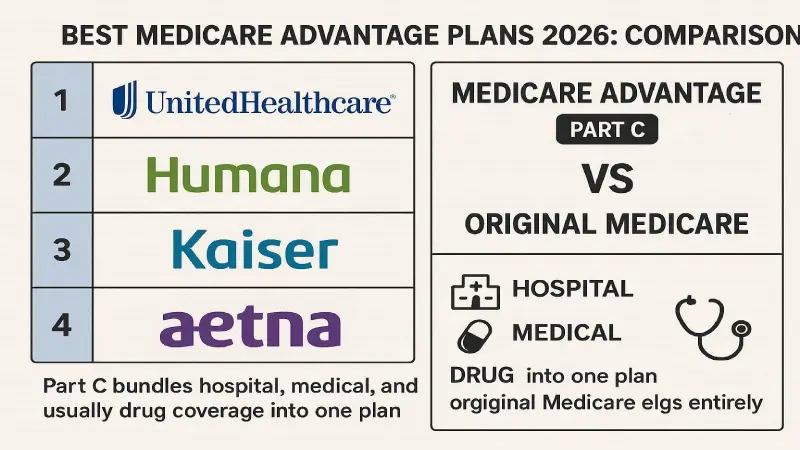

| Rank | Provider | CMS Stars | Best For | Avg Premium | J.D. Power | Score |

|---|---|---|---|---|---|---|

| #1 | UnitedHealthcare Editor’s Choice | 4.0–5.0★ | Most enrollees | $0–$32 | ⭐ #2 | 4.8/5 |

| #2 | Kaiser Permanente | 5.0★ | Integrated care | $0–$45 | ⭐ #1 | 4.8/5 |

| #3 | Humana | 4.0★ | Low premium | $0–$18 | ⭐ #3 | 4.7/5 |

| #4 | Aetna (CVS Health) | 3.5–4.5★ | Rural access | $0–$28 | Above avg. | 4.6/5 |

| #5 | Blue Cross Blue Shield | 3.5–5.0★ | Local networks | $0–$55 | Above avg. | 4.5/5 |

| #6 | Cigna | 3.5–4.5★ | Chronic conditions | $0–$40 | Average | 4.4/5 |

| #7 | Anthem | 3.5–4.0★ | Multi-state coverage | $0–$38 | Average | 4.3/5 |

| #8 | Wellcare | 3.0–4.0★ | Low income (D-SNP) | $0 | Below avg. | 4.1/5 |

| #9 | Molina Healthcare | 3.0–4.0★ | Dual eligible | $0 | Below avg. | 4.0/5 |

| #10 | Devoted Health | 4.0–5.0★ | Tech-forward seniors | $0–$25 | N/A (new) | 3.9/5 |

UnitedHealthcare Best Overall 2026

4.8/5 Nexuora

4–5★CMS Star Rating

$0Min. Monthly Premium

43States with 5-Star Plans

Our verdict: UnitedHealthcare is the best Medicare Advantage insurer for most Americans — period. Their AARP-branded plans cover the widest network (1M+ providers), offer $0 premium options in nearly every state, and include extras like fitness memberships (Renew Active), transportation, and meal delivery. If you want one quote, start here.

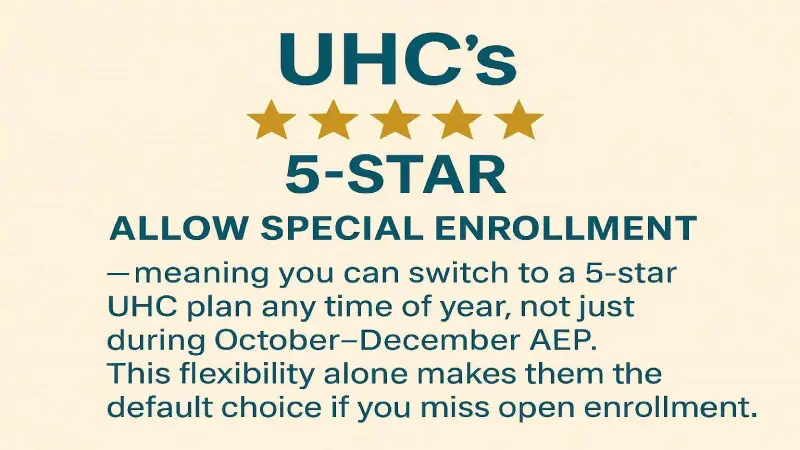

What other review sites miss: UHC’s 5-star plans allow Special Enrollment — meaning you can switch to a 5-star UHC plan any time of year, not just during October–December AEP. This flexibility alone makes them the default choice if you miss open enrollment.

Ahmada Ndao is a financial research analyst and independent journalist

specializing in US consumer finance, legal rights, and insurance markets.

With over 5 years covering American financial products, he has helped

thousands of readers navigate complex insurance decisions, find the right

legal representation, and optimize their credit strategies. His research

methodology combines primary data analysis, direct outreach to industry

professionals, and continuous monitoring of federal regulatory changes.

Ahmada’s work has been cited by financial communities across the US and

reviewed by licensed attorneys and insurance professionals for accuracy.