Best 0% APR Balance Transfer Credit Cards 2026 — No Interest, Real Fees & Who Approves You Fastest

The average American carrying credit card debt pays $1,380 per year in interest alone — money that buys nothing, protects nothing, and builds no equity. A 0% APR balance transfer card eliminates that interest expense entirely for 12–21 months, creating a window to pay down principal aggressively without a single dollar going to interest. In 2026, the best balance transfer cards offer up to 21 months at 0% APR — meaning a $6,000 balance transferred to the right card and paid down at $286/month costs exactly $0 in interest. The same balance at 22% APR costs $1,320 in interest over 21 months before the balance is cleared. This guide compares every major 0% balance transfer card available in 2026 — with honest transfer fee analysis, approval odds by credit score, and a step-by-step guide to completing a balance transfer successfully.

🏆 Top 8 Best 0% APR Balance Transfer Cards USA 2026

| # | Card | 0% APR Period | Transfer Fee | Annual Fee | Best For |

|---|---|---|---|---|---|

| 🥇 1 | Wells Fargo Reflect Card | 21 months 🏆 | 5% (min $5) | $0 | Longest 0% period — large balances |

| 🥈 2 | Citi Diamond Preferred | 21 months 🏆 | 5% (min $5) | $0 | Longest period tied · Citi ecosystem |

| 🥉 3 | BankAmericard Credit Card | 18 months | 3% (min $10) | $0 | Lowest transfer fee · BofA customers |

| 4 | Chase Slate Edge | 18 months | 3% intro, 5% after 60 days | $0 | Best for Chase customers |

| 5 | Citi Simplicity Card | 21 months | 5% (min $5) | $0 | No late fees · Most forgiving terms |

| 6 | Discover it Balance Transfer | 18 months | 3% intro, 5% after | $0 | Cash back rewards + balance transfer |

| 7 | US Bank Visa Platinum | 18 months | 3% (min $5) | $0 | Best cell phone protection add-on |

| 8 | Capital One Quicksilver | 15 months | 3% | $0 | Best when you also want cash rewards |

💰 Real Savings — How Much Can a Balance Transfer Save You?

The financial case for a balance transfer is straightforward when the numbers are laid out clearly. Here is the real math for three common balance scenarios at the current average APR of 22.8%:

| Balance | Monthly Min Payment | Interest at 22.8% (21 mo) | Transfer Fee (5%) | Net Saving | Months to Pay Off (Same Payment) |

|---|---|---|---|---|---|

| $3,000 | $75 | $1,197 | $150 | $1,047 saved | 21 months (paid in full) |

| $6,000 | $150 | $2,394 | $300 | $2,094 saved | 21 months (paid in full) |

| $10,000 | $250 | $3,990 | $500 | $3,490 saved | 21 months (paid in full) |

| $15,000 | $375 | $5,985 | $750 | $5,235 saved | 21 months (paid in full) |

🔍 Full Card Reviews — Top 5 Detailed 2026

1. Wells Fargo Reflect Card — Best Overall (21 Months, $0 Fee)

The Wells Fargo Reflect Card offers the longest 0% APR balance transfer period available in the US market in 2026 — 21 months from account opening. This is tied with the Citi Diamond Preferred and Citi Simplicity for the longest available offer, but the Reflect's 5% transfer fee (minimum $5) applies to all transfers made within 120 days of account opening. On a $10,000 balance, the $500 transfer fee is recovered within the first 3 months of avoided 22.8% APR interest, making the economics compelling for any substantial balance.

The Reflect has no annual fee and no rewards — it is a pure debt-reduction tool. After the 21-month 0% period, the APR rises to 17.74%–29.49% variable based on creditworthiness. The Reflect also includes cell phone protection (up to $600 per claim, 2 claims per year, $25 deductible) when you pay your monthly phone bill with the card — a useful secondary benefit. Wells Fargo does not have the most sophisticated customer experience of the major card issuers, but for a card held specifically for balance transfer purposes, service quality is a secondary consideration.

- ✅ 21 months 0% APR — longest available tied

- ✅ $0 annual fee

- ✅ Cell phone protection included

- ✅ Transfers allowed from most major US card issuers

- ❌ 5% transfer fee — higher than BankAmericard

- ❌ No rewards on spending

- ❌ 120-day window for 0% rate on transfers

2. Citi Diamond Preferred — Best for Citi Ecosystem Users

The Citi Diamond Preferred matches the Wells Fargo Reflect with a 21-month 0% APR balance transfer offer and carries the same 5% transfer fee. For existing Citi banking or credit card customers, the Diamond Preferred has a modest integration advantage — transfers between Citi accounts can be processed faster, and Citi's customer service infrastructure handles account issues more smoothly when you already have a relationship with the bank. The Diamond Preferred also carries a 0% introductory APR on purchases for 12 months — useful if you need to make large purchases without immediately adding high-interest debt while paying down your transferred balance. No annual fee.

- ✅ 21 months 0% APR — longest available tied

- ✅ 12 months 0% on purchases too

- ✅ $0 annual fee

- ✅ Fast processing for Citi-to-Citi transfers

- ❌ 5% transfer fee

- ❌ No rewards programme

3. BankAmericard — Best Transfer Fee (3%, 18 Months)

The BankAmericard Credit Card offers the lowest transfer fee of any competitive 0% balance transfer card — 3% (minimum $10) — combined with an 18-month 0% APR period. For large balances where transfer fees represent a significant cost, the 3% fee saves meaningfully versus the 5% charged by the 21-month cards. On a $12,000 balance, the BankAmericard's $360 fee saves $240 versus the Wells Fargo Reflect's $600 fee. Whether the 3-month shorter 0% period costs you money versus the lower fee depends on your paydown pace — if you can pay off the balance within 18 months, the BankAmericard is the lower total cost option for large balances.

- ✅ 3% transfer fee — lowest among competitive offers

- ✅ 18 months 0% APR

- ✅ $0 annual fee

- ✅ Best for large balances ($10,000+) where fee savings matter

- ❌ 3 months shorter than the 21-month leaders

- ❌ No rewards

- ❌ Better for existing BofA customers

4. Citi Simplicity — Best for Forgiveness (No Late Fees)

The Citi Simplicity Card is unique in the balance transfer market: it charges no late fees and no penalty APR — meaning if you miss a minimum payment during the 0% period, you are not immediately penalised with a rate jump to 29%+ or a late fee charge. This feature is particularly valuable for cardholders who have had previous difficulty with payment consistency and want a safety net during the debt paydown process. The 21-month 0% period matches the best available, the 5% transfer fee applies, and there is no annual fee. The Simplicity does not offer rewards — it is a pure debt management tool with maximum consumer forgiveness built in.

- ✅ No late fees — unique consumer protection

- ✅ No penalty APR — miss a payment without losing your 0% rate

- ✅ 21 months 0% APR

- ✅ $0 annual fee

- ❌ 5% transfer fee

- ❌ No rewards

5. Discover it Balance Transfer — Best for Combining Debt Reduction with Rewards

The Discover it Balance Transfer is the only card on this list that offers competitive cash back rewards alongside the balance transfer benefit. The card earns 5% cash back on rotating quarterly categories (gas, groceries, restaurants, Amazon, etc. — up to $1,500 per quarter) and 1% on everything else, with Discover matching all cash back earned in the first year (the "Cashback Match"). The 18-month 0% APR applies to balance transfers, and an introductory 3% transfer fee applies for transfers completed in the first 3 months (5% thereafter). For consumers who want to pay down debt while also capturing rewards on new spending, the Discover it Balance Transfer is the best hybrid option.

- ✅ 5% cash back on rotating categories + Cashback Match

- ✅ 18 months 0% APR on transfers

- ✅ 3% intro transfer fee (for 3 months)

- ✅ $0 annual fee

- ❌ 0% period shorter than 21-month leaders

- ❌ Rewards require active category management

💳 Transfer Fees — The Hidden Cost You Must Calculate First

Every balance transfer card charges a one-time transfer fee — typically 3–5% of the amount transferred. This fee is added to your balance on the new card and does not accrue interest during the 0% period. Understanding the fee's real impact requires simple arithmetic:

3% vs 5% Fee — Real Dollar Comparison

| Balance | 3% Fee (BankAmericard) | 5% Fee (Wells Fargo/Citi) | Fee Difference | Months to Recover at 22.8% APR |

|---|---|---|---|---|

| $3,000 | $90 | $150 | $60 | ~1 month |

| $6,000 | $180 | $300 | $120 | ~1 month |

| $10,000 | $300 | $500 | $200 | ~1 month |

| $15,000 | $450 | $750 | $300 | ~1 month |

| $20,000 | $600 | $1,000 | $400 | ~1 month |

The break-even between 3% and 5% fee cards versus the 3-month longer 0% period of 5% cards: If you will not fully pay your balance in 18 months, the 3 additional months at 0% from the 21-month cards is worth more than the 2% fee savings from BankAmericard. If you will definitively pay in full within 18 months, BankAmericard's lower fee saves you money. When uncertain, the 21-month 5% cards provide more insurance against underestimating your paydown timeline.

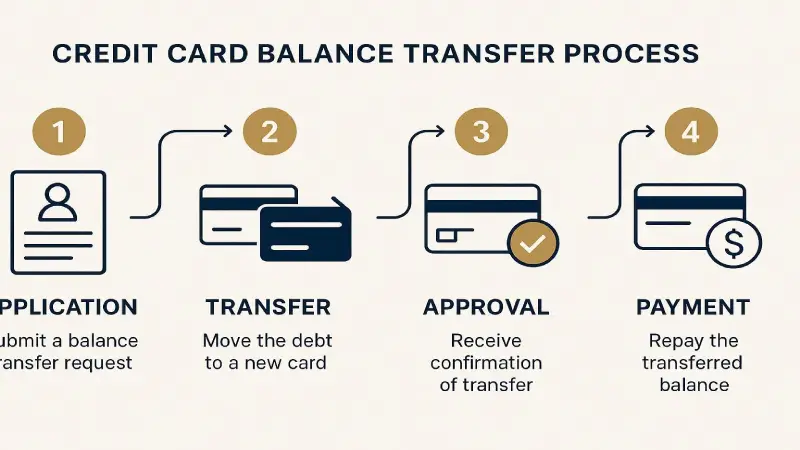

📋 How to Do a Balance Transfer — Step by Step 2026

Step 1 — Apply for the balance transfer card (Day 1)

Apply online for your chosen card. You will need: your Social Security Number, annual income, housing payment amount, and the account numbers and balances of the debts you want to transfer. Many cards offer instant approval decisions — if approved, you will typically receive your card and account number within 7–10 business days. Some issuers allow you to initiate the balance transfer request during the application process — Chase and Citi both offer this option, which can speed up the process.

Step 2 — Request the balance transfer (Days 1–10)

Once approved, log into your new card account or call customer service to initiate the balance transfer. You will need: the name of the creditor you are transferring from, your account number with that creditor, and the amount you want to transfer. Important: You typically cannot transfer balances between cards from the same issuer — you cannot transfer a Chase balance to another Chase card, or a Citi balance to another Citi card. Transfers must be from a different bank's card.

Step 3 — Continue paying the original card (Days 5–14)

Balance transfers take 5–10 business days to complete. During this period, continue making minimum payments on your original card. If a payment is due and the transfer has not yet processed, make the payment. Missing a payment on your original card while waiting for a transfer will generate late fees and credit score damage — neither of which is reversed when the transfer finally completes.

Step 4 — Verify the transfer completed (Day 10–14)

Check both accounts — your new card should show a balance equal to the transferred amount plus the transfer fee. Your original card should show a zero or reduced balance. Call your original card issuer to confirm the account status and consider whether to close it or keep it open (keeping it open improves your credit utilisation ratio as long as you do not use it).

Step 5 — Set up autopay and create a payoff plan (Day 14+)

Set up automatic minimum payment on your new balance transfer card immediately — missing even one payment on a balance transfer card can trigger the loss of your 0% APR and activate the penalty rate (sometimes 29%+). Then calculate your required monthly payment to pay off the full balance before the 0% period ends: balance ÷ number of 0% months = required monthly payment. For a $6,000 balance on a 21-month card: $6,000 ÷ 21 = $286/month. Set up this payment amount as your recurring autopay.

📊 Approval Odds by Credit Score

| Credit Score Range | FICO Category | Best Cards Available | Expected Transfer Limit |

|---|---|---|---|

| 750–850 | Exceptional | All cards — best terms | 50–80% of credit limit |

| 700–749 | Good | Most cards — good terms | 40–70% of credit limit |

| 670–699 | Fair | Discover it, Citi Simplicity (some) | 30–50% of credit limit |

| 640–669 | Below Average | Very limited — may not qualify | Minimal if approved |

| Below 640 | Poor | Not eligible for 0% transfer cards | N/A |

The 0% APR balance transfer cards require good-to-excellent credit for approval — generally a FICO score of 670+ for most cards and 700+ for the best terms. The credit limit you receive determines the maximum balance you can transfer, and transfer limits are typically set at 80–90% of your credit limit (not 100%). If your balance exceeds your new card's transfer limit, you can transfer a partial balance and pay down the remainder on your original card aggressively during the 0% period.

⚠️ 6 Balance Transfer Mistakes That Cost Thousands

Mistake 1 — Making new purchases on the balance transfer card

Many cardholders make the mistake of using their new balance transfer card for everyday purchases. This can cause problems because: payments are typically applied to the lowest-APR balance first (your 0% transferred balance), meaning new purchases at the regular APR accumulate interest while your transferred balance is paid down. Effectively, new purchases on a balance transfer card accrue interest from day one at the regular APR. Keep your balance transfer card for the transferred balance only — use a different card for new spending.

Mistake 2 — Missing the transfer window

Most cards require transfers to be initiated within 60–120 days of account opening to qualify for the 0% promotional rate. Transfers initiated after this window are processed at the standard (non-promotional) APR. Submit your transfer request as soon as your account is open — do not wait weeks while the card sits unused.

Mistake 3 — Not creating a payoff plan before transferring

Transferring a balance without a concrete monthly payment plan is a recipe for still having a balance when the 0% period expires. Calculate your required monthly payment on day one. If you cannot pay the full balance within the 0% window at a realistic monthly payment amount, reconsider the transfer or look for the longest available 0% period.

Mistake 4 — Closing the original card immediately

After a successful balance transfer, closing your original credit card account reduces your total available credit and increases your credit utilisation ratio — both of which can reduce your credit score by 20–50 points. Keep the original card open with a $0 balance (or make small periodic purchases and pay them in full) to maintain your credit limit and credit history length.

Mistake 5 — Ignoring the balance transfer fee in your budget

The transfer fee is added to your balance immediately. Your debt on the new card is the transferred amount plus the fee. Budget for this — your required monthly payment should reflect the total balance including the fee, not just the transferred amount.

Mistake 6 — Missing a minimum payment

Missing even one minimum payment on a balance transfer card can trigger the loss of your 0% promotional rate — some cards will apply the penalty APR (which can exceed 29%) retroactively to your entire balance. Set up autopay for at least the minimum payment amount on the day you activate your new card. This is non-negotiable.

🎯 What to Do After the 0% Period Ends

Planning for the end of the 0% period is essential — the promotional rate expiration is the single most financially dangerous moment in the balance transfer lifecycle. There are three scenarios and three appropriate responses:

Scenario 1 — Balance is fully paid before expiration. You achieved the goal. The card's regular APR becomes irrelevant because you carry no balance. You can now choose to keep the card open for credit utilisation benefits or close it if it has no ongoing value. Consider whether the credit limit is useful for your credit profile before closing.

Scenario 2 — Significant balance remains, and you qualify for another balance transfer. Apply for a second 0% balance transfer card 2–3 months before your current 0% period expires — giving enough time for approval and transfer processing. Transfer the remaining balance to the new card. This strategy — sometimes called "balance transfer surfing" — can extend your interest-free paydown window by an additional 18–21 months. Note that each new credit application creates a hard inquiry and the new card may have a different transfer limit. Do not assume approval is guaranteed for a second card.

Scenario 3 — Balance remains, and you do not qualify for another transfer. Call your current card issuer and request a lower APR — issuers frequently accommodate customers with good payment history. Alternatively, investigate a personal loan (typically 8–18% APR for good credit) as a lower-cost paydown vehicle than the standard credit card APR that will apply at expiration.

For managing finances alongside debt reduction, see our complete guide to travel rewards credit cards — because once you are debt-free, those same dollars can start earning you free travel: Best Travel Rewards Credit Cards 2026.

❓ Frequently Asked Questions — 0% APR Balance Transfer Cards 2026

What is the longest 0% APR balance transfer available in 2026?

The longest 0% APR balance transfer period available in the US in 2026 is 21 months, offered by three cards: the Wells Fargo Reflect Card, the Citi Diamond Preferred Card, and the Citi Simplicity Card. All three charge a 5% balance transfer fee (minimum $5). The 21-month period allows a $6,000 balance to be paid off at $286/month with zero interest — saving approximately $2,094 compared to carrying that balance at the current average APR of 22.8%. For very large balances ($15,000+), the BankAmericard's 3% transfer fee (18-month 0% period) may save more total money despite the shorter window, depending on your monthly payment capacity.

Does a balance transfer hurt your credit score?

A balance transfer can have both positive and negative short-term impacts on your credit score. Negative: applying for a new credit card generates a hard inquiry, which typically reduces your score by 5–10 points temporarily. Positive: the new card's credit limit increases your total available credit, which reduces your overall credit utilisation ratio — the second most important factor in your FICO score. If you have $10,000 in existing balances and your new balance transfer card has a $12,000 limit, your total available credit increases by $12,000 while your balance stays the same (before the transfer), meaningfully reducing utilisation. As you pay down the transferred balance, your credit utilisation continues to improve. Most cardholders who use balance transfers correctly see a net credit score improvement over 12–18 months as their balance-to-limit ratio falls.

Can you do a balance transfer between cards from the same bank?

No — balance transfers between cards issued by the same bank are not permitted. You cannot transfer a Chase balance to another Chase card, a Citi balance to another Citi card, or a Wells Fargo balance to the Wells Fargo Reflect Card. Balance transfers must be from a card issued by a different bank. This rule exists because banks would otherwise face a situation of essentially refinancing their own loans. Always verify that the debt you want to transfer is held by a different issuer than the balance transfer card you are applying for.

What happens if I don't pay off my balance before the 0% period ends?

When the 0% promotional period expires, your remaining balance begins accruing interest at the card's standard variable APR — which ranges from approximately 17% to 29%+ depending on your creditworthiness and the card. Importantly, no retroactive interest is charged on the balance you already paid during the 0% period — only the remaining balance going forward is affected. If you still have a significant balance remaining as the expiration approaches, your options are: apply for a second 0% balance transfer card (2–3 months before expiration); call the current issuer and request a lower ongoing APR; or investigate a personal loan at a lower rate than the standard card APR to pay off the remaining balance.

Is a 3% or 5% balance transfer fee better?

A 3% fee is lower, but the cards offering 3% transfer fees (BankAmericard, Chase Slate Edge, Discover it) provide 18 months of 0% APR versus 21 months from the 5% fee cards. The right choice depends on your paydown timeline. If you can definitively pay your full balance within 18 months, the 3% card saves 2% in fees — $200 on a $10,000 balance. If there is any chance you will need more than 18 months, the 21-month card at 5% provides 3 more months of interest protection worth significantly more than the 2% fee difference at current 22.8% average APRs. When in doubt, choose the 21-month card — the insurance value of 3 extra months at 0% is real, and the fee difference is modest on typical consumer balances.

How many balance transfers can I do?

There is no legal limit on the number of balance transfers you can do over your lifetime. However, each new balance transfer card application generates a hard credit inquiry and reduces the average age of your credit accounts — both slightly negative for your credit score. Most lenders want to see consistent, responsible credit management rather than frequent new account openings. In practice, two to three balance transfers on the same debt (if you need to "surf" from one 0% card to the next) is financially sound if the alternative is paying high-APR interest. Beyond three transfers on the same debt, the pattern of new card applications may affect your approval odds for the next card. The most financially effective strategy is a single transfer with a long enough 0% period and a disciplined payoff plan that eliminates the debt entirely within that period.

✅ Final Verdict — Best 0% APR Balance Transfer Cards 2026

For most consumers, the Wells Fargo Reflect Card or Citi Simplicity are the best choices — 21 months at 0% APR gives the longest available runway to eliminate high-interest debt. The Citi Simplicity's no-late-fee protection adds a valuable safety net for less consistent payers. For large balances ($12,000+) where transfer fee savings are significant, the BankAmericard's 3% fee saves real money versus the 5% alternatives — if you are confident you can pay in full within 18 months. Once debt-free, redirect that interest money toward building wealth — see how travel credit card rewards can work for you at Best Travel Rewards Credit Cards 2026.

Disclaimer: Credit card terms and 0% APR offers change frequently. All data reflects April 2026 public card offers. Always verify current terms directly with the card issuer before applying. Nexuora does not receive commission from any card issuer. Updated April 23, 2026.

Ahmada Ndao is a financial research analyst and independent journalist

specializing in US consumer finance, legal rights, and insurance markets.

With over 5 years covering American financial products, he has helped

thousands of readers navigate complex insurance decisions, find the right

legal representation, and optimize their credit strategies. His research

methodology combines primary data analysis, direct outreach to industry

professionals, and continuous monitoring of federal regulatory changes.

Ahmada’s work has been cited by financial communities across the US and

reviewed by licensed attorneys and insurance professionals for accuracy.