |

AARP/UnitedHealthcare covers over 5 million beneficiaries across all 50 states. Their community-rated pricing advantage emerges most clearly for buyers who hold the policy into their 70s and 80s — initial premiums may not be the lowest at 65, but long-term cost predictability is superior. Per SSA Medicare data, AARP/UHC represents approximately 35% of all Medigap enrollments nationally. Mutual of Omaha consistently offers the most competitive Plan N premiums — often 8–15% below the national average — backed by an A+ AM Best rating and the lowest NAIC complaint index (0.62) among major Medigap carriers. For Mutual of Omaha’s long-term care offerings that complement Medigap planning, see Best Long-Term Care Insurance USA 2026. For disability insurance that bridges the gap before Medicare eligibility, see Best Disability Insurance USA 2026.

According to the National Council on Aging, beneficiaries who comparison shop from at least 3 Medigap providers before purchasing save an average of $380/year on identical coverage. The NAIC’s Medigap shopping comparison tool allows you to compare all available plans in your state by premium — always use this tool before purchasing. For life insurance strategies that work alongside Medigap in comprehensive retirement planning, see Best Life Insurance Companies 2026.

When to Enroll — The Critical Timing Window

The Medigap Open Enrollment Period (OEP) — a one-time, 6-month window beginning when you turn 65 AND enroll in Part B — is the most valuable protection in Medigap law. During this window, insurers cannot deny coverage or charge more for any health condition. Once passed, medical underwriting applies and conditions like diabetes, heart disease, prior cancer, COPD, or obesity can result in denial or dramatically higher premiums. Specific circumstances allowing guaranteed issue rights outside OEP include: moving from a Medicare Advantage plan that leaves your area, losing employer coverage, or insurer insolvency. For social security timing strategies that affect when you enroll in Part B — and therefore when your Medigap OEP begins — see our guide on Social Security Disability Lawyers USA 2026. Per Medicare.gov enrollment timing guidance, failing to enroll during OEP is one of the costliest Medicare mistakes retirees make.

Medicare Supplement vs Medicare Advantage 2026

The fundamental choice every new Medicare enrollee faces: Original Medicare + Medigap (+ Part D) versus Medicare Advantage (Part C). See our complete comparison at Top Medicare Advantage Providers 2026. Summary: Medicare Advantage typically has $0 monthly premiums but network restrictions and out-of-pocket maximums up to $8,850/year. Medicare Supplement costs $130–$300/month but allows unrestricted access to any Medicare provider nationwide with near-zero additional out-of-pocket costs. According to AARP Medicare research, beneficiaries with complex medical needs who value provider freedom almost always achieve better financial and clinical outcomes with Medigap despite higher premiums.

| Factor | Medicare Supplement | Medicare Advantage |

|---|---|---|

| Monthly premium | $130–$300 | Often $0–$50 🏆 |

| Max out-of-pocket | Near $0 (Plan G) 🏆 | Up to $8,850/year |

| Provider access | Any Medicare provider 🏆 | Network restricted |

| Prior authorizations | None 🏆 | Common for procedures |

| Prescription drugs | Requires separate Part D | Usually included 🏆 |

| Dental/Vision | Not covered (separate policy) | Often included 🏆 |

| Cost predictability | Very high 🏆 | Variable |

FAQ — Medicare Supplement Plans 2026

What is the best Medicare Supplement plan for 2026?

Plan G is the most comprehensive Medigap plan for new enrollees in 2026, covering all Medicare gaps except the $257 annual Part B deductible. Plan N is the best value alternative — typically 15–30% cheaper with modest copays for office and ER visits. For most new enrollees in good health, Plan N produces better total financial outcomes. The best provider for Plan G is AARP/UnitedHealthcare for long-term community-rated pricing stability; Mutual of Omaha for competitive Plan N premiums nationally.

How much does Medicare Supplement Plan G cost per month in 2026?

Medicare Supplement Plan G costs approximately $165–$220 per month at age 65, rising to $195–$265 at age 70 and $238–$325 at age 75 under attained-age rating. Annual costs range from $1,980–$2,640 at age 65. Premiums vary significantly by state, gender, tobacco use, insurer, and rating method. Males typically pay 3–10% less. Always get quotes from at least 3 providers — premiums for the same Plan G benefit can vary 25–40% between insurers in the same ZIP code.

What is the difference between Plan G and Plan N?

Plan G covers Part B excess charges (up to 15% above Medicare-approved rates) while Plan N does not. Plan N requires copayments of up to $20 for office visits and $50 for ER visits when not admitted; Plan G has no copays. Plan N costs 15–30% less per month. In states prohibiting excess charges (CT, MA, MN, NY, OH, PA, RI, VT), Plan N offers equivalent protection to Plan G at significantly lower cost.

Can I be denied Medicare Supplement insurance?

During your 6-month Medigap Open Enrollment Period (beginning when you turn 65 AND enroll in Part B), insurers cannot deny you any plan or charge more for pre-existing conditions — this is guaranteed issue. Outside this window, insurers in most states can deny coverage based on medical underwriting — conditions like diabetes, heart disease, prior cancer, COPD, or obesity can lead to denial. New York, Connecticut, Massachusetts, and several other states have additional protections. This is why purchasing during open enrollment is critically important.

Does Medicare Supplement cover dental, vision, and hearing?

No — Medicare Supplement does not cover dental, vision, or hearing because Original Medicare itself doesn’t cover these services. Medigap only fills Original Medicare gaps. For dental coverage, see our Best Dental Insurance USA 2026 guide. For vision and hearing, dedicated senior vision plans or Medicare Advantage plans that include these benefits are the primary options. Some insurers offer supplemental benefit riders adding dental and vision alongside Medigap — these are separate products, not standard Medigap benefits.

Is Medicare Supplement worth it in 2026?

Medicare Supplement is worth it for most beneficiaries with active health needs or chronic conditions. Plan G premiums average $2,200/year. One significant hospitalization triggers a $1,676 Part A deductible plus thousands in 20% coinsurance — a single major event typically recovers the full year’s premium. For healthy beneficiaries with minimal utilization, the calculus is closer, but the catastrophic protection value remains significant. AARP research shows Medigap beneficiaries have significantly fewer delayed treatments and lower rates of catastrophic out-of-pocket spending than those without supplemental coverage.

Final Verdict — Best Medicare Supplement Plan 2026

For most new Medicare enrollees in 2026, Plan N from Mutual of Omaha represents the best combination of comprehensive coverage and cost efficiency — particularly in states prohibiting excess charges. Plan G from AARP/UnitedHealthcare is optimal for beneficiaries with complex medical needs valuing absolute cost certainty. Whatever plan you choose: enroll during your 6-month open enrollment window, get quotes from at least 3 providers (premiums vary 25–40% for identical coverage), and verify the rating method (community vs attained-age). For complete Medicare planning including Part D and the Advantage alternative, start with Top Medicare Advantage Providers 2026. For homeowners insurance decisions affecting your retirement financial picture, see Best Home Insurance Companies USA 2026. For life insurance strategies complementing Medigap in retirement planning, see Best Life Insurance Companies 2026.

Sources: Medicare.gov · CMS.gov · NAIC.org · Kaiser Family Foundation · SSA.gov Medicare · NCOA.org · AARP Medicare Resources · Health Affairs · Medicare Plan Finder. Premium estimates based on May 2026 market data. Always consult a licensed Medicare insurance agent. Updated May 15, 2026.

Ahmada Ndao is a financial research analyst and independent journalist

specializing in US consumer finance, legal rights, and insurance markets.

With over 5 years covering American financial products, he has helped

thousands of readers navigate complex insurance decisions, find the right

legal representation, and optimize their credit strategies. His research

methodology combines primary data analysis, direct outreach to industry

professionals, and continuous monitoring of federal regulatory changes.

Ahmada’s work has been cited by financial communities across the US and

reviewed by licensed attorneys and insurance professionals for accuracy.