The difference between the best and worst credit card for your spending profile can exceed $1,200 in annual value. A frequent traveler using the wrong cashback card leaves hundreds of dollars in transfer bonuses on the table. Someone carrying credit card debt paying 21%+ APR who hasn’t transferred to a 0% intro card is throwing money away every month. The US credit card market in 2026 has never been more competitive — welcome bonuses exceed $1,000 in value on premium cards, airport lounge access has shifted dramatically, and the points landscape has changed with new valuations from The Points Guy (Chase Ultimate Rewards at 2.05¢/point, Citi ThankYou at 1.9¢/point in May 2026). This guide cuts through 200+ cards to identify the 8 best for distinct profiles — with real sign-up bonus values, annual fee break-even calculations, and head-to-head comparisons between the most-searched cards.

The best credit card in 2026 depends entirely on your profile: frequent travelers maximize Chase or Amex premium cards; cashback seekers get the most from Citi Double Cash or Wells Fargo Active Cash; debt consolidators need Wells Fargo Reflect’s 21-month 0% APR. Source: CNBC Select, The Points Guy, NerdWallet, Nexuora Research May 2026.

Table of Contents

- Quick Pick — Best Card by Profile

- Best Travel Credit Cards 2026

- Best Cashback Credit Cards 2026

- Best Balance Transfer Cards 2026

- Best No Annual Fee Cards 2026

- Head-to-Head: Chase Sapphire Preferred vs Amex Gold vs Capital One Venture X

- Points Value Guide — What Your Rewards Are Actually Worth

- Which Card Is Right for You?

- Frequently Asked Questions

Quick Pick — Best Credit Card by Profile 2026

| Your Profile | Best Card | Annual Fee | Sign-Up Bonus Value |

|---|---|---|---|

| Best overall travel card | Chase Sapphire Preferred | $95 | ~$750 in travel |

| Best premium travel card | Capital One Venture X | $395 | Up to $1,000+ |

| Best for earning points fast | American Express Gold | $325 | ~$1,200+ |

| Best lounge access + family guests | Chase Sapphire Reserve | $550 | ~$1,500+ |

| Best simple cashback | Citi Double Cash | $0 | None (ongoing 2%) |

| Best flat-rate cashback | Wells Fargo Active Cash | $0 | $200 after $500 spend |

| Best balance transfer / 0% APR | Wells Fargo Reflect | $0 | 21 months 0% APR |

| Best grocery + dining rewards | Amex Gold Card | $325 | 4x groceries, 4x dining |

Best Travel Credit Cards USA 2026

Chase Sapphire Reserve leads for family travelers with two free lounge guests. Capital One Venture X leads for value per annual fee dollar. Amex Platinum leads for global lounge footprint. Source: The Points Guy May 2026 Valuations; Nexuora Research.

1 — Chase Sapphire Preferred: Best Entry-Level Travel Card

The Chase Sapphire Preferred remains the most recommended travel card in America for a reason: it delivers serious value at a $95 annual fee that most travelers recover in the first 60 days. The current sign-up bonus of 60,000 points after $4,000 spend in 3 months is worth approximately $750 in travel via Chase Travel — or up to $1,230 when transferred to airline and hotel partners at TPG’s May 2026 valuation of 2.05¢/point. Ongoing rewards: 5x on Chase Travel bookings, 3x on dining, 3x on online groceries, 3x on select streaming services, 2x on all other travel. The annual 10% points bonus on every card anniversary adds meaningful compounding value over time. The $50 annual hotel credit through Chase Travel effectively reduces the annual fee to $45 for travelers who use it.

2 — Capital One Venture X: Best Premium Card for Value

The Capital One Venture X at $395/year is the best value among premium travel cards — a statement supported by The Points Guy naming it the best flat-rate premium card in their May 2026 rankings. The math: a $300 annual travel credit through Capital One Travel plus 10,000 bonus miles on each card anniversary (worth ~$200 in travel) adds up to $500 in guaranteed annual value against a $395 fee — meaning the card effectively pays you $105 before you earn a single rewards point. The ongoing earning rate of 2x miles on everything (with 5x on hotels and 10x on car rentals through Capital One Travel) builds miles at a consistent pace without category tracking. 2026 lounge change note: Capital One began charging guest fees at its lounges on February 1, 2026 — which reduces its advantage for cardholders who regularly bring companions.

3 — American Express Platinum: Best for Lounge Access Volume

At $895/year (raised in 2026), the Amex Platinum is now harder to justify without maximizing its credits — but for heavy travelers who do maximize them, it delivers over $1,500 in annual value. Credits include $200 airline fee credit, $200 hotel credit, $240 digital entertainment credit, $189 CLEAR Plus credit, $155 Walmart+ credit, and $100 Global Entry/TSA PreCheck credit. The lounge access includes Amex Centurion Lounges (best premium lounges in airports that have them), Priority Pass Select, and Delta Sky Club when flying Delta or a partner. Earning: 5x on flights booked directly with airlines or Amex Travel, 5x on prepaid hotels via Amex Travel. Guest fee change: Amex began charging for additional guests at Centurion Lounges — reducing its family-friendliness versus Chase Sapphire Reserve.

4 — Chase Sapphire Reserve: Best for Families + Dining

The Chase Sapphire Reserve at $550/year is more expensive than the Sapphire Preferred but delivers a broader credit set and the most family-friendly lounge policy in 2026. Sapphire Lounges are currently the only major issuer lounges that include two free guests — making the Reserve uniquely valuable for travelers with a partner or children. Earning rates: 8x on Chase Travel portal bookings, 4x on flights and hotels booked direct, 3x on dining worldwide. TPG values Chase Ultimate Rewards at 2.05¢/point in May 2026. The $300 annual travel credit (applied automatically to any travel purchase) effectively reduces the net annual fee to $250.

Best Cashback Credit Cards USA 2026

Citi Double Cash leads for simplicity with 2% on everything. Amex Gold delivers the highest return for grocery and dining spenders at 4x. Wells Fargo Active Cash offers a $200 bonus with no annual fee. Source: CNBC Select, NerdWallet May 2026

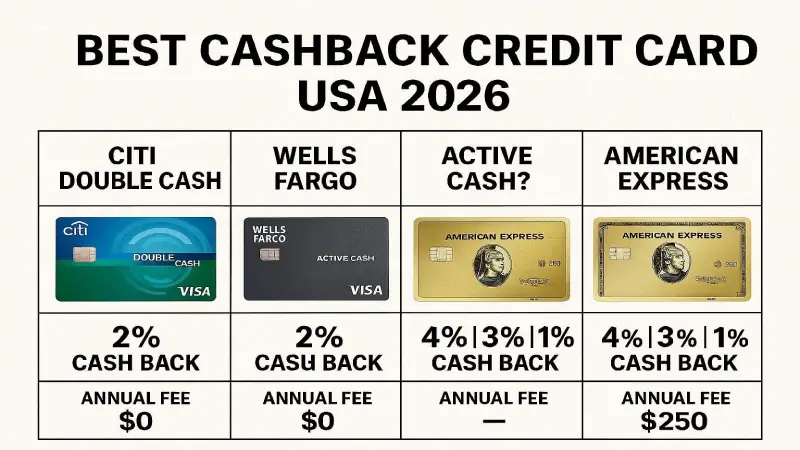

1 — Citi Double Cash: Best Simple Cashback Card

The Citi Double Cash is the gold standard of no-annual-fee cashback — earning a flat 2% on every purchase (1% when you buy, 1% when you pay), with no categories to track, no spending caps, and no annual fee. It’s the right choice for anyone who wants maximum simplicity: put everything on this card and earn a guaranteed 2% back on all spending. The cash back earns as Citi ThankYou Points, which TPG values at 1.9¢/point in May 2026 — meaning the 2% cash back rate translates to 3.8% return if transferred to airline partners like Turkish Airlines Miles&Smiles or Air France-KLM Flying Blue. No welcome bonus (the trade-off for the flat 2% rate), but no annual fee makes this a permanent wallet staple.

2 — American Express Gold: Best for Grocery + Dining Spenders

The Amex Gold at $325/year delivers the highest earning rate for food spending of any card in the US market: 4x Membership Rewards points at US supermarkets (up to $25,000 per year) and 4x at restaurants worldwide. At TPG’s Membership Rewards valuation, 4x earning translates to an 8%+ return on grocery and dining spend. For households spending $1,000+/month on food and restaurants, the Gold’s return exceeds most premium cards. Annual credits: $120 dining credit ($10/month at select partners) and $120 Uber Cash reduce the net annual fee from $325 to $85 if fully utilized. The sign-up bonus regularly exceeds 60,000–90,000 points — worth $1,200–$1,800 in travel via transfer partners.

3 — Wells Fargo Active Cash: Best No-Fee Flat Cashback

The Wells Fargo Active Cash earns a flat 2% cash rewards on all purchases (same as Citi Double Cash) with the addition of a $200 cash rewards bonus after $500 in purchases in the first 3 months — making it superior to the Double Cash for new cardholders who want an upfront bonus alongside the flat 2% rate. No annual fee, no rotating categories, cash rewards don’t expire. A 0% intro APR for 12 months on purchases adds flexibility for large purchases. For most cashback seekers who want simplicity plus a sign-up bonus, this is the practical first choice over the Citi Double Cash in 2026.

Best Balance Transfer Cards USA 2026

Wells Fargo Reflect offers the longest 0% intro APR period in the US market — 21 months on both purchases and balance transfers. With average credit card interest rates above 21% in 2026, transferring $10,000 in balance saves $2,100+ in interest during the intro period. Source: NerdWallet, WalletHub, Bankrate May 2026

1 — Wells Fargo Reflect: Best Balance Transfer Card 2026

The Wells Fargo Reflect is the unanimous top pick across NerdWallet, WalletHub, Bankrate, and Motley Fool Money for balance transfers in 2026 — and for good reason. It offers the longest 0% intro APR period available from any major issuer: 21 months on both purchases and qualifying balance transfers. Balance transfers made within 120 days of account opening qualify for the intro rate (a longer window than competing cards that cap at 60 days). No annual fee. After the intro period, variable APR of 17.49%–28.24% applies. Additional benefit: up to $600 in cell phone protection against damage or theft. The limitation: no rewards after the intro period ends — this is a debt-elimination tool, not a long-term spending card. Once your balance is paid off, switch to a rewards card.

2 — Citi Simplicity: Best for Lower Balance Transfer Fee

The Citi Simplicity offers a 0% intro APR for 21 months on balance transfers with a lower balance transfer fee than the Wells Fargo Reflect in some configurations. No late fees, no penalty APR, no annual fee — and the ability to split payments via Citi Flex Pay on eligible purchases of $75+. For borrowers who are disciplined about payments but want the security of no penalty APR if they miss one, Citi Simplicity’s terms are more forgiving.

How to Calculate Your Balance Transfer Savings

| Current Balance | Interest at 21% APR (21 months) | Balance Transfer Fee (5%) | Net Savings |

|---|---|---|---|

| $3,000 | ~$945 | $150 | ~$795 saved |

| $5,000 | ~$1,575 | $250 | ~$1,325 saved |

| $10,000 | ~$3,150 | $500 | ~$2,650 saved |

| $20,000 | ~$6,300 | $1,000 | ~$5,300 saved |

Best No Annual Fee Credit Cards USA 2026

| Card | Annual Fee | Best For | Rewards Rate | Sign-Up Bonus |

|---|---|---|---|---|

| Citi Double Cash | $0 | Simple flat cashback | 2% on everything | None |

| Wells Fargo Active Cash | $0 | Flat cashback + bonus | 2% on everything | $200 after $500 spend |

| Capital One Savor | $0 | Dining + entertainment | 3% dining/entertainment, 5% on hotels/rental cars via C1 Travel | Varies |

| Chase Freedom Flex | $0 | Rotating 5% categories | 5% on rotating quarterly categories (up to $1,500/quarter) | $200 after $500 spend |

| Chase Freedom Unlimited | $0 | Flat + dining/travel bonus | 1.5% on all purchases, 3% dining, 5% on Chase Travel | $200 after $500 spend |

| Wells Fargo Reflect | $0 | 0% APR / balance transfer | No rewards | 21 months 0% APR |

Head-to-Head Comparisons — The Most-Searched Matchups

Chase Sapphire Preferred vs Amex Gold Card

| Factor | Chase Sapphire Preferred | Amex Gold |

|---|---|---|

| Annual Fee | $95 | $325 |

| Sign-Up Bonus | 60,000 pts (~$750 travel) | 60,000–90,000 pts (~$1,200–$1,800) |

| Grocery Earning | 3x (online only) | 4x (US supermarkets up to $25K/yr) ✅ |

| Dining Earning | 3x | 4x worldwide ✅ |

| Travel Earning | 5x Chase Travel, 2x all travel ✅ | 3x flights direct/Amex Travel |

| Annual Credits | $50 hotel credit | $120 dining + $120 Uber Cash ✅ |

| Transfer Partners | 14 airline/hotel partners ✅ | 22 airline/hotel partners ✅ |

| Points Value (TPG) | 2.05¢/point | 2.0¢/point (MR points) |

| Best For | Balanced traveler, first premium card | Heavy grocery + dining spender |

Verdict: Choose Chase Sapphire Preferred if you want a single, flexible travel card at a low annual fee. Choose Amex Gold if you spend heavily on groceries ($500+/month) and dining — the 4x earning rate outperforms the Sapphire Preferred’s 3x by a margin that easily justifies the $230 fee difference for heavy food spenders.

Citi Double Cash vs Chase Sapphire Preferred

| Factor | Citi Double Cash | Chase Sapphire Preferred |

|---|---|---|

| Annual Fee | $0 ✅ | $95 |

| Rewards Rate | 2% flat on all purchases ✅ | 1x–5x depending on category |

| Sign-Up Bonus | None | 60,000 pts (~$750 travel) ✅ |

| Travel Benefits | None | Trip delay, baggage, rental car ✅ |

| Transfer Partners | 15 (via ThankYou) ✅ | 14 ✅ |

| Best For | Simplicity seekers, non-travelers | Travelers who maximize categories |

Verdict: Choose Citi Double Cash if you want zero complexity and never travel. Choose Chase Sapphire Preferred if you travel at least twice per year — the travel protections and bonus categories easily justify the $95 fee, and the sign-up bonus alone covers the fee for years.

Capital One Venture X vs Chase Sapphire Reserve

| Factor | Capital One Venture X | Chase Sapphire Reserve |

|---|---|---|

| Annual Fee | $395 ✅ | $550 |

| Travel Credit | $300 (Capital One Travel) ✅ | $300 (any travel) ✅ |

| Anniversary Bonus | 10,000 miles (~$200 value) ✅ | None |

| Base Earning | 2x on all purchases ✅ | 1x on non-bonus |

| Dining Earning | 2x | 3x worldwide ✅ |

| Lounge Guest Policy | Guest fees now apply | 2 free guests at Sapphire Lounges ✅ |

| Priority Pass | Unlimited visits ✅ | Unlimited visits ✅ |

| Net Annual Cost | ~$95 effective ($395-$300) ✅ | ~$250 effective ($550-$300) |

| Best For | Solo travelers, value maximizers | Families, heavy dining spenders |

Verdict: Capital One Venture X delivers better value for solo travelers — its net annual cost of ~$95 (after credits) is far below the Sapphire Reserve’s ~$250. Chase Sapphire Reserve is superior for family travelers (two free lounge guests) and heavy restaurant spenders (3x dining vs Venture X’s 2x).

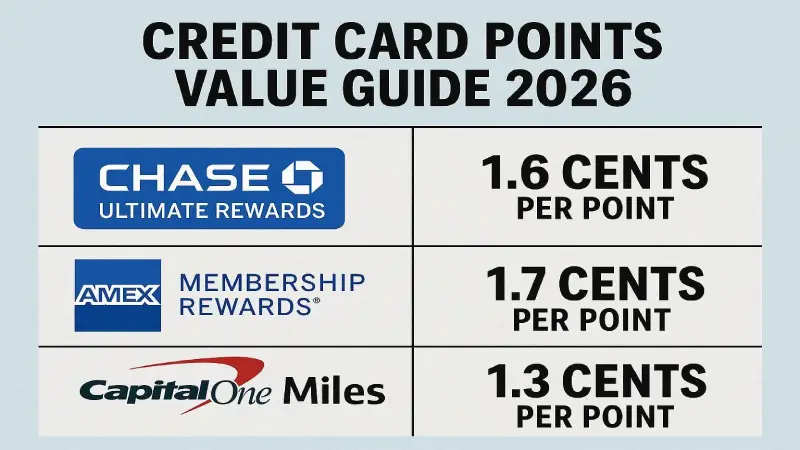

Points Value Guide — What Your Rewards Are Actually Worth in 2026

| Points Currency | Cards That Earn It | TPG Valuation (May 2026) | 60,000 Points Worth |

|---|---|---|---|

| Chase Ultimate Rewards | Sapphire Preferred/Reserve, Freedom cards | 2.05¢/point ✅ | $1,230 in travel |

| Amex Membership Rewards | Amex Gold, Platinum, Green | 2.0¢/point | $1,200 in travel |

| Citi ThankYou Points | Citi Strata Elite, Premier, Double Cash | 1.9¢/point | $1,140 in travel |

| Capital One Miles | Venture X, Venture, Savor | 1.85¢/point | $1,110 in travel |

| Chase cash back | Freedom Unlimited, Active Cash equivalent | 1.0¢/point | $600 cash |

| Amex cash back | Blue Cash Preferred/Everyday | 1.0¢/point | $600 cash |

The key insight: The face value of a sign-up bonus (« 60,000 points = $750 in travel ») is the minimum value — not the maximum. When transferred to airline partners, 60,000 Chase Ultimate Rewards points are worth $1,230 at TPG’s May 2026 valuation of 2.05¢/point. This is why the card issuers advertise face value ($750) rather than transfer value ($1,230) — and why understanding transfer partner redemptions is the single highest-leverage skill in credit card optimization.

Which Card Is Right for You? — Decision Framework

| Your Situation | Best Card | Why |

|---|---|---|

| You carry a balance and pay interest | Wells Fargo Reflect | Eliminate $2,000–$5,000 in interest during 21-month 0% window — then switch to rewards card |

| You want simplicity above all | Citi Double Cash or Wells Fargo Active Cash | Flat 2% on everything, no categories, no annual fee |

| You travel 2+ times per year | Chase Sapphire Preferred | Best combination of value, flexibility, and travel protections at $95 annual fee |

| You spend $500+/month on groceries | Amex Gold | 4x on US supermarkets — highest grocery earning rate available |

| You want premium travel, solo | Capital One Venture X | Best net value at premium tier; ~$95 effective annual cost |

| You travel with family | Chase Sapphire Reserve | Only major issuer offering 2 free lounge guests (2026) |

| You want airport lounges + max points | Amex Platinum | Broadest lounge access; worth it only if maximizing all $1,500+ in credits |

| You’re building credit | Capital One Platinum Secured | Secured card with path to upgrade |

Frequently Asked Questions — Best Credit Cards USA 2026

What is the best credit card in the USA for 2026?

There is no single « best » credit card — the best card depends on your spending profile and goals. For most travelers: Chase Sapphire Preferred ($95 annual fee, 60,000-point bonus worth ~$750-$1,230). For simplicity seekers: Citi Double Cash or Wells Fargo Active Cash (2% on everything, no annual fee). For debt consolidation: Wells Fargo Reflect (21 months 0% APR). For grocery and dining spenders: Amex Gold (4x on groceries and dining). For premium travel value: Capital One Venture X (effectively ~$95 net annual cost after credits).

Is Chase Sapphire Preferred worth it in 2026?

Yes — the Chase Sapphire Preferred remains one of the best-value travel cards in 2026. The sign-up bonus of 60,000 points is worth $750 in Chase Travel or up to $1,230 via transfer partners at The Points Guy’s May 2026 valuation of 2.05¢/point. The $95 annual fee is partially offset by the $50 annual hotel credit. Ongoing earning of 5x on Chase Travel, 3x on dining, 3x on online groceries, and 2x on all other travel makes it competitive across most spending categories. For anyone who travels at least twice per year, the travel protections (trip delay insurance, baggage insurance, rental car coverage) add meaningful value beyond the rewards.

What is the best credit card with no annual fee in 2026?

The best no-annual-fee credit card in 2026 depends on your goal: for flat cashback, Citi Double Cash (2% on everything) and Wells Fargo Active Cash (2% + $200 welcome bonus) tie for top spot. For dining and entertainment, Capital One Savor (3% on dining/entertainment, no annual fee) leads. For 0% APR or balance transfers, Wells Fargo Reflect (21 months 0% APR, no annual fee) is the clear winner. For rotating 5% categories, Chase Freedom Flex (5% on quarterly rotating categories).

How long is the Wells Fargo Reflect 0% APR period?

The Wells Fargo Reflect Card offers a 0% introductory APR for 21 months from account opening on both purchases and qualifying balance transfers — the longest 0% period available from any major US card issuer in 2026. Balance transfers must be made within 120 days of account opening to qualify for the intro rate. A balance transfer fee of 5% (minimum $5) applies. After 21 months, a variable APR of 17.49%–28.24% applies. The card has no annual fee and no rewards — it is specifically designed as a debt elimination tool.

Amex Gold vs Chase Sapphire Preferred — which is better?

For grocery and dining spenders: Amex Gold is better. Its 4x earning rate at US supermarkets and restaurants outperforms the Sapphire Preferred’s 3x, and the $240 in annual credits ($120 dining + $120 Uber Cash) reduce the effective annual fee from $325 to $85. For travelers and those with mixed spending: Chase Sapphire Preferred is better. Its $95 annual fee is lower, its Chase Ultimate Rewards points are valued at 2.05¢/point (above Amex MR’s 2.0¢), and its travel protections (trip delay, baggage delay, rental car) are stronger. If your monthly grocery and restaurant spend exceeds $1,500, the Amex Gold’s higher earning rate produces more value.

What credit score do I need for Chase Sapphire Preferred?

Chase Sapphire Preferred typically requires a good to excellent credit score — generally 700+ FICO score for reasonable approval odds, and 720+ for strong approval odds. Chase also applies the 5/24 rule: if you have opened 5 or more credit card accounts in the past 24 months (across all issuers), Chase will automatically deny your application regardless of credit score. Check your credit score before applying and count your new card openings in the past 2 years before applying for any Chase card.

Final Verdict — Best Credit Cards USA 2026

The 2026 credit card market rewards informed consumers — the difference between the right and wrong card for your profile can exceed $1,200 in annual value. Our top picks by profile: Chase Sapphire Preferred for most travelers ($95, best sign-up bonus value-to-fee ratio); Amex Gold for grocery and dining spenders (4x, recoverable fee); Capital One Venture X for solo premium travelers (best net annual cost); Citi Double Cash or Wells Fargo Active Cash for simplicity seekers (no fee, 2% flat); Wells Fargo Reflect for anyone paying credit card interest (21 months 0% APR — the single highest-ROI card move available in 2026). The single best financial move for anyone currently paying 21%+ interest on credit card debt is applying for the Wells Fargo Reflect and transferring that balance immediately. For related financial guides, see our Best High-Yield Savings Accounts USA 2026 and Best Personal Loans USA 2026.

Disclaimer: Credit card terms, sign-up bonuses, annual fees, and APR offers are subject to change and vary by applicant creditworthiness. Points valuations are based on The Points Guy’s May 2026 estimates and are not guaranteed redemption values. This article is for informational purposes only and does not constitute financial advice. Nexuora may receive compensation from some credit card issuers. Updated May 26, 2026.

Ahmada Ndao is a financial research analyst and independent journalist

specializing in US consumer finance, legal rights, and insurance markets.

With over 5 years covering American financial products, he has helped

thousands of readers navigate complex insurance decisions, find the right

legal representation, and optimize their credit strategies. His research

methodology combines primary data analysis, direct outreach to industry

professionals, and continuous monitoring of federal regulatory changes.

Ahmada’s work has been cited by financial communities across the US and

reviewed by licensed attorneys and insurance professionals for accuracy.