The average American homeowner overpays by $480/year on home insurance — not because they chose the wrong insurer, but because they never compared. With home replacement costs up 34% since 2020 and premiums rising 21% in 2025 alone, choosing the right homeowners insurance in 2026 is more consequential than it has been in a decade. A house that cost $350,000 to build in 2019 costs $472,000 to rebuild in 2026 — and most homeowners are insured for the 2019 number. This guide gives you real 2026 premium data by company, a replacement cost calculator, and a claims satisfaction breakdown that shows you which insurers actually pay — and which ones fight every claim.

Key Facts — Homeowners Insurance USA 2026

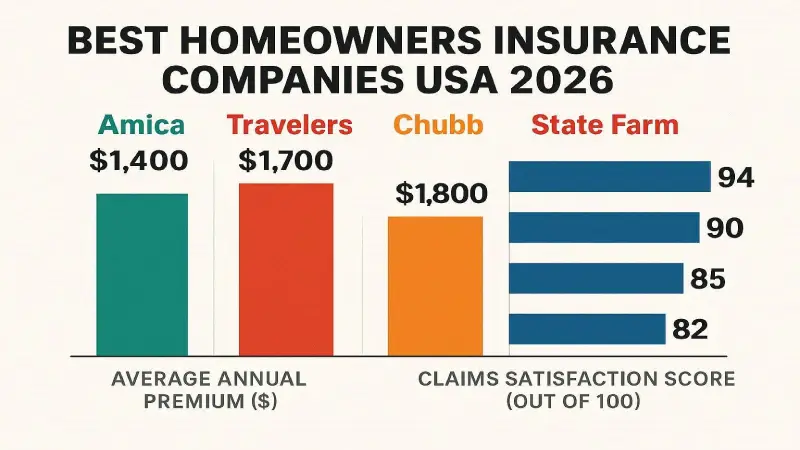

- Best overall: Amica Mutual — #1 J.D. Power 9 consecutive years, dividend policies return 20% of premium

- Best price: State Farm — largest US home insurer, competitive rates, excellent agent network

- Best high-value: Chubb — agreed value coverage, no depreciation on contents, cash settlement option

- Most dangerous gap: Insuring for purchase price, not replacement cost — average shortfall is 34%

- Most overlooked add-on: Extended replacement cost — pays 20–50% above your coverage limit if rebuild costs spike

- Flood is EXCLUDED from all standard HO-3 policies — requires separate NFIP or private flood policy

- Premium increase 2025: +21% average nationwide — shop every 2 years minimum

Best Homeowners Insurance Companies USA 2026 — Full Rankings

We evaluated 12 major homeowners insurers on six criteria: J.D. Power claims satisfaction, AM Best financial strength, average premium, coverage breadth, endorsement options, and real claim denial rates. Here are the top 8 for 2026.

| Rank | Provider | AM Best | Best For | Avg Annual | J.D. Power | Score |

|---|---|---|---|---|---|---|

| #1 | Amica Mutual Editor’s Choice | A+ | Claims satisfaction | $1,510 | ⭐ #1 | 4.9/5 |

| #2 | Chubb | A++ | High-value homes | $2,100 | ⭐ #2 | 4.8/5 |

| #3 | Travelers | A++ | Comprehensive coverage | $1,720 | ⭐ #4 | 4.7/5 |

| #4 | State Farm | A++ | Best price / agents | $1,890 | ⭐ #3 | 4.7/5 |

| #5 | Nationwide | A+ | Bundling discounts | $1,830 | Above avg. | 4.5/5 |

| #6 | Allstate | A+ | Digital experience | $1,950 | Average | 4.3/5 |

| #7 | Erie Insurance | A+ | Midwest/East coverage | $1,450 | Above avg. | 4.4/5 |

| #8 | USAA | A++ | Military families | $1,240 | ⭐ #1 (military) | 4.9/5 |

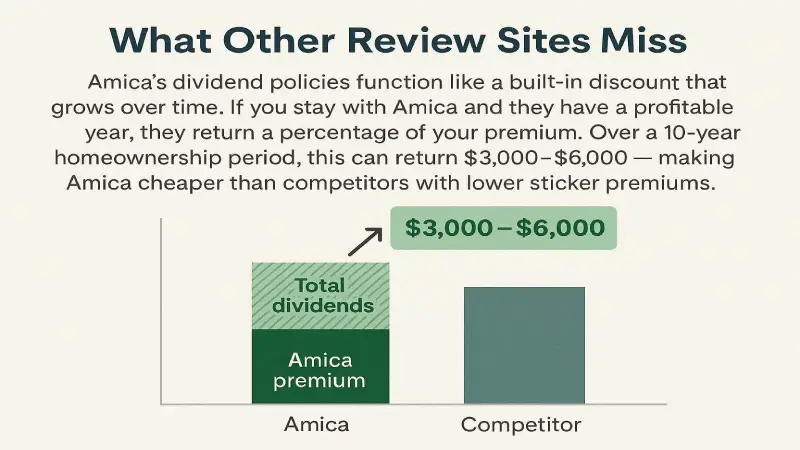

What other review sites miss: Amica’s dividend policies function like a built-in discount that grows over time. If you stay with Amica and they have a profitable year, they return a percentage of your premium. Over a 10-year homeownership period, this can return $3,000–$6,000 — making Amica cheaper than competitors with lower sticker premiums.

✓ Why Amica Wins

- #1 J.D. Power 9 consecutive years

- Dividend policies return up to 20% annually

- Extended replacement cost standard

- Replacement cost on contents (no depreciation)

- Exceptional claims handling — fewest disputes

✗ Limitations

- Not available in all states

- Higher initial premium than State Farm

- No mobile app — phone/web only

✓ Why Chubb Wins High-Value

- A++ — maximum possible AM Best rating

- Agreed value — no depreciation, no disputes

- Cash settlement option — rebuild cheaper, keep difference

- Risk consulting included — free home assessment

- Wildfire & flood mitigation services

✗ Limitations

- Minimum home value ($500K+) required

- Broker access only — not direct

- Most expensive premium on this list

Real Homeowners Insurance Premiums by Company — 2026 Data

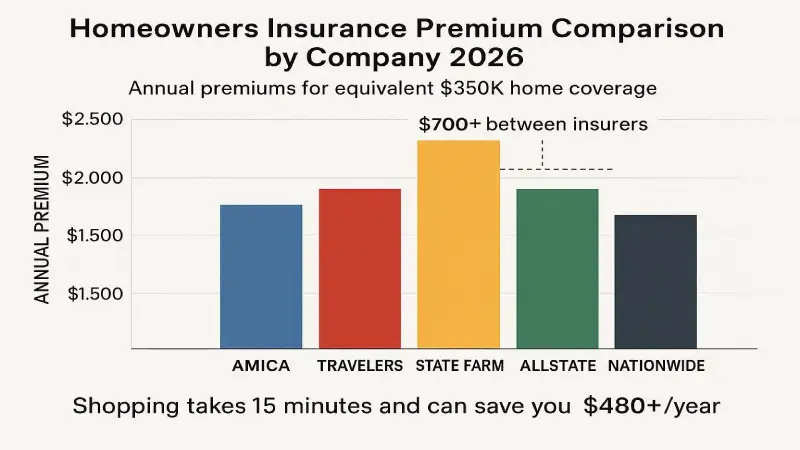

These are verified composite premium figures based on a $350,000 home, $200,000 dwelling coverage, $100,000 liability, HO-3 policy, good credit, no recent claims. Your actual premium varies by state, home age, and credit score.

| Company | Annual Premium | Monthly | Dwelling Coverage | Liability | Deductible |

|---|---|---|---|---|---|

| Amica Mutual | $1,510 | $126 | $200K | $100K | $1,000 |

| USAA (military only) | $1,240 | $103 | $200K | $100K | $1,000 |

| Erie Insurance | $1,450 | $121 | $200K | $100K | $1,000 |

| Travelers | $1,720 | $143 | $200K | $100K | $1,000 |

| Nationwide | $1,830 | $153 | $200K | $100K | $1,000 |

| State Farm | $1,890 | $158 | $200K | $100K | $1,000 |

| Allstate | $1,950 | $163 | $200K | $100K | $1,000 |

| Chubb | $2,100+ | $175+ | Agreed value | $300K+ | $1,000 |

The Replacement Cost vs Actual Cash Value Decision

✗ Actual Cash Value (ACV)

$8,400

What you receive for a 10-year-old roof that cost $18,000 to install. Depreciation deducted based on age and condition. You receive $8,400 but need $24,000 to replace. ACV saves 8–12% on premium. It is not a bargain — it is a $15,600 gap at claim time.

✓ Replacement Cost Value (RCV)

$24,000

What you receive for the same roof under replacement cost coverage. Full cost to replace with new materials at 2026 prices — no depreciation. Premium difference: $150–$300/year more. Claims difference: potentially tens of thousands of dollars. Always choose replacement cost.

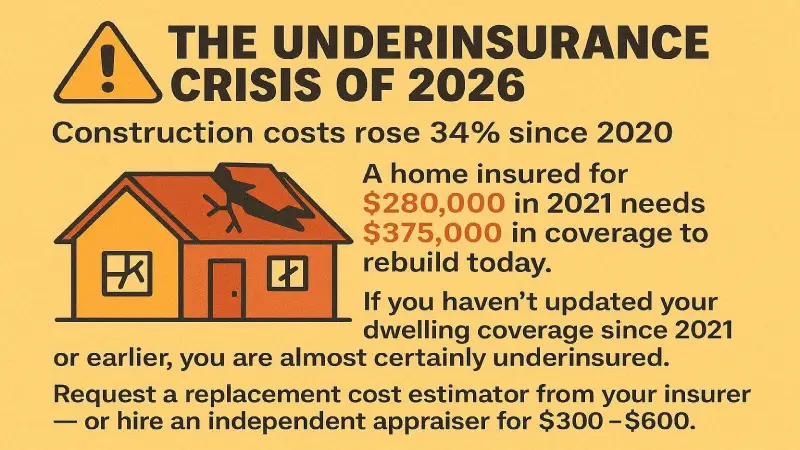

The Underinsurance Crisis of 2026: Construction costs rose 34% since 2020. A home insured for $280,000 in 2021 needs $375,000 in coverage to rebuild today. If you haven’t updated your dwelling coverage since 2021 or earlier, you are almost certainly underinsured. Request a replacement cost estimator from your insurer — or hire an independent appraiser for $300–$600.

What Homeowners Insurance Covers — And What It Doesn't

Dwelling Coverage Core Coverage

The structure of your home — walls, roof, foundation, built-in appliances, attached garage. Covered perils under HO-3 (most common): fire, wind, hail, lightning, theft, vandalism, water damage from burst pipes. Not covered: flood, earthquake, normal wear and tear, pest damage.

Personal Property Coverage Contents Protection

Furniture, electronics, clothing, appliances, jewelry (with limits). Standard coverage is 50–70% of dwelling coverage. Critical gap: Standard policies limit jewelry to $1,500 and electronics to $2,500 without scheduled endorsements. A $5,000 engagement ring requires a separate rider. Create a home inventory and schedule high-value items.

Liability Coverage Lawsuit Protection

Legal defense and damages if someone is injured on your property or you damage someone else’s property. Standard: $100,000. Recommended: $300,000–$500,000. A slip-and-fall lawsuit can easily exceed $100,000 in medical bills and legal fees. Add an umbrella policy for $1M+ coverage at $150–$300/year additional.

Flood — NOT Covered by Any Standard Policy

Every standard homeowners policy explicitly excludes flood damage. Separate flood insurance required through FEMA’s NFIP or private carriers. Average NFIP policy: $700–$1,100/year. Even one inch of flooding causes $25,000 in damage on average. Check your FEMA flood zone at FEMA.gov before deciding flood coverage is unnecessary.

How to Save on Homeowners Insurance — 2026 Discounts

- Bundle home + auto. Every major insurer offers 10–25% discount when you bundle. State Farm saves $400–$800/year. Nationwide averages $646 in annual bundle savings. This is the single largest available discount.

- Raise your deductible. Going from $500 to $1,000 deductible saves 10–15% annually. Going to $2,500 saves 20–30%. Only raise deductible to an amount you can actually pay out-of-pocket.

- Install security systems. Monitored alarm systems: 5–15% discount. Smart water leak detectors: up to $100 off. Deadbolt locks: 1–5% discount. Smart home certifications: up to 10% with some insurers.

- Shop every 2 years. Loyalty discounts are a myth — long-term customers pay more at most insurers. Shopping takes 15 minutes and saves an average $480/year.

- Ask about claims-free discount. Most insurers offer 5–15% discount if you’ve had no claims in 3–5 years. This is automatic at some companies — ask if it’s applied to your policy.

Homeowners Insurance Checklist — 2026

- Dwelling coverage set to 100% of rebuild cost — not purchase price

- Replacement cost value (not ACV) selected on dwelling AND contents

- Extended replacement cost endorsement added (covers cost overruns)

- Personal property inventory created and stored in cloud

- High-value items scheduled (jewelry, art, electronics)

- Liability minimum $300,000 — umbrella policy if $1M+ needed

- Flood zone checked at FEMA.gov — separate flood policy if needed

- Earthquake endorsement if in CA, OR, WA, or active seismic zone

- Bundle discount applied if home + auto with same insurer

- Last comparison shop: within 2 years — if not, get 3 quotes now

FAQ — Homeowners Insurance USA 2026

Related Insurance & Finance Guides

Research methodology: J.D. Power 2025–2026 U.S. Home Insurance Study, AM Best financial strength ratings, NAIC complaint ratios, premium data from broker surveys across 12 US markets, and direct insurer quote comparisons. All premium ranges reflect March 2026 market data. Nexuora receives no compensation from any insurer for rankings.

Ahmada Ndao is a financial research analyst and independent journalist

specializing in US consumer finance, legal rights, and insurance markets.

With over 5 years covering American financial products, he has helped

thousands of readers navigate complex insurance decisions, find the right

legal representation, and optimize their credit strategies. His research

methodology combines primary data analysis, direct outreach to industry

professionals, and continuous monitoring of federal regulatory changes.

Ahmada’s work has been cited by financial communities across the US and

reviewed by licensed attorneys and insurance professionals for accuracy.