Best Homeowners Insurance Companies USA 2026 — Ranked by J.D. Power, AM Best & NAIC Complaint Index

The average American homeowner overpays $612 per year for home insurance — simply by staying with their current insurer without comparing. But choosing the right homeowners insurance company isn't just about finding the lowest premium. The insurer that promises $1,200/year and delivers a $40,000 settlement on a $90,000 kitchen fire claim is vastly inferior to the insurer charging $1,600/year that pays the full $90,000 without dispute. Three independent data sources — J.D. Power's annual home insurance satisfaction study, AM Best's financial strength ratings, and the NAIC's complaint index — provide the most objective picture of which homeowners insurance companies actually perform when you need them most. This complete 2026 guide ranks every major US homeowners insurer across all three metrics, with real average premiums and a definitive verdict on who leads for each homeowner profile.

🏆 Master Ranking — J.D. Power + AM Best + NAIC Combined 2026

| # | Company | J.D. Power Score | AM Best Rating | NAIC Complaint Index | Avg Annual Premium | Overall Verdict |

|---|---|---|---|---|---|---|

| 🥇 1 | USAA | 900/1,000 🏆 | A++ | 0.51 🏆 | $1,640 | Best in class — military eligible only |

| 🥈 2 | Amica Mutual | 868/1,000 | A+ | 0.43 🏆 | $1,760 | Best non-military · Lowest complaints |

| 🥉 3 | State Farm | 882/1,000 🏆 | A++ | 0.68 ✅ | $1,780 | Best nationally available overall |

| 4 | Erie Insurance | 856/1,000 | A+ | 0.62 ✅ | $1,620 🏆 | Best value · Cheapest premium |

| 5 | Auto-Owners Insurance | 861/1,000 | A++ | 0.59 ✅ | $1,690 | Best mid-size carrier |

| 6 | Travelers | 833/1,000 | A++ | 0.84 ✅ | $1,810 | Best risk management resources |

| 7 | Allstate | 829/1,000 | A+ | 1.24 ⚠️ | $2,120 | Best bundle discount — standalone is expensive |

| 8 | Nationwide | 827/1,000 | A+ | 0.76 ✅ | $1,860 | Best for farm/rural properties |

| 9 | Chubb | 822/1,000 | A++ | 0.38 🏆 | $2,480 | Best for high-value homes ($1M+) |

| 10 | Liberty Mutual | 805/1,000 ⚠️ | A | 1.42 ⚠️ | $1,980 | Only competitive when bundling home+auto |

| 11 | Farmers | 797/1,000 ⚠️ | A | 1.38 ⚠️ | $2,060 | Below average on all 3 metrics |

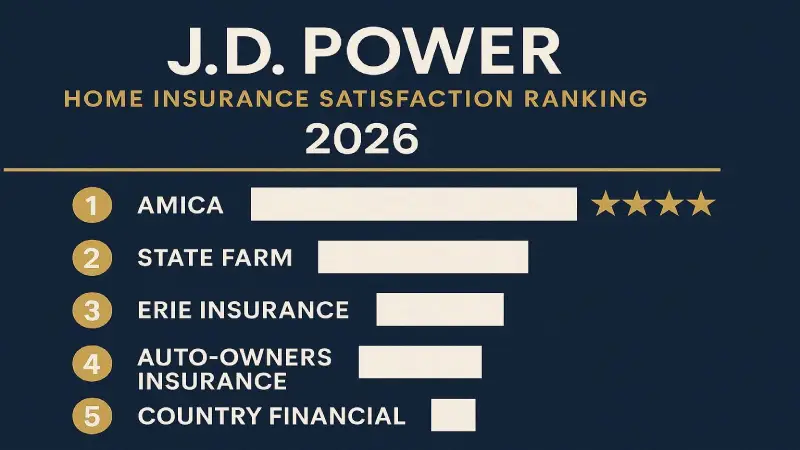

⭐ J.D. Power 2026 Home Insurance Rankings — Full Breakdown

J.D. Power's annual U.S. Home Insurance Study is the most widely cited consumer satisfaction benchmark in the homeowners insurance industry. The 2026 study surveyed 13,200 homeowners insurance customers and measured satisfaction across five factors, listed in order of importance to overall satisfaction: interaction (ease of contacting and working with the insurer), policy offerings (coverage options and customisation), price (perceived value for premium paid), billing and payment (ease of payment, accuracy of billing), and claims (speed, communication, and fairness of claims handling). The overall satisfaction score reflects a weighted combination of all five factors on a 1,000-point scale.

| Company | J.D. Power Score | vs Industry Avg (821) | Strongest Factor | Weakest Factor |

|---|---|---|---|---|

| USAA | 900 🏆 | +79 points | Claims handling | N/A — leads all categories |

| State Farm | 882 🏆 | +61 points | Interaction (agent network) | Price perception |

| Auto-Owners | 861 | +40 points | Policy offerings | Digital experience |

| Erie Insurance | 856 | +35 points | Price perception | National availability |

| Amica Mutual | 868 | +47 points | Claims satisfaction | Price (above average premium) |

| Travelers | 833 | +12 points | Policy offerings | Interaction |

| Industry Average | 821 | — | — | — |

| Allstate | 829 | +8 points | Digital experience | Claims settlement amount |

| Nationwide | 827 | +6 points | Policy offerings | Claims communication |

| Chubb | 822 | +1 point | Claims quality | Price (premium-priced) |

| Liberty Mutual | 805 ⚠️ | -16 points | Digital experience | Claims handling |

| Farmers | 797 ⚠️ | -24 points | Agent relationships | Claims settlement |

What J.D. Power Scores Actually Mean for You

A 16-point difference between State Farm (882) and Liberty Mutual (805) may seem small numerically — but in the context of the J.D. Power 1,000-point scale, it represents a statistically significant difference in customer experience. The J.D. Power score most directly predicts how smoothly your claims experience will go — the highest-scoring carriers have demonstrably better communication during claims, faster resolution, and higher settlement satisfaction. When your house floods or burns, you want the insurer with the 882 score, not the 805 score.

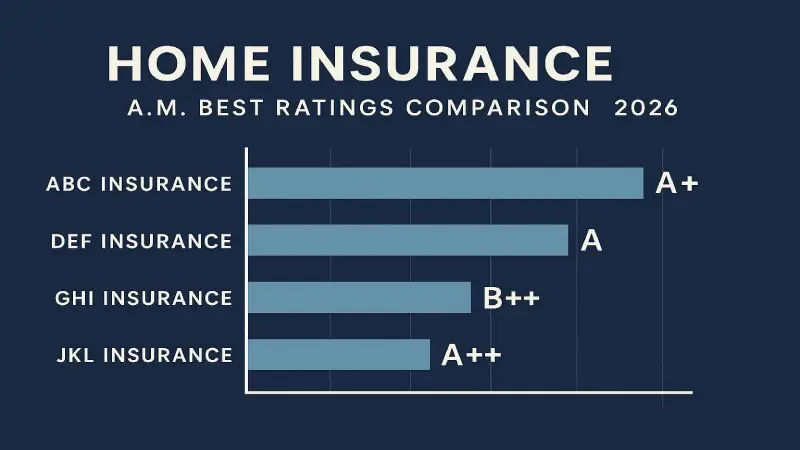

🏦 AM Best Ratings — Financial Strength in Plain English

AM Best is the oldest and most respected credit rating agency specialising in the insurance industry. Their Financial Strength Rating (FSR) assesses an insurer's ability to meet ongoing insurance obligations — in plain terms, whether they have the financial reserves to pay your claim if a major disaster hits. Understanding the rating scale demystifies what these letters mean practically:

| AM Best Rating | Category | What It Means | Major Carriers at This Level |

|---|---|---|---|

| A++ | Superior | Exceptional financial strength — highest reserve levels | USAA, State Farm, Chubb, Travelers, Auto-Owners |

| A+ | Superior | Very strong — highly capable of meeting obligations | Amica, Erie, Allstate, Nationwide |

| A | Excellent | Strong — good capacity to meet insurance obligations | Liberty Mutual, Farmers, Hippo |

| A- | Excellent | Good — some vulnerability in severe economic conditions | Openly, Kin, some regional carriers |

| B++ | Good | Adequate — more vulnerable to adverse conditions | Genworth (LTC segment) |

| Below B++ | Fair/Poor | Significant concerns — avoid for primary coverage | Avoid for homeowners insurance |

Practical guidance: For standard homeowners insurance covering a $200,000–$800,000 home, the practical difference between A++ and A is minimal — both rating levels have more than sufficient reserves to pay normal claims. The AM Best rating becomes critically important in catastrophic scenarios — a major regional disaster (hurricane Ian in Florida, Camp Fire in California) that generates tens of thousands of simultaneous claims. Carriers with A++ ratings have demonstrated they maintain reserves to pay massive catastrophic event claims without financial strain. Choose A or above for all homeowners insurance — avoid any carrier below A-.

📊 NAIC Complaint Index — The Most Underused Rating

The NAIC (National Association of Insurance Commissioners) complaint index is the most underused but most practically revealing rating in homeowners insurance comparison. It measures the ratio of formal consumer complaints filed with state insurance regulators versus the number of complaints expected given the insurer's market share. A score of 1.00 means the company receives exactly the expected number of complaints. Below 1.00 means fewer complaints than expected — better. Above 1.00 means more complaints than expected — a warning signal.

Unlike J.D. Power (which measures satisfaction surveys) or AM Best (which measures financial strength), the NAIC index measures actual formal complaints — situations where a policyholder was unhappy enough to file a regulatory complaint against their insurer. This represents real disputes about claim denials, settlement amounts, delays, and coverage interpretations. It is the most direct measure of claims-handling problems.

| Company | NAIC Complaint Index | Interpretation | vs Average (1.00) |

|---|---|---|---|

| Chubb | 0.38 🏆 | 62% fewer complaints than expected | Far better |

| Amica Mutual | 0.43 🏆 | 57% fewer complaints than expected | Far better |

| USAA | 0.51 🏆 | 49% fewer complaints than expected | Far better |

| Auto-Owners | 0.59 ✅ | 41% fewer complaints than expected | Better |

| Erie Insurance | 0.62 ✅ | 38% fewer complaints than expected | Better |

| State Farm | 0.68 ✅ | 32% fewer complaints than expected | Better |

| Nationwide | 0.76 ✅ | 24% fewer complaints than expected | Better |

| Travelers | 0.84 ✅ | 16% fewer complaints than expected | Slightly better |

| Industry Average | 1.00 | — | Average |

| Allstate | 1.24 ⚠️ | 24% more complaints than expected | Worse |

| Farmers | 1.38 ⚠️ | 38% more complaints than expected | Worse |

| Liberty Mutual | 1.42 ⚠️ | 42% more complaints than expected | Significantly worse |

💰 Real Rates — Average Annual Premiums by Carrier 2026

The following premiums are estimated annual averages for a single-family home with $300,000 in dwelling coverage, $200,000 personal property, $100,000 liability, and a $1,000 deductible in a low-to-moderate risk ZIP code. Actual premiums vary significantly by state, location, home age, and individual risk profile.

| Company | Avg Annual Premium ($300K home) | vs National Avg ($1,820) | Best Discount Available |

|---|---|---|---|

| Erie Insurance | $1,620 🏆 | -$200 (-11%) | Multi-policy bundle |

| USAA | $1,640 | -$180 (-10%) | Military loyalty |

| Auto-Owners | $1,690 | -$130 (-7%) | Multi-policy + claims-free |

| State Farm | $1,780 | -$40 (-2%) | Multi-policy 17% |

| Amica Mutual | $1,760 | -$60 (-3%) | Dividend policy (returns surplus) |

| National Average | $1,820 | — | — |

| Travelers | $1,810 | -$10 (-1%) | Green home discount |

| Nationwide | $1,860 | +$40 (+2%) | Smart home device discount |

| Liberty Mutual | $1,980 | +$160 (+9%) | Bundle up to 25% |

| Farmers | $2,060 | +$240 (+13%) | Multi-policy bundle |

| Allstate | $2,120 | +$300 (+16%) | Bundle up to 25% |

| Chubb | $2,480 | +$660 (+36%) | Risk management programme |

🔍 Full Reviews — Top 7 Carriers Detailed 2026

1. USAA — Best in America (Military Families Only)

USAA is objectively the best homeowners insurance company in America — leading every major quality metric simultaneously. Their J.D. Power score of 900/1,000 is the highest of any insurer in the study. Their NAIC complaint index of 0.51 means they receive half the complaints expected for their size. Their AM Best rating of A++ represents the highest possible financial strength. And their average premium of $1,640 for a $300K home is below the national average. The only limitation: USAA is exclusively available to active military members, veterans, and their immediate family members. If you are eligible, there is no reason to compare further — USAA wins unambiguously. Apply at usaa.com and verify your eligibility.

2. State Farm — Best Nationally Available Carrier

State Farm is America's largest homeowners insurer and the strongest nationally available option across all three rating dimensions. Their J.D. Power score of 882/1,000 is the highest of any carrier available to all Americans — 61 points above the industry average. Their NAIC complaint index of 0.68 reflects 32% fewer complaints than expected for their massive size (28M+ customers). Their AM Best rating of A++ — the highest possible — reflects over a century of sound financial management. State Farm's 19,000+ exclusive agents provide the most accessible in-person service of any national insurer, which directly drives their interaction satisfaction scores. Their average premium of $1,780 is only slightly above national average and their 17% multi-policy bundle discount makes them highly competitive for homeowners who also insure their vehicle with State Farm.

3. Amica Mutual — Best Non-Military Carrier for Claims

Amica Mutual is the quiet leader of homeowners insurance quality — less advertised than Allstate or Liberty Mutual, but consistently outperforming both on every quality metric. As a mutual insurance company, Amica is owned by its policyholders rather than shareholders — meaning surplus funds are returned to policyholders as dividends rather than extracted as profit. Their dividend policies return 5–20% of annual premium to policyholders who have a claims-free year. Amica's NAIC complaint index of 0.43 — the second-lowest among major national carriers — reflects their exceptional claims handling. Their J.D. Power score of 868 places them comfortably above the industry average. The trade-off: Amica is not available in every state and their online presence is less developed than pure digital carriers.

4. Erie Insurance — Best Value Carrier

Erie Insurance offers the lowest average premium of any major rated homeowners insurer ($1,620/year for a $300K home) while maintaining quality scores well above the industry average — J.D. Power 856/1,000 and NAIC 0.62. Erie is a regional carrier available in 12 states (Illinois, Indiana, Kentucky, Maryland, New York, North Carolina, Ohio, Pennsylvania, Tennessee, Virginia, West Virginia, Wisconsin) plus Washington DC. Within those states, Erie consistently delivers the best combination of competitive pricing and service quality available. Their "Guaranteed Replacement Cost" standard coverage — which pays to rebuild your home to its pre-loss condition regardless of what it costs, even if it exceeds your policy limit — is one of the most generous standard coverage terms in the market.

5. Auto-Owners Insurance — Hidden Gem

Auto-Owners Insurance is one of the least-known but highest-rated homeowners insurers in the United States — available in 26 states through independent agents. Their NAIC complaint index of 0.59 and J.D. Power score of 861 both reflect above-average performance, and their AM Best A++ rating confirms exceptional financial strength. Auto-Owners is exclusively agent-distributed — you cannot purchase directly — which means the buying experience requires finding an independent agent who represents them, but also means you get personalised advice rather than a generic online experience. For homeowners in their coverage area who value quality service over digital convenience, Auto-Owners deserves serious consideration.

6. Travelers — Best Risk Management Resources

Travelers is the only major homeowners insurer that provides genuine risk management services to policyholders as a standard benefit — not just a marketing claim. Their IntelliDrive home programme monitors weather and environmental risks specific to your property and sends alerts before adverse events. Their loss control resources — including home inspection tools, maintenance checklists, and safety programme templates — help policyholders prevent losses rather than just claim after them. Travelers' AM Best A++ rating and above-average J.D. Power score (833) make them a solid choice, particularly for homeowners who value the risk prevention partnership model.

7. Chubb — Best for High-Value Homes

Chubb is not the right insurer for average-value homes — their premiums ($2,480 average for $300K) reflect a premium-service model designed for high-value properties. But for homes valued above $750,000–$1,000,000, Chubb is the unambiguous leader. Their Masterpiece policy provides agreed value coverage (no coinsurance clauses, no depreciation arguments at claim time), risk consulting services from in-house engineers, cash settlement options (they will write you a check for the agreed value and let you rebuild as you see fit), and the strongest claims service of any insurer (NAIC complaint index 0.38 — the lowest of any major carrier). For luxury homeowners, the premium difference versus standard carriers is justified by the claims certainty and coverage precision that Chubb delivers.

🎯 Best Homeowners Insurer by Profile 2026

| Profile | Best Choice | Runner-Up | Why | Avoid |

|---|---|---|---|---|

| Military / veteran family | 🏆 USAA | State Farm | Leads all metrics at lower price | Liberty Mutual, Farmers |

| Best overall non-military | 🏆 State Farm | Amica | Highest J.D. Power + AM Best nationally available | Allstate, Liberty Mutual |

| Lowest complaints priority | 🏆 Chubb | Amica | NAIC 0.38 / 0.43 — least complaint-generating | Farmers, Liberty Mutual |

| Best price (standard home) | 🏆 Erie | USAA (if eligible) | $1,620 avg — lowest of major carriers | Chubb, Allstate |

| High-value home ($750K+) | 🏆 Chubb | PURE Insurance | Agreed value · Best claims · Luxury specialist | Standard carriers |

| Bundle home + auto | 🏆 State Farm | Erie | Quality claims + agent relationship | Farmers, Liberty Mutual |

| Best digital experience | 🏆 Hippo | Openly | Modern insurtech — app-first management | Traditional carriers |

| Rural / farm property | 🏆 Nationwide | Auto-Owners | Farm-in-High product · Agricultural specialisation | Chubb (urban-focused) |

📋 Beyond the Ratings — 5 Coverage Features That Matter More Than Price

Feature 1 — Replacement Cost vs Actual Cash Value

Always choose Replacement Cost (RC) coverage for both your dwelling and personal property — never Actual Cash Value (ACV). ACV deducts depreciation from your claim payment. A 10-year-old roof costs $18,000 to replace — under ACV, you might receive $9,000 (50% depreciated). Under RC, you receive $18,000. The premium difference is typically 10–15% — worth every dollar.

Feature 2 — Extended Replacement Cost Endorsement

Construction costs increased 35–55% between 2020 and 2026. If your Coverage A (dwelling limit) was set in 2020 and never updated, you may be underinsured by 30–50%. Extended Replacement Cost endorsements automatically increase coverage by 25–50% above your stated limit — protecting you from underinsurance at claim time. Erie Insurance includes this as standard in their policy. Always ask for it.

Feature 3 — Additional Living Expenses Duration

ALE pays for hotel and living costs while your home is being rebuilt. Standard policies cover 12 months or 20% of dwelling coverage. For total loss scenarios (fire, tornado, flood), rebuilding takes 18–36 months in 2026. Choose policies with 24-month ALE coverage or dollar-unlimited ALE rather than time-limited.

Feature 4 — Sewer and Water Backup Coverage

Standard homeowners policies exclude sewer backup and water that enters through drains or sumps. This is one of the most common and most expensive home claims — a sewer backup can cost $10,000–$50,000 in cleanup and repairs. This endorsement adds $40–$100/year to your premium and is one of the best-value add-ons available.

Feature 5 — Identity Theft Coverage

Many carriers now include basic identity theft restoration services as a homeowners policy add-on. State Farm, Allstate, and Travelers all offer identity theft endorsements for $25–$40/year — providing credit monitoring, fraud resolution assistance, and expense reimbursement. For most homeowners, this is more likely to be used than a fire claim.

❓ Frequently Asked Questions

What is the best homeowners insurance company in the USA in 2026?

USAA is objectively the best homeowners insurance company in the USA in 2026 across every major quality metric — 900/1,000 J.D. Power score, A++ AM Best rating, 0.51 NAIC complaint index, and below-average premium at $1,640/year. However, USAA is only available to active military, veterans, and their immediate family. For everyone else, State Farm is the best nationally available homeowners insurer — 882/1,000 J.D. Power (highest of all nationally available carriers), A++ AM Best, and a 0.68 NAIC complaint index (32% fewer complaints than expected for their market size). For the lowest premium among quality carriers, Erie Insurance wins at $1,620/year average with strong satisfaction scores in the 12 states where they operate.

How do I use the J.D. Power score to choose home insurance?

J.D. Power home insurance scores measure overall customer satisfaction on a 1,000-point scale, with the 2026 industry average at 821. When using J.D. Power scores: choose carriers scoring above the industry average (821+) as a baseline filter; pay special attention to the "claims" sub-factor if you're in a high-risk area (wildfire, hurricane, hail) since claims experience is most relevant for frequent claimants; don't use J.D. Power as your only filter — pair it with the NAIC complaint index (which measures formal complaints) and AM Best (which measures financial strength) for a complete picture. A carrier with a high J.D. Power score but poor NAIC complaint index may perform well for routine interactions but generate disputes at claim settlement time.

What does the NAIC complaint index mean for home insurance?

The NAIC complaint index compares the number of formal consumer complaints an insurer receives to the number expected based on their market share. A score of 1.00 is average — the company receives exactly as many complaints as expected for their size. Below 1.00 is better — the company receives fewer complaints than expected. Above 1.00 is worse — more complaints than expected. For homeowners insurance specifically, complaints are most commonly about: claim denials, unsatisfactory settlement amounts, excessive delays, and coverage disputes. Choosing an insurer with a low NAIC complaint index (like Amica at 0.43 or Chubb at 0.38) means you are statistically much less likely to encounter these problems than with a high-index carrier like Liberty Mutual (1.42) or Farmers (1.38).

Is State Farm or Allstate better for homeowners insurance?

State Farm is significantly better than Allstate for homeowners insurance across all major quality metrics in 2026. State Farm scores 882/1,000 on J.D. Power (vs Allstate's 829); State Farm's NAIC complaint index is 0.68 (vs Allstate's 1.24 — nearly double the complaints); State Farm carries AM Best A++ (vs Allstate's A+); and State Farm's average premium ($1,780) is $340 cheaper than Allstate's ($2,120). The only scenario where Allstate is worth considering over State Farm: if you are bundling home and auto and Allstate's 25% bundle discount produces a combined home+auto price that is significantly cheaper than State Farm's 17% bundle discount in your specific case. Run the combined numbers — but for standalone homeowners insurance, State Farm wins decisively.

How much should homeowners insurance cost in 2026?

The national average homeowners insurance premium in 2026 is $1,820/year for a home with $300,000 in dwelling coverage — up 11.4% from 2025 due to construction cost inflation, increased weather catastrophe claims, and higher reinsurance costs. However, premiums vary enormously by state: Louisiana averages $3,400/year (hurricane and flood risk); Oklahoma averages $3,180 (tornado belt); Florida averages $2,800 (hurricane + litigation); Texas averages $2,460; California averages $1,560 (wildfire varies dramatically by county). Midwest and Northeast states like Wisconsin, Ohio, and Vermont average $1,100–$1,400. Within states, location differences (proximity to fire station, flood zone designation, wildfire risk score) can vary premiums by 50–100%. Always compare at least 3 quotes annually — the spread between cheapest and most expensive major carrier for the same home can exceed $800/year.

Is Amica or State Farm better for homeowners insurance?

Both Amica and State Farm are excellent homeowners insurers — the choice depends on what you prioritise. State Farm wins on J.D. Power score (882 vs Amica's 868), national availability (all 50 states vs Amica's more limited availability), agent network depth (19,000+ agents), and brand recognition. Amica wins on NAIC complaint index (0.43 vs State Farm's 0.68 — Amica generates 37% fewer complaints), dividend policy structure (Amica's dividend policies can return 5–20% of premium to claim-free policyholders), and mutual ownership model (policyholders own the company, not shareholders). For a homeowner who values the fewest possible disputes at claim time and the mutual ownership model, Amica is a compelling choice. For maximum accessibility, agent support, and brand certainty, State Farm is the stronger choice.

✅ Final Verdict — Best Homeowners Insurance 2026

USAA wins overall if you're eligible — no other carrier comes close across all three metrics. State Farm wins for everyone else — best J.D. Power nationally, best AM Best nationally, solid NAIC, and competitive pricing. Amica is the best alternative for those who prioritise complaint avoidance above all. Erie is the best value in the 12 states where they operate. Avoid Liberty Mutual and Farmers for standalone home insurance — both have below-average J.D. Power scores, above-average complaint rates, and above-average premiums. Use all three ratings together — J.D. Power + AM Best + NAIC — never choose on premium alone. For a complete Liberty Mutual-specific review, see our article on Liberty Mutual Homeowners Insurance Review 2026. For wildfire-specific coverage considerations, see our Wildfire Insurance Claims Guide 2026.

Disclaimer: J.D. Power scores, AM Best ratings, NAIC complaint indices and premium estimates are based on 2026 publicly available data. Individual premiums vary by location, home characteristics, and personal risk profile. Always verify current data directly with each insurer. Nexuora is not affiliated with any insurer listed. Updated May 9, 2026.

Ahmada Ndao is a financial research analyst and independent journalist

specializing in US consumer finance, legal rights, and insurance markets.

With over 5 years covering American financial products, he has helped

thousands of readers navigate complex insurance decisions, find the right

legal representation, and optimize their credit strategies. His research

methodology combines primary data analysis, direct outreach to industry

professionals, and continuous monitoring of federal regulatory changes.

Ahmada’s work has been cited by financial communities across the US and

reviewed by licensed attorneys and insurance professionals for accuracy.