Progressive is one of the three largest auto insurance providers in the United States, writing over $60 billion in premiums annually and covering vehicles in all 50 states. Its scale gives it access to massive actuarial datasets, a nationwide repair network, and the financial stability to absorb large-scale catastrophic claims events.

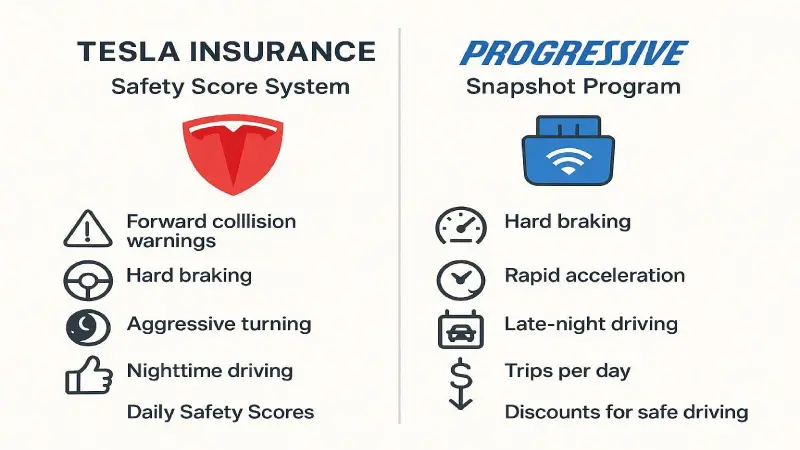

Tesla Insurance remains unique in the market because it integrates directly with Tesla vehicle driving data — not through a third-party app or plug-in device, but through the car’s own onboard computer. This direct integration creates a genuinely different pricing model than anything Progressive or traditional competitors offer.

Both insurers have made meaningful investments in EV coverage as the Tesla fleet has grown. But their fundamental approaches to risk assessment, pricing, and claims handling diverge significantly.

| Feature | Progressive | Tesla Insurance |

|---|---|---|

| Nationwide Availability | Yes — all 50 states | Limited — state-by-state expansion |

| Real-Time Tesla Telemetry | No | Yes — direct vehicle integration |

| Telematics Program | Snapshot (app or plug-in) | Safety Score (automatic) |

| OEM Parts Guarantee | No | Yes — Tesla-certified only |

| Best For | High-risk flexibility, bundles | Safe Tesla drivers with high scores |

| Multi-Policy Bundles | Excellent — home, renters, boat, RV | Moderate — limited bundle options |

| High-Risk Driver Acceptance | Strong | Score-dependent — volatility risk |

| Mobile Experience | Very good | Excellent — Tesla app integrated |

| Credit Score Weight | Moderate | Lower weight |

| Financial Strength | A+ (AM Best) | Not independently rated |

| Claims Network Size | Very large nationwide | Tesla Service Centers + partners |

| Autopilot Usage Benefit | No direct benefit | Yes — improves Safety Score |

Progressive works better for drivers who want traditional insurance flexibility, nationwide support, and access to bundle discounts. Tesla Insurance favors cautious Tesla owners with consistently excellent Safety Scores who live in states where Tesla Insurance is available. For a comparison with the other major traditional competitor, see: Tesla Insurance vs GEICO 2026.

The answer depends on your specific driving profile, location, risk history, and bundling situation. There is no universal winner — but there are clear winner profiles for each insurer.

Location remains one of the biggest pricing factors for Tesla insurance. State regulations, litigation environments, repair costs, and weather exposure all drive significant variation. See our dedicated state comparison: Tesla Insurance California vs Texas.

California

Tesla Insurance’s pricing advantage is largest in California. Direct state operations, California’s regulatory environment (Prop 103 limiting credit score use), and Tesla’s EV-specific repair cost modeling combine to produce consistently lower rates than Progressive in the state’s major markets.

| Insurer | Monthly Premium |

|---|---|

| Tesla Insurance | $301 |

| Progressive | $365 |

| Annual Savings (Tesla) | $768 |

Winner: Tesla Insurance — largest state-level advantage in the national market.

Texas

Texas offers competitive pricing from both carriers. Tesla Insurance’s advantage narrows compared to California but remains meaningful for safe drivers. GEICO actually leads in Texas — see our full state comparison for details.

| Insurer | Monthly Premium |

|---|---|

| Tesla Insurance | $297 |

| Progressive | $331 |

| Annual Savings (Tesla) | $408 |

Winner: Tesla Insurance for safe drivers.

Florida

Florida’s expensive insurance environment narrows the gap between carriers. No-fault requirements, litigation exposure, and hurricane risk push both companies toward similar pricing. Progressive’s larger Florida claims network can be advantageous post-hurricane when Tesla Service Centers face capacity constraints.

| Insurer | Monthly Premium |

|---|---|

| Tesla Insurance | $432 |

| Progressive | $447 |

| Annual Savings (Tesla) | $180 |

Winner: Tesla Insurance on price, but Progressive’s claims network advantage is more relevant in Florida than any other state.

New York

| Insurer | Monthly Premium |

|---|---|

| Tesla Insurance | $455 |

| Progressive | $471 |

| Annual Savings (Tesla) | $192 |

Winner: Tesla Insurance on price. New York’s Tesla Service Center density is improving but Progressive’s broader repair network remains an operational advantage in dense metro areas.

State Availability Note

Tesla Insurance is not available in every state. Progressive’s nationwide availability in all 50 states means it is the only option in states where Tesla Insurance has not yet launched. Drivers should verify Tesla Insurance availability in their specific state before planning coverage around it. For a full EV insurer availability overview, see: Best EV Insurance Companies USA 2026.

Understanding coverage specifics is essential — a lower monthly premium only provides value if the coverage quality meets your actual needs after an accident.

| Coverage Component | Progressive | Tesla Insurance |

|---|---|---|

| Liability (Bodily Injury) | Yes — up to policy limits | Yes — up to policy limits |

| Liability (Property Damage) | Yes | Yes |

| Collision | Yes — approved repair network | Yes — Tesla-certified repair |

| Comprehensive | Yes — approved repair network | Yes — Tesla-certified repair |

| Uninsured Motorist | Yes | Yes |

| Medical Payments / PIP | Yes — where state required | Yes — where state required |

| OEM Parts Guarantee | No — aftermarket possible | Yes — Tesla OEM only |

| Roadside Assistance | Optional add-on | Included via Tesla app |

| Rental Reimbursement | Optional add-on | Optional add-on |

| Gap Coverage | Available | Available |

| Autopilot Recalibration Coverage | Covered under collision/comp | Directly specified in policy |

| Battery Replacement Coverage | Standard comprehensive coverage | Full coverage available |

| Custom Parts and Equipment | Available add-on | Built into EV pricing model |

| Loan/Lease Payoff | Available | Available |

The OEM parts guarantee remains Tesla Insurance’s most significant coverage advantage. After any covered collision, Tesla Insurance ensures your vehicle is repaired with genuine Tesla parts — preserving Autopilot sensor calibration, structural integrity, and software compatibility. Progressive’s policy may use aftermarket parts that, while potentially similar in appearance, may not maintain the precision tolerances required for Autopilot’s forward-facing cameras and sensors.

Tesla repair costs are extremely high regardless of insurer — minimum coverage exposes drivers to catastrophic financial risk. Full coverage is strongly recommended for all Model Y and Model 3 owners. For comprehensive discount strategies, see: Best Insurance Discounts for Tesla Owners in 2026.

Ahmada Ndao is a financial research analyst and independent journalist

specializing in US consumer finance, legal rights, and insurance markets.

With over 5 years covering American financial products, he has helped

thousands of readers navigate complex insurance decisions, find the right

legal representation, and optimize their credit strategies. His research

methodology combines primary data analysis, direct outreach to industry

professionals, and continuous monitoring of federal regulatory changes.

Ahmada’s work has been cited by financial communities across the US and

reviewed by licensed attorneys and insurance professionals for accuracy.