Electric vehicles cost 20–65% more to insure than equivalent gas-powered cars — and most EV owners don’t find out why until they file a claim. The average full-coverage insurance cost for a Tesla is $4,149/year versus $2,513/year for the average vehicle nationally. A minor fender-bender can damage the battery pack — a component that costs $5,000–$15,000 to replace and requires factory-approved repair shops that most standard insurers don’t know how to handle. This guide cuts through the marketing to show you real 2026 premiums by Tesla model, what the top 7 EV insurers actually cover (and don’t), how battery replacement coverage works — and which insurer is the cheapest for your specific situation.

Table of Contents

- Why EV Insurance Costs More — The Real Reasons

- Real Costs by Tesla Model — 2026 Annual Premiums

- Top 7 EV Insurance Providers — Full Rankings

- Battery Replacement Coverage — The Gap Nobody Talks About

- Provider Comparison Table

- Non-Tesla EVs — Rivian, Lucid, Chevy EV Costs

- How to Save on EV Insurance

- Frequently Asked Questions

Why Electric Vehicle Insurance Costs More — The Real Reasons

Insurance premiums are based on expected claims cost. For EVs, that expected cost is genuinely higher — not because insurers are arbitrarily marking up rates, but because EVs cost more to repair, require specialist technicians, and have limited approved repair networks. Here are the four main drivers.

1. High Repair Costs

EVs use advanced materials (aluminum, high-strength steel) and integrated systems that cost significantly more to repair than conventional vehicles. A minor collision that would cost $800 to repair on a gas vehicle can cost $2,000–$4,000 on a Tesla because of the aluminum body panels, integrated sensor systems, and proprietary components. Tesla-approved body shops must use Tesla-approved parts, which have no aftermarket alternatives and carry higher margins.

2. Limited Repair Network

Tesla requires collision repairs to be completed at Tesla-approved body shops or Tesla-approved independent shops. In major metros, this network is growing — but in smaller cities and rural areas, the nearest approved shop may be 50–150 miles away. This drives up claim costs because vehicles must often be towed long distances and may require rental cars for extended periods during repair.

3. Battery Pack Exposure

The battery pack on a Tesla Model 3 is worth $5,000–$10,000. On a Model S or Model X, replacement costs can reach $15,000–$22,000. Even minor undercarriage damage in a collision can damage the battery pack. Insurers price this risk into premiums because a moderate accident that would total a $15,000 gas car may require a $12,000 battery replacement on a $45,000 Tesla — making the vehicle uneconomical to repair even when it appears only moderately damaged.

4. Vehicle Value

Teslas and most EVs are high-value vehicles. The Tesla Model Y starts at $44,000; the Model S at $74,000+. Higher vehicle value directly increases comprehensive and collision premiums because the insurer’s maximum exposure is higher.

| Factor | Gas Vehicle Average | Tesla Average | Premium Impact |

|---|---|---|---|

| Full coverage annual premium | $2,513/yr | $4,149/yr | +65% |

| Average repair cost per claim | ~$3,500 | ~$5,900 | +69% |

| Approved repair network | Nationwide | Restricted | Higher towing costs |

| Battery replacement cost | N/A | $5K–$20K | Significant exposure |

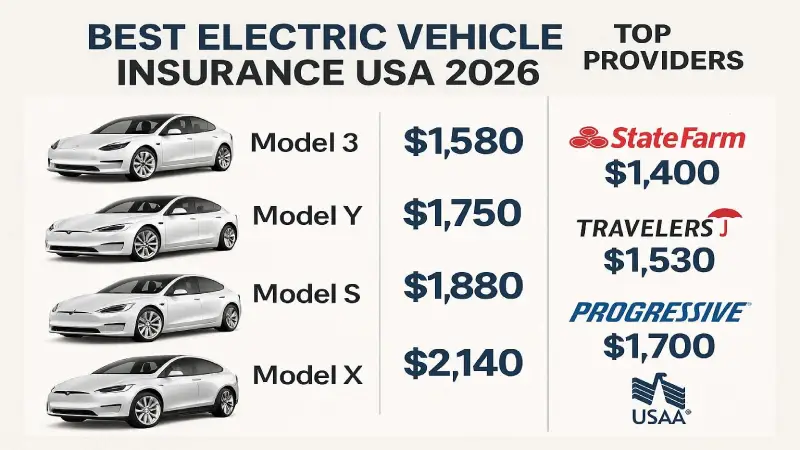

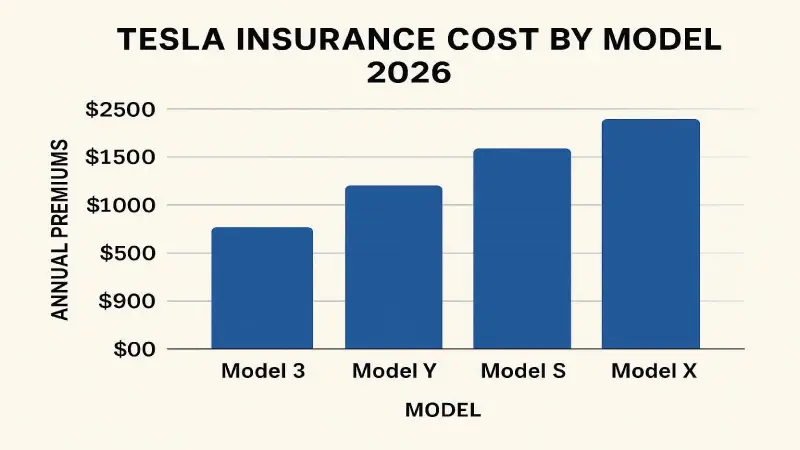

Real Costs by Tesla Model — 2026 Annual Premiums

| Tesla Model | Avg Annual Premium | Avg Monthly | Cheapest Insurer | Cheapest Annual Rate |

|---|---|---|---|---|

| Model 3 | $3,871/yr | $323/mo | State Farm | ~$1,545/yr |

| Model Y | $3,836/yr | $320/mo | State Farm / GEICO | ~$3,242/yr |

| Model S | $5,200+/yr | $433+/mo | Nationwide | ~$2,800/yr |

| Model X | $4,800+/yr | $400+/mo | State Farm | ~$2,600/yr |

| Cybertruck | $4,500–$6,000/yr | $375–$500/mo | Varies by state | Still limited data |

Top 7 Electric Vehicle Insurance Providers — Full Rankings 2026

#1 — State Farm: Best Overall for EV Insurance

State Farm earns the top spot for EV insurance in 2026 on the strength of three factors: consistently the cheapest or near-cheapest rates for most Tesla models (Model 3 as low as $1,545/year; Model Y ~$3,242/year); A++ AM Best financial rating and the highest J.D. Power claims satisfaction score among major national carriers (882/1,000); and EV-specific coverage that explicitly includes charging equipment protection and battery replacement coverage for collision-damaged batteries. State Farm’s Drive Safe & Save usage-based program offers discounts for safe driving that EV owners — who tend to be smoother drivers than average — frequently maximize. The limitation: State Farm no longer writes new policies in California or Massachusetts.

#2 — Nationwide: Best EV Discount + Cheapest for Model S

Nationwide is the best choice for Tesla Model S owners (their cheapest insurer nationally) and offers the highest EV-specific discount in the market at 10% off for electric vehicles. Their SmartRide telematics program offers up to 40% good-driver discount — the largest UBI discount available from any major insurer. Nationwide also offers gap insurance for financed EVs (critical given EV depreciation patterns) and covers home charging equipment as an endorsement. Available in all 50 states.

#3 — Tesla Insurance: Best for Real-Time Pricing

Tesla’s own insurance product uses real-time driving data from the vehicle’s built-in sensors to set your monthly premium. Safe drivers get the lowest rates — Tesla claims their best drivers pay significantly below market. Available in 12 states: Arizona, California, Colorado, Illinois, Maryland, Minnesota, Nevada, Ohio, Oregon, Texas, Utah, and Virginia. Tesla Insurance claims are handled through the app and repairs go directly to Tesla-certified shops — eliminating the network friction that drives up costs with traditional insurers. The limitation: if you’re a higher-risk driver or live outside the 12 states, this option isn’t available.

#4 — GEICO: Best for Tesla Model Y on Budget

GEICO is typically the cheapest insurer for Tesla Model Y in many markets and offers competitive multi-vehicle discount of up to 25%. GEICO’s digital experience is strong and claims processing is faster than average. However, GEICO does not offer EV-specific endorsements — no dedicated EV discount, no charging equipment coverage as standard. They’re a solid budget choice but not the best if you want EV-tailored coverage.

#5 — Progressive: Best for Customization + Snapshot Discount

Progressive’s Snapshot telematics program gives EV owners — who typically drive more smoothly than gas-vehicle drivers — meaningful discounts of up to 30%. Progressive also offers gap coverage and upgrade coverage add-ons specifically designed for EV modifications. Their NAIC complaint ratio is below average (favorable) and they’re available in all 50 states. The 10% bundle discount for home + auto is lower than some competitors, but their base EV rates are competitive in most markets.

#6 — COUNTRY Financial: Best for Non-Tesla EVs

COUNTRY Financial is the least-known option on this list but offers the cheapest rates for non-Tesla electric vehicles — average monthly rates of $48 for liability and $89 for full coverage. If you drive a Chevy Bolt, Nissan Leaf, Hyundai Ioniq, or similar non-Tesla EV, COUNTRY Financial consistently underprices the major carriers. Available in 19 states primarily in the Midwest and South.

#7 — Travelers: Best for Tesla Model Y in California

With California’s unique insurance market (where State Farm no longer writes new policies), Travelers is consistently ranked among the top options for California Tesla owners. Their J.D. Power score is above average, their California rates are competitive, and they offer a dedicated EV endorsement. For California EV owners who lost access to State Farm or Allstate, Travelers is the strongest replacement option.

Battery Replacement Coverage — The Gap Most EV Owners Miss

This is the most important coverage detail for EV owners — and the one most glossed over by insurance comparison sites. Here is exactly what is and is not covered.

| Battery Situation | Covered by Standard Auto Insurance? | Details |

|---|---|---|

| Battery damaged in collision | ✅ Yes | Covered under collision coverage like any other collision damage |

| Battery damaged by fire/theft/hail | ✅ Yes | Covered under comprehensive coverage |

| Battery gradual degradation | ❌ No | Not covered by any insurer — maintenance/wear item |

| Battery failure outside warranty | ❌ No | Manufacturer warranty only; no insurance product covers this |

| Home charging equipment damaged | ⚠️ Sometimes | Requires specific endorsement (State Farm, Nationwide offer this) |

| Charging cable stolen | ⚠️ Sometimes | Covered under comprehensive if policy explicitly includes it |

Tesla's Battery Warranty — What It Covers

Tesla’s warranty covers battery defects and retains a minimum of 70% capacity for 8 years or 100,000–150,000 miles (depending on model). What it does NOT cover: gradual battery degradation below 70% capacity, damage from improper charging, flood damage to the battery, or any battery issue after the warranty period expires. Once your Tesla’s warranty expires, you carry the full financial risk of battery failure — a risk that standard auto insurance does not address.

What to Ask Your Insurer

When getting a quote for EV insurance, ask these specific questions: Does your policy explicitly cover battery replacement in a collision claim? Is home charging equipment (Level 2 EVSE) covered under your policy or as an endorsement? What is your approved repair network for my specific vehicle make? Do you have experience handling total loss claims on EVs where the battery is damaged but the body is relatively intact?

EV Insurance Provider Comparison Table 2026

| Insurer | Model 3 Rate | EV Discount | Battery Coverage | Charging Coverage | UBI Program | AM Best |

|---|---|---|---|---|---|---|

| State Farm | ~$1,545/yr ✅ | None specific | Collision ✅ | Endorsement ✅ | Drive Safe & Save | A++ |

| Nationwide | Competitive | 10% ✅ | Collision ✅ | Endorsement ✅ | SmartRide (40%) | A+ |

| Tesla Insurance | Varies (real-time) | N/A | ✅ Full | ✅ Included | Real-time safety score | N/A |

| GEICO | Competitive | None specific | Collision ✅ | ❌ Standard only | DriveEasy | A++ |

| Progressive | Competitive | None specific | Collision ✅ | Add-on available | Snapshot (30%) | A+ |

| COUNTRY Financial | ~$89/mo (non-Tesla) | EV rate ✅ | Collision ✅ | Available | Limited | A+ |

| Travelers | Competitive (CA) | EV endorsement | Collision ✅ | Available | IntelliDrive | A++ |

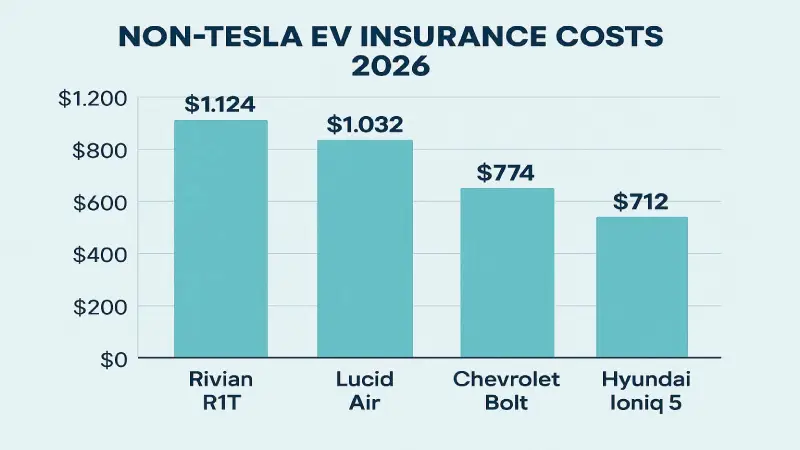

Non-Tesla EVs — Insurance Costs for Rivian, Lucid, Chevy & Others

| EV Model | Avg Annual Premium | Notes |

|---|---|---|

| Rivian R1T / R1S | $3,800–$5,500/yr | Limited approved repair shops; newer brand; high vehicle value |

| Lucid Air | $5,000–$7,500/yr | Ultra-luxury; very limited repair network; high parts cost |

| Chevy Equinox EV | $1,800–$2,800/yr | Most affordable EV to insure; GM dealer network available |

| Chevy Bolt EV | $1,600–$2,400/yr | Budget EV; standard GM repair network; lower value |

| Hyundai Ioniq 6 | $2,200–$3,200/yr | Growing dealer network; competitive repair costs |

| Ford Mustang Mach-E | $2,400–$3,500/yr | Ford dealer network advantage; broad availability |

| BMW i4 | $3,500–$5,000/yr | Luxury premium; BMW dealer network nationwide |

The pattern is clear: EVs with established dealer-based repair networks (Chevy, Ford, Hyundai) are significantly cheaper to insure than brand-only repair network vehicles (Tesla, Rivian, Lucid). If minimizing insurance cost is a priority in your EV purchase decision, mainstream brands with broad dealer networks offer a meaningful ongoing cost advantage.

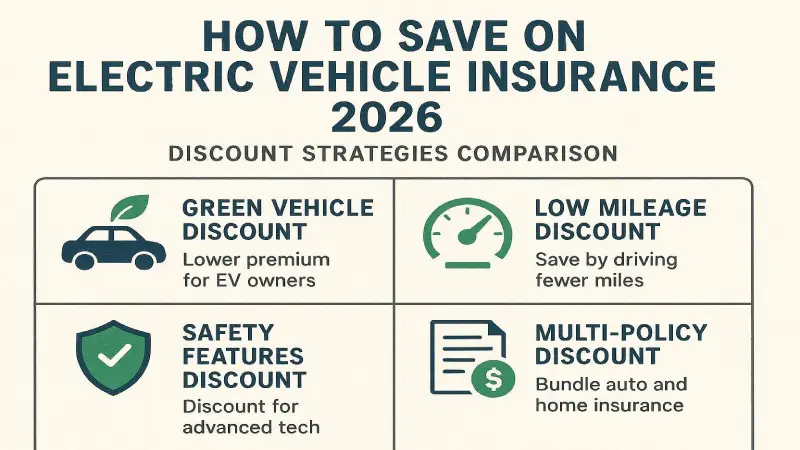

How to Save on EV Insurance — 6 Proven Strategies

1. Use Telematics / Usage-Based Insurance (UBI)

EV drivers tend to accelerate smoothly, brake gradually, and drive at consistent speeds — behaviors that telematics programs reward with the maximum discounts. Nationwide’s SmartRide (up to 40% off), Progressive’s Snapshot (up to 30% off), and State Farm’s Drive Safe & Save are designed to benefit exactly this driving profile. Enroll in a UBI program and you can frequently offset 20–30% of your EV’s premium surcharge.

2. Bundle Home and Auto

Home + auto bundle discounts of 17–25% apply to both policies — on an EV premium of $4,000/year, a 25% bundle discount saves $1,000/year. If you own a home and insure it separately, switching both to State Farm or Liberty Mutual produces meaningful total savings even if the standalone EV rate is above competitors.

3. Increase Your Deductible

Moving from a $500 to a $1,000 deductible typically reduces collision and comprehensive premiums by 15–25%. For EV owners who can afford a higher out-of-pocket maximum, this is the fastest way to reduce monthly premiums. For a $4,000/year policy, a 20% reduction saves $800/year.

4. Take the Federal EV Tax Credit and Reduce Your Insured Value

The federal EV tax credit (up to $7,500 for qualifying new EVs) reduces your effective purchase price. Work with your insurer to ensure your vehicle’s insured value reflects the post-credit cost — this can slightly reduce your comprehensive coverage premium without affecting actual protection.

5. Ask About EV-Specific Discounts

Nationwide offers a 10% EV discount. Travelers offers an EV endorsement discount. Several regional insurers offer green vehicle discounts. These are not automatically applied — you must specifically ask. If your current insurer has no EV discount, mention it in your next renewal negotiation or use it as a switching argument when getting competitive quotes.

6. Compare at Least 4 Quotes Before Buying

The difference between the most expensive and least expensive insurer for the same Tesla in the same ZIP code can exceed $2,000/year. State Farm at $1,545/year versus the average of $3,871/year for a Model 3 is a real data point. Spending 30 minutes comparing quotes can save more than any other single action you take.

Frequently Asked Questions — Electric Vehicle Insurance 2026

Why is electric vehicle insurance more expensive than regular car insurance?

EV insurance costs more for four main reasons: higher vehicle purchase prices (meaning higher comprehensive and collision premiums), expensive repairs requiring specialist technicians and proprietary parts, limited approved repair networks that increase towing and rental costs, and battery pack exposure (a $5,000–$20,000 component that can be damaged in moderate collisions). The average Tesla costs $4,149/year to insure versus $2,513/year for the average vehicle nationally — a 65% premium.

What is the cheapest car insurance for Tesla in 2026?

State Farm is consistently the cheapest insurer for most Tesla models in 2026, with rates as low as $1,545/year for a Model 3 (vs. the $3,871 national average). Nationwide and GEICO are the next cheapest options. Tesla’s own insurance is the cheapest option for safe drivers in the 12 states where it’s available (Arizona, California, Colorado, Illinois, Maryland, Minnesota, Nevada, Ohio, Oregon, Texas, Utah, Virginia). The best rate for your specific vehicle depends heavily on your ZIP code, driving record, and age — always compare at least 4 quotes.

Does car insurance cover EV battery replacement?

Standard auto insurance covers battery replacement ONLY if the battery is damaged in a covered incident — a collision, fire, theft, or comprehensive peril. Gradual battery degradation, manufacturing defects after the warranty period, and non-collision battery failure are NOT covered by any standard auto insurance policy. Tesla’s manufacturer warranty covers battery defects and a minimum of 70% capacity retention for 8 years or up to 150,000 miles (model-dependent) — but this is not insurance, it’s a warranty.

Does my home charging station affect my auto insurance?

Your home charging equipment (Level 2 EVSE) is typically covered under your homeowners or renters insurance policy as personal property — not your auto policy. However, if the charger is damaged by your vehicle (backing into it, for example), your auto policy’s collision coverage may apply. Some auto insurers (State Farm, Nationwide) offer explicit charging equipment endorsements on your auto policy. Ask your insurer which policy covers your specific charging setup.

Is Tesla Insurance worth it?

Tesla Insurance is worth it for safe drivers in the 12 states where it’s available. It uses real-time driving behavior data to price premiums monthly — safe drivers pay less than traditional insurers charge. The advantages: claims go directly through the Tesla app, repairs are handled by Tesla-certified shops, and it covers Tesla-specific components explicitly. The limitations: only available in 12 states, pricing varies month-to-month based on driving score, and higher-risk drivers may pay more than alternatives. Compare Tesla Insurance’s quoted rate against State Farm and Nationwide before deciding.

Final Verdict — Best EV Insurance USA 2026

For most Tesla owners: State Farm for price, Nationwide for EV discounts, Tesla Insurance for safe drivers in eligible states. The single most impactful action you can take is comparing at least 4 quotes — the spread between the cheapest and most expensive insurer for the same vehicle can exceed $2,000/year. For non-Tesla EV owners: COUNTRY Financial for budget vehicles, Travelers for California, State Farm everywhere else. Always ask specifically about EV discounts, charging equipment coverage, and the insurer’s approved repair network for your vehicle before signing — the cheapest premium is worthless if the claims experience is poor. For related coverage, see our guide on Best Car Insurance USA 2026 and our Progressive Snapshot vs Allstate Drivewise comparison.

Disclaimer: Premium estimates are based on May 2026 national averages and vary significantly by state, driver profile, and coverage level. Always obtain personalized quotes before purchasing. Nexuora is not affiliated with any insurer. Updated May 26, 2026.

Ahmada Ndao is a financial research analyst and independent journalist

specializing in US consumer finance, legal rights, and insurance markets.

With over 5 years covering American financial products, he has helped

thousands of readers navigate complex insurance decisions, find the right

legal representation, and optimize their credit strategies. His research

methodology combines primary data analysis, direct outreach to industry

professionals, and continuous monitoring of federal regulatory changes.

Ahmada’s work has been cited by financial communities across the US and

reviewed by licensed attorneys and insurance professionals for accuracy.